-

-  -

-

See also: Latest at nejtillemu.com

- -

The U.S. trade deficit, $43.5 billion in goods and

services, widened in March to the second highest on record

.

The

figure compares with a record $44.9 billion shortfall in December.

May

13 2003 Bloomberg

The decline in the dollar may have contributed to a 2.9 percent increase

in imports to $126.3 billion, the second highest on record behind September

2000. Goods ordered months ago and being delivered in March cost more because

the dollar has fallen 10 percent against the euro this year.

Imports from

Western Europe surged in March to a record as the trade deficit with the region

rose to $7.8 billion from $6.6 billion.

Trade deficit swells to $130B in 2Q

Current Account deficit

passes $112.5B record set in 1Q

http://www.bea.gov/bea/newsrel/transnewsrelease.htm

The U.S. trade deficit narrowed in June as American companies increased exports for a fourth consecutive month, helped by a decline in the dollar. Aug. 20 (Bloomberg)

The $37.2 billion gap in goods and services trade followed a record $37.8 billion deficit in May.

Exports rose 1.7 percent in June to $82 billion.

Imports rose 0.5 percent for the month to $119.2 billion.

With the dollar back in the ascendancy, the threat posed by the US

current account deficit once again seems remote. But research by HSBC offers a

reminder of the danger for the US economy if the market insists on a

significant adjustment in the current account position.

Christopher Swann Financial Times; Aug 09, 2002

The reduction of the US current account deficit in the mid to late 1980s was brought about by a large fall in the dollar, with a fall against the yen from Y260 to Y140.

The first problem for the US is that the J-curve effect - which stipulates that the the price effects of a depreciation initially outweigh the volume effects - meant that the falling dollar initially led to a deterioration of the current account position. This was evident during the dollar's fall in the years after 1985.

Between 1985 and 1987 the US current account rose from $124bn to $168bn. Only in 1988 did it fall back to $128bn, reflecting the enhanced competitiveness of the US economy. It took until 1990 before the current account was balanced.

This time even this kind of slow progress on the current account deficit may be hard to achieve through depreciation, said David Bloom currency strategist at HSBC.

"With the Japanese economy in its current situation and with no flexibility for monetary easing, it would be unthinkable for the Japanese to allow such a pronounced appreciation in their currency," said David Bloom, currency strategist at HSBC in London.

This has been illustrated by persistent intervention by several Asian states, including South Korea, to curb the rise in their currencies against the dollar.

Since Asia accounts for a large percentage of the US current account deficit, it would be impossible to resolve the problem through a depreciation of the dollar that excluded Asian states.

This leaves either slower growth or lower asset prices as potential solutions to the deficit.

Again the precedent of the late 1980s is not encouraging, said Mr Bloom. Between 1987 and 1990 the average growth in G6 economies excluding the US was 4.25 per cent. This meant the US could expand at a respectable 2.75 per cent and still use slow growth to narrow the current account gap.

"The current anaemic rates of growth in the other large economies mean that the US would face four years of near stagnation," said Mr Bloom.

US trade deficit hits record high

FT, July 19

2002 15:16

The monthly US trade deficit hit a record $37.6bn in May, according to an official report released yesterday that suggested a resumption of economic growth world-wide - but that report also put downward pressure on the US dollar, equity prices and GDP forecasts.Full text

Dollar

falls on record trade gap

BBC 19 July, 2002

Handelssiffror sänker dollarn

DI, 2002-06-20

Dollarn tappade mark efter att handels- och tjänstebalansen stigit till 35,9 miljarder dollar i april, vilket var klart över förväntningarna på minus 32,2 miljarder dollar.

Dollarn, som på senare tid försvagats på ett sämre sentiment för den amerikanska ekonomin, tappade från strax under 0:96 till 0:9625 mot euron i en initial reaktion. Mot yenen tappade dollarn till 123:50 från 123:75.

Dollar/euron handlas därmed på sin högsta nivå sedan i juni 2000. Euron har därmed också lyckats bryta igenom en teknisk nivå strax under 0:96 mot dollarn som även testades i januari 2001.

Även bytesbalansen i USA för första kvartalet kom in sämre än väntat, med ett underskott på 112,5 miljarder dollar mot väntade -108,0, vilket också tyngde dollarn.

Euro soars on record US trade gap

BBC, 20 June, 2002, 19:26 GMT

News of a record US trade deficit has propelled the European single currency to a two-year high against the dollar.

The euro rose from $0.9574 late on Wednesday to $0.9645 on Thursday, its strongest showing since June 2000.

The single European currency's new-found strength stemmed from figures showing that the US current account deficit had mushroomed to a record $112.5bn in the first three months of the year.

The higher current account deficit - which shows that more money is leaving the US in the form of foreign investments and spending on imports than is coming in - suggests rising demand for foreign currencies, undermining the dollar.

Investors shun US shares

"If the market ever needed convincing the US dollar is overvalued, it received it in spades this morning," said Sal Guatieri, economist at the Bank of Montreal.

The latest figures came in ahead of most analysts' forecasts, and marked an 18.3% increase on the current account gap for the last three months of 2001.

The rise in the first quarter current account deficit was fuelled partly by a sharp fall in spending on US shares by private foreign investors, reflecting concerns over the earnings prospects of US corporations.

Separate figures showed that the US trade deficit in goods and services for April widened to $35.9bn, itself a new monthly record.

The April trade deficit - which measures spending on goods and services, but excludes financial flows from stock and bond purchases - partly reflected an increase in spending on oil imports.

The US trade deficit with Japan grew to $6.8bn from $5.71bn in March, while the shortfall with the European Union widened to $5.14bn from $4.42bn.

US optimistic as trade deficit shrinks

BBC, 17 May, 2002

The US trade deficit shrank to $31.63bn, 0.4% narrower than the $31.75bn trade gap recorded in February.

Exports rose 0.6% during March, fuelled by a rise in the demand for American cars and car parts, commercial aircraft and computers.

The exports rise offset a 0.3% rise in imports.

The imports rise was largely attributed to a sharp rise in crude oil prices.

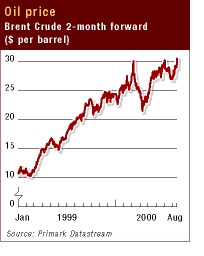

US oil imports rose 15.7% to $6.83bn during the month after a $2.62 rise in the price of a barrel of crude oil to $19.18.

U.S. Trade Deficit Climbed To $28.5 Billion in January

WALL STREET JOURNAL March 19, 2002

U.S. Trade Deficit Climbed To $28.5 Billion in

January

WALL STREET JOURNAL March 19, 2002

The U.S. trade deficit widened to $28.5 billion in January as the nation's foreign oil bill surged and U.S. exports fell to the lowest level in more than three years.

For all of 2001, the deficit showed an improvement for the first time in six years, narrowing by 7.5% to $347.5 billion. That was still the second-highest deficit in history.

Economists are warning that this year the improvements could stall as a recovering U.S. economy draws in imports at a faster clip while U.S. exports are held back by economic weakness in many of America's trading partners.

Additionally, U.S. manufacturers are demanding that the Bush administration switch its policy on the dollar, contending that an overvalued U.S. currency is seriously crimping their ability to export.

So far, however, Treasury Secretary Paul O'Neill has insisted there will be no change in the dollar policy inherited from the Clinton administration, which insisted that a strong dollar was in the best interests of the U.S.

While a strong dollar hurts exports, its helps to keep inflation down by making imports cheaper. It also makes investments by foreigners in U.S. stocks and bonds more attractive, fostering an inflow of cash the U.S. needs to finance its huge merchandise deficits.

Imports grew 3.6% during the month to $106.49 billion.

Oil imports were up by 11.1% to $6.5 billion. This increase reflected a rise in the volume of crude-oil shipments and the price per barrel, which rose by 80 cents to $16.31 in January.

Exports fell for the second month in a row, declining to $77.97 billion from December's $78.04 billion.

US Trade Data Distorted, But Show Econ Slump -

Official

/September trade figures/

Dow Jones 2001-11-21

The September trade figures were distorted by the one-time effect of insurance claims after the Sept. 11 terrorist attacks, but the numbers continue to reflect an economy that is losing altitude, said U.S. Commerce Undersecretary for Economic Affairs Kathleen Cooper.

The trade gap narrowed a record 31% in September to $18.69 billion - its lowest level since March, 1999 - from $27.11 billion in August.

Imports plummeted 14.0% to $95.99 billion, led by an $11 billion drop

in insurance imports, and

exports plunged 8.5% to $77.29 billion.

Economists have said that excluding the one-time adjustment for post-Sept. 11 insurance claims, which resulted in lowering service imports, the trade gap would have widened to nearly $30 billion.

The Commerce Department said foreign insurance companies' payments of U.S. claims following Sept. 11 subtracted about $11 billion from imports in September.

While Cooper wouldn't speculate on how large the deficit may have been excluding the special factor of the insurance payments, she said the trade numbers show the economy is struggling.

The U.S. trade deficit in August

Wall Street

Journal 2001-10-19

The U.S. deficit in international trade of goods and services narrowed to $27.11 billion in.

As the U.S. economy has slowed, imports have fallen faster than exports, narrowing the trade deficit from its most recent peak of $33.8 billion last October.

U.S. imports fell by 1.1% in August to $111.57 billion.

Exports, meanwhile, rose for the first time since May, rising 1% to $84.46 billion in August.

The U.S. trade deficit fell in April, but...

CNN,

2001-06-21

but the drop followed a record-setting gain in March and was still higher than forecasts by Wall Street economists.

The nation's trade deficit shrank to $32.2 billion in April from a revised $33.1 billion in March.

Economists polled by Briefing.com had expected a deficit of $30.9 billion.

Imports fell 2.2% to $119.09 billion.

Imports of capital goods, such as semiconductors, aircraft and telecommunications equipment, were the lowest since November 1999, falling by $2.76 billion to $25.98 billion.

Imported consumer goods, like toys, clothes and household appliances, slipped by $1.19 billion to $24.25 billion in April. The declines offset increased imports of food, automobiles and industrial supplies.

The nation's oil bill inched up to $6.66 billion from $6.65 billion, as higher demand offset lower prices.

The average price for a barrel of oil fell to $21.65 in April from $22.76 the month before.

Exports fell 2% to $86.92 billion, the lowest level in a year, as lower sales of capital goods offset record shipments of American-made consumer goods.

In a separate report, the Commerce Department said the current-account deficit narrowed to $109.6 billion during the first quarter from a revised $116.3 billion in the fourth quarter of 2000.

The fourth-quarter figure previously had been estimated at $115.3 billion.

The March trade gap was previously reported at about $31.2 billion, and resulted from the biggest one-month gain since the Commerce Department started keeping track of it in 1992.

Trade Deficit Shrinks by $6.26 Billion, As Imports Drop by a Record Amount

THE WALL STREET JOURNAL 2001-04-19

The U.S. trade deficit narrowed a whopping $6.26 billion in February, as U.S. consumers finally curbed their appetite for imports.

The trade deficit contracted to $26.99 billion from January’s record $33.25 billion, the Commerce Department reported. February’s deficit is the smallest in 14 months, reflecting the biggest monthly narrowing to date.

Imports, adjusted for seasonal variation, staged a stunning about-face after their recent rise, plummeting $5.39 billion to $117.45.

The decline in imports was the biggest since the Commerce Department began compiling the monthly figures in 1992.

But economists were quick to point out that a big drop in oil prices was one of the main reasons behind the plunge in imports, and they predicted it wouldn’t last.

Ian Shepherdson, chief U.S. economist with High Frequency Economics Ltd. in Valhalla, N.Y. added: “And a shrinking deficit due to plunging domestic demand is not exactly great news.”

Exports continued their anemic growth, rising to $90.46 billion.

The deficit with China contracted to $5.07 billion, the smallest since April 1999.

U.S. Current Account Deficit Widened To

Record $115.27 Billion

Wall Street Journal 2001-03-16

For the quarter, the current account deficit remained at about 4% of gross domestic product.

For the year, the gap widened to $435.38 billion from the previous record in 1999 of $331.48 billion.

The shortfall in goods and services trade, the largest component of the overall current account deficit, swelled to $98.85 billion in the fourth quarter

Trade Gap $32.99 Billion in December

This brings the trade deficit for the year 2000 to a record $369.69 billion, sharply higher than $264.97 posted in 1999.

“The good news is that slower growth and lower oil prices are pulling down imports, which have fallen for three straight months,” Mr. Shepherdson said, “but the bad news is that the strong dollar and slower growth in other countries is pulling exports down too.

Imports eased 0.7% to $122.81 billion, reflecting a $1.4 billion drop in automobile imports as dealers sought to reduce excess inventories. Demand for imported consumer goods also fell by $700 million, and food imports dropped $200 million.

Petroleum prices, with the price per barrel falling to $26.53 in December from $28.40. Even so, the value of crude imports during the month of record cold temperatures rose to $7.65 billion from $7.22 billion.

The volume of crude imports rose to 288 million barrels from 254 million barrels in November.

Exports declined 0.8% to $89.82 billion as the strong U.S. dollar continued to take a toll on exporters.

The gap with China fell to $6.06 billion from $7.60 billion in November, while the deficit with Japan also narrowed to $6.06 billion in December from $6.75 billion.

U.S. deficits with North American Free Trade Agreement partners were mixed, with Canada’s rising to a record $5.73 billion from $4.48 billion, and Mexico’s falling to $1.71 billion from $1.99 billion.

The gap with the European Union fell to $3.34 billion from $5.28 billion.

The 2000 trade deficit of $369.7 billion was 39.5% higher than the previous record-holder, a deficit of $265 billion in 1999.

The trade deficit has set an annual record for the past three years as the strong U.S. economy has been a magnet for imports while many of America’s major export markets have been struggling to recover from currency crises in 1997 and 1998.

Trade Gap Narrowed in November To $32.99 Billion as Imports Dropped

WASHINGTON -- The trade gap narrowed in November as lower oil prices helped propel the largest monthly drop in imports in almost a decade.

The trade gap shrank to a seasonally adjusted $32.99 billion, down from a revised $33.55 billion in October.

For the second month in a row, both imports and exports declined. And, as in October, imports dropped at a steeper pace than exports.

The year-to-date trade gap through November hit $335.89 billion and remained solidly on track to set a record. Through November 1999, the gap was $239.32 billion.

Imports slipped by 1.1% to $123.35 billion in November, led by a smaller bill for imported petroleum. Crude petroleum imports fell to $7.22 billion, the lowest level since May and down sharply from the $8.45 billion seen in October. The decline was aided by a 22-cent fall in per barrel prices to $28.40

November exports fell 0.8% to $90.36 billion, with the decline concentrated in capital goods like autos, computer accessories and airplanes.

The data are likely to push fourth-quarter growth moderately lower. The Commerce Department is set to release its estimate of Gross Domestic Product growth on Jan. 31, the same day Federal Reserve policy makers meet to decide interest rate policy.

The deficit with the European Union fell slightly, to $5.28 billion from $5.55 billion.

So did the gap with members of the Organization of Petroleum Exporting Countries, declining to $3.81 billion from $4.33 billion. For the year to date, the $43.54 billion deficit with OPEC countries was more than double what it was in the same period a year ago.

U.S. Trade Gap Unexpectedly Narrows To $33.18 Billion; Oil Imports

Increase

A WSJ.COM News Roundup 2000-12-19

The trade gap narrowed in October despite higher oil imports as demand for food, industrial supplies, automobiles and other big-ticket items languished.

The deficit in international trade in goods and services narrowed to $33.18 billion, down from September’s revised $33.74 billion—the biggest imbalance in history, the Commerce Department said Tuesday. The September shortfall initially had been estimated at $34.26 billion.

For the first 10 months of the year, the gap has ballooned to $302.53 billion, far beyond the $264.97 billion recorded during the same period in 1999.

During October, imports fell 1.6% to $124.42 billion. Imports of consumer goods, however, rose $100 million as merchants prepared for the Christmas season.

Although analysts had expected a lower oil bill, the U.S. actually imported more crude -- $8.45 billion worth—than in the prior month.

This came despite a 36-cent decline in the price of oil to $28.62 per barrel.

Imports from members of the Organization of Petroleum Exporting Countries during the month were a $6.4 billion record.

Exports declined 1.5% to $91.23 billion, following several months of strong growth this year.

America’s deficit with China rose to $9.07 billion, a record, as the world’s most populous country remained on track to surpass Japan this year as the nation with the largest trade surplus with the U.S.

The deficit with Japan climbed $8.42 billion.

Trade gaps with NAFTA partner Canada also hit an all-time high of $4.71 billion, while the deficit with Mexico narrowed slightly to $2.38 billion.

The deficit with the European Union jumped to $5.55 billion from $3.92 in the previous month.

Trade has continued to be the major blot on America’s economic performance as the appetite for imports far outstrips U.S. export sales.

Critics of President Clinton’s trade policies argue that the administration’s insistence of pursuing open-market agreements with other countries has left U.S. workers vulnerable to unfair competition from low-wage foreign factories. But the argument has been overshadowed by the economy’s remarkable domestic performance, which pushed the unemployment rate to a three-decade low.

The unemployment rate is expected to slowly rise over the next year under the impact of interest-rate increases by the Federal Reserve. Some analysts believe this will spawn greater demands for Congress to erect protectionist barriers to keep foreign goods out of the country.

The Clinton administration argues that in an era of increasing globalization, America has no choice but to push for trade liberalization, which benefits U.S. consumers and opens foreign markets for American exporters.

U.S. Current-Account Deficit Widened To $113.77

Billion in the Third Quarter

CNN 2000-12-14

The current-account gap widened to a record level in the third quarter - $113.77 billion. It topped the revised $104.97 billion record set in the prior quarter.

Many economists fret that a deficit of this magnitude is unsustainable in the long run, and worry that a sudden shift in foreign-investor sentiment toward the U.S. could trigger a destabilizing slide in the value of the U.S. dollar.

But so far, the U.S. growth outlook has continued to outshine its major trading partners, encouraging foreigners to keep the funds flowing. Economists admit that it is impossible to predict whether or when investors abroad decide to tighten the purse strings.

The shortfall in goods and services trade, the largest component of the overall current-account deficit, grew to $96.5 billion during the third quarter from an $88.6 billion deficit in the prior quarter.

The balance on investment income also recorded a deficit, $4.52 billion, as foreigners earned more returns on investments abroad than Americans.

Financial transfers, like foreign aid and payments to international organizations, contributed $12.75 billion to the overall current-account deficit.

Full article at Wall Street Journal

U.S. Trade Gap Widened To Record $34.3 Billion

in September

Washington, Nov. 21 (Bloomberg)

The U.S. trade deficit widened to a record in September as imports of heating oil, chemicals, other petroleum products and natural gas surged while exports fell, government statistics showed today.

The $34.3 billion shortfall followed a gap of $29.8 billion in August that had been the narrowest in four months, the Commerce Department said. The report tracks trade in goods and services.

The numbers suggest little slowdown in U.S. demand for foreign-produced commodities, made cheaper by a dollar that has risen at least 12 percent this year against a trade-weighted mix of currencies.

The strong dollar is also making it harder for the U.S. to sell its goods abroad.

”America’s appetite for cheap imported goods continues,” said Chris Rupkey, an economist at Bank of Tokyo Mitsubishi in New York, before the report. ”Much to the chagrin of U.S. business, these goods continue to stream to our shores, making it impossible for them to raise their prices in order to firm up their sagging profit margins.”

Imports rose 3.1 percent in September to a record $126.6 billion, as the trade gaps with China, Canada and Mexico all set records. Exports fell 0.7 percent to $92.4 billion, reflecting weaker demand for automobiles and auto parts, oil drilling rigs, computer accessories and telecommunications equipment.

Through September, the trade deficit totaled $270.2 billion this year, up from $188.7 billion during the first nine months of 1999, according to the Commerce Department. The September deficit puts the annual shortfall on track to reach a record $360 billion, compared with the previous high of $265 billion in 1999.

Crude oil futures had risen to a 10-year-high of $37.80 a barrel on Sept. 20. The trade figures reflect the value of merchandise and the U.S. imports more than half its oil.

The average cost of a barrel of crude oil, as calculated by the Commerce Department, rose to $28.90 in September, the highest since the Iraqi occupation of Kuwait in November 1990.

Imports of consumer goods rose 2 percent in September after a gain of 0.9 percent in August. Shipments into the Port of Los Angeles increased 26 percent in October to a record 251,000 containers.

Many of those incoming ships bore holiday goods. U.S. households will probably spend $490 on gifts this Christmas season, compared with $495 last year, based on a survey of 5,000 by the Conference Board.

A euro that has declined as much as 18 percent against the dollar this year is eroding sales of many U.S. made products.

U.S. trade deficit narrows - helped by exports

and lower (!) oil prices

CNN and Wall Street Journal, October 19, 2000

The United States trade deficit narrowed significantly in August from July as the value of goods and services leaving the country gained on the value of imports, pushing the gap to its lowest since February.

The trade deficit narrowed in August to $29.44 billion. That was $2.26 billion below July's revised $31.7 billion deficit.

Imports rose to a record $122.5 billion during the month from a revised $121.5 billion in July, reflecting strong demand for imported autos and raw materials.

Falling oil prices held back the impact of record imports. Crude-petroleum imports totaled $8.24 billion in August, down from $8.37 billion in July. On a per barrel basis, crude oil was $26.59.

The deficit with Japan narrowed, to $6.76 billion, as did that with the European Union, $4.69 bn.

However, the nation's largest and politically problematic deficit, that with China, grew to $8.60 billion in August from $7.64 billion.

Exports also rose to a record, ringing in at $93.02 billion for the month, up from a revised $89.8 billion in July. Notably, the gain in exports came without a wide swing in sales of civilian aircraft.

Financial Times figures about US Trade

U.S. July Trade Gap Widens to Record $31.9 Billion

The U.S. trade deficit widened to a record in July as imports of oil and goods from China reached the highest.The shortfall in goods and services grew to $31.9 billion from $29.8 billion in June.

A record volume of oil helped push imports up 0.6 percent to a record $121.6 billion. Auto imports also rose.

Exports fell 1.5 percent to $89.7 billion.

``This tells us that demand in the U.S. is still pretty strong,'' said Mark Vitner, an economist at First Union Securities Inc.

Oil imports rose 4.3 percent in July to $8.4 billion. The volume reached a record 301 million barrels, and the average price rose to $27.76 a barrel, the highest since Iraq's occupation of Kuwait in November 1990.

Crude oil for October delivery rose 89 cents today to a 10-year high of $37.40 a barrel.

Increased imports of oil from the North Sea as well as a declining euro contributed to a record $7.2 billion trade deficit with Western Europe.

The trade gap with China reached a new high - $7.6 billion. Imports from China touched a record $9.3 billion.

The gap with Japan set a record of $7.52 billion, reflecting exports of $5.07 billion and imports of $12.59 billion.

The gap with Canada reached a record $4.75 billion from the $4.08 billion logged in June. But the $2.19 billion trade shortfall with Mexico represented a slight narrowing from June's $2.28 billion mark.

Through July, the trade deficit totaled $206.3 billion this year, up from $140.7 billion during the first seven months of 1999.

The July number puts the annual shortfall on track to reach $354 billion, compared with the record $265 billion in 1999.

Current-Account Deficit Climbs to a Record High

Figure Expanded

to $106.1 Billion In 2nd Quarter

THE WALL STREET

JOURNAL September 14, 2000

The current-account deficit hit yet another record high last quarter. The deficit reached $106.1 billion in the second quarter, up from a revised $101.5 billion in the year's first three months.

The figure was slightly below the $108 billion that many economists expected, but still kept the U.S. on pace for an astounding $425 billion gap for the year.

The deficit is a constant source of nervousness in world-wide financial markets and among policy makers. For years the U.S. has been running up an ever-larger tab with foreigners, buying more overseas than it sells abroad and paying for it by borrowing foreign money.

Economists know that can't keep up forever. But they are uncertain whether the gap will narrow sooner rather than later, or whether it will happen sharply or slowly.

A sharp adjustment, perhaps caused by a big correction in U.S. stock markets or a tumbling dollar as foreigners pull their money from the U.S., could create a serious economic slowdown.

If, however, the U.S. economy slows gradually, as Europe and Japan pick up speed, the current-account deficit might narrow benignly.

Investment income

Income receipts on U.S.-owned assets abroad

increased to $86.4 billion.

Income payments on foreign-owned assets in the

United States increased to $89.5 billion.

Foreigners bought a net $222.7 billion in U.S. assets during the second quarter, down from $236.5 billion in the first three months of the year.

Net financial inflows for direct foreign investment - foreign purchases of U.S. companies, plants and the like - measured nearly $80 billion in the second quarter. In contrast, those net inflows measured $84.5 billion for all of 1996.

In the second quarter, goods imports rose 4.3% to $302 billion, while goods exports rose 4.4% to $191.8 billion.

Still, some pessimists cringe every time a new current-account deficit record is set. "To take the complacent view that the markets will definitely deal with this problem is naïve," says Dimitri Papadimitriou, president of the Jerome Levy Economics Institute at Bard College, in Annandale-on-Hudson, N.Y.

A new factor - oil prices - is further clouding the outlook. The price of petroleum imports rose a moderate 0.6% in August, after dropping 1.6% in July and soaring 10.6% in June.

U.S. trade gap hits record

The U.S. trade deficit hit its third record in the last four months in June, rising to $30.62 billion.

Rising prices for oil and other imports drove the deficit to the record levels, although it actually came in lower than expected. A survey of analysts by Briefing.com forecast the deficit would rise to $31.5 billion in the month, compared with the revised $30.31 billion in May, which also was a record.

U.S. exports increased to $90.6 billion from $86.6 billion in May. Exports were helped by improved shipments of capital goods, primarily semiconductors and computer accessories, industrial supplies and materials as well as consumer goods.

Imports increased to $121.2 billion from $116.9 billion in May, primarily due to an increase in the amount spent on crude oil.

U.S. Trade Deficit at Record High

BBC 2000-07-20

The US trade deficit set a new record, as the booming economy continued to suck in imports. Both exports and imports in the United States are falling, but the country's trade gap is widening and now stands at a record $31.04bn in May.

The overall decline in trade - the second in as many months - was unexpected, but with the US economy still more buoyant than that of its trading partners, exports plunged faster than imports.

According to the US Commerce Department, the trade gap with key countries like Canada and Mexico surged to new highs. It was hardly a surprise that the trade deficit with oil producing countries rose sharply, but it also widened against Europe and China. The exception was Japan, where the trade gap closed ever so slightly.

With much of the world economy slow to pick up pace, the bullish US economy has been buying more and more foreign goods, expanding the trade gap month after month.

A string of interest rate rises by the US central bank, the Federal Reserve, seems to have done little to contain the demand for imported products. In contrast, higher interest rates have boosted the US dollar against most other currencies, making US goods more expensive to buy abroad.

During May, US exports fell to $85.75bn - down from $86.58bn in April.

Imports dropped to $116.79bn in May, after weighing in at $117.08bn in the previous month.

Wall Street economists had expected the deficit to narrow slightly in May.

The growing trade deficits with the rest of the world have been fanning protectionist pressures in the United States, and have made it harder to reach agreement on further measures of trade liberalisation.

U.S. Trade Deficit Narrows with lower Oil Prices

U.S.

Current Account Deficit at Record High

Washington, June 20 (Bloomberg) The U.S. trade deficit narrowed in April from the previous month's record as a dip in oil prices offset increased demand for foreign-made autos, computers and consumer goods, government figures showed today.

The April deficit in goods and services shrank to $30.4 billion from $30.6 billion during March.

So far this year, the deficit is $116.6 billion, compared with $71.6 billion for the first four months of 1999.

Analysts expect the trade deficit to widen again. Oil prices have begun rising after an April decline.

Demand for cars and electronic equipment has grown since last year, private industry data also show.

And inbound cargo U.S. seaports suggest U.S. businesses have been stockpiling record volumes of Asian goods even as some recent U.S. indicators point to slower consumer spending.

Imports of goods and services fell 0.2 percent to $117.1 billion during April, reflecting lower petroleum prices as well as reduced imports industrial supplies and materials, which includes oil, and food.

For all of last year, the trade deficit totaled a record of $265 billion.

The government reported separately that a broader measure of the U.S. trade deficit that also includes financial transactions widened to a record $102.3 billion in the first quarter.

The growth in the Current Account Deficit came as overseas investors earned more on their U.S. holdings. The shortfall was $96.2 billion in the fourth quarter.

A 3.7 percent decline in oil imports contributed to a narrowing of the April deficit in goods and services.

The futures price of a barrel of crude fell to less than $24 on April 10 after exceeding $34 in March, the first time it was that high in more than nine years.

Prices took off again in May and June and averaged more than $32 a barrel this week on the New York Mercantile Exchange. The Commerce Department said oil averaged $24.42 a barrel in April.

Imports of consumer goods -- ranging from apparel to home electronics -- rose 1.8 percent.

In April, inbound shipments at the Port of Los Angeles, one of the nation's busiest ports, set a record. Imports also exceeded 200,000 containers for the second time in the port's history during May.

Imports of cars and trucks rose 0.8 percent in April.

Motor vehicle imports have grown this year. Although U.S. auto sales slipped in May, imports grabbed a larger share of sales. The Japanese Automobile Manufacturers Association reported last month that exports to the U.S. rose to 175,724 vehicles in April, up 50 percent from a year earlier.

Toyota Motor Corp.'s May sales rose 2.7 percent for the Japan- based maker's best month ever. Although North American-made vehicles accounted for 64 percent of the total, Toyota imports had risen almost two-thirds. Honda Motor Co. and Volkswagen AG also gained.

The record $7.3 billion deficit with Japan compared with $6.8 billion in March and $5.6 billion during April 1999.

The deficit with China rose to $5.8 billion in April from $5.1 billion during March and $4.8 billion during April 1999.

Last week, the U.S. House Appropriations Committee rejected a bid to restore $22 million in trade-enforcement funds, dealing a blow to White House efforts to ensure China adheres to its World Trade

Elsewhere, the deficit with Asia's newly industrialized countries rose to $1.4 billion in April.

The deficit with Canada, the largest U.S. trading partner, rose to $3.9 billion, the second highest on record.

The deficit with Mexico fell to $1.5 billion.

The deficit with Western Europe fell to $4.6 billion.

May 19 (Bloomberg) The deficit in goods and services rose to $30.2 billion in March from $28.7 billion during February.

Imports rose to a record as the price of oil reached the highest level in more than nine years and shipments of autos into the U.S. increased for the fourth time in the last five months.

Exports also set a record in March, led by increased shipments of semiconductors, telecommunications equipment, automobiles and industrial supplies.

Imports of goods and services rose 3.4 percent to $117.4 billion during March as the price of crude oil increased to $26.38 a barrel, the highest since November 1990. March imports of crude oil rose to a record $7.6 billion.

Exports rose 2.9 percent to $87.3 billion in March.

March imports of crude petroleum rose 17.8 percent to $7.6 billion. Excluding oil, imports rose 2.5 percent.

Oil prices fell from a nine-year high of $34.37 a barrel on March 8 after members of the Organization of Petroleum Countries signaled their intention to boost output.

Last Friday, prices rose back to $30 for the first time since March 20, pulled higher by gasoline prices and concern that producers won't increase oil output as demand rises later this year.

The government also reported that the trade deficit with OPEC rose to a record $4.2 billion in March.

Through March, the deficit totaled $86.3 billion versus $54.2 billion during the first three months of 1999.

For all of last year, the trade deficit totaled a record of more than $267.6 billion.

Consumer spending galloped at the fastest pace in 15 years during the first quarter of the year, reflecting the lowest unemployment rate in 30 years, rising incomes and gains on stocks and other investments.

The trade deficit with China fell to $5.1 billion in March from $5.6 billion during February. It was $4.6 billion in February 1999.

Congress is set to vote next week on a bill that would guarantee China low-tariff access to the U.S. market, as part of China's effort to join the World Trade Organization.

The bill's supporters, including President Bill Clinton and Federal Reserve Chairman Alan Greenspan, say China's entry into the WTO - which will lower tariffs and further open China's markets to U.S. manufacturers - is essential to continuing U.S. economic prosperity.

In turn, permanent normal trade relations for China will give the Chinese more incentive to negotiate contracts with U.S. companies, supporters of the measure say.

The merchandise trade deficit with Japan rose to $6.8 billion in March from $6.7 billion during February and $6.5 billion in March 1999.

The deficit with Canada, the largest U.S. trading partner, rose to $3.9 billion from $3.1 billion.

The deficit with Mexico fell to $1.9 billion from $2 billion.

The deficit with Western Europe rose to $5.9 billion from $3.5 billion.

U.S. Feb. Trade Deficit Widens to a Record $29.2 Bln

April

19 (Bloomberg)

The U.S. trade deficit widened to a record in February as the price of imported oil soared and exports fell.

The deficit in goods and services grew to $29.2 billion in February from $27.4 billion during January.

February imports of crude petroleum rose to a record $6.5 billion.

Excluding oil, imports fell 0.6 percent, reflecting reduced shipments of automobiles, televisions, VCRs, clothing and toys. Even so, analysts say there is little sign that the consumer appetite for imported goods is waning. Imports in February were 19 percent higher than a year earlier.

Exports fell for a second straight month, as outbound shipments of civilian aircraft and other capital goods declined. Still, exports of business services and goods were 9.5 percent higher than in February 1999.

Imports rose 1.5 percent to a record $113.4 billion during February.

The $8.8 billion deficit in petroleum products alone was the largest since the government started tracking those numbers in 1989, the Commerce Department said. Exports fell 0.2 percent to $84.2 billion.

For all of last year, the trade deficit in goods and services totaled a record of more than $271 billion.

The merchandise trade deficit with Japan widened to $6.7 billion in February from $5.6 billion during January and $5.3 billion in February 1999.

The trade deficit with China narrowed to $5.6 billion in February from $6 billion during January. It was $4.6 billion in February 1999.

Elsewhere, the deficit with Asia's newly industrialized countries narrowed to $2.1 billion from $2.5 billion in January.

The deficit with Canada, the largest U.S. trading partner, narrowed to $3.3 billion from $4.1 billion a month earlier.

The deficit with Mexico widened to $2 billion from $1.8 billion in January.

The deficit with Western Europe narrowed to $3.5 billion from $3.6 billion.

Trade Deficit Set $28 Billion Record In January as Gap With China

Widened

March 22, 2000 THE WALL STREET JOURNAL

The U.S. trade deficit hit a record $28 billion in January, with the gap with China ballooning just as Congress prepares to consider a hotly contested bilateral trade agreement.

The overall monthly U.S. deficit in goods and services, seasonally adjusted, widened from December's revised total of $24.6 billion. Further, it expanded 73% from the previous January's figured.

The data reinforced trends seen in a government report released last week showing that the current-account deficit, a broader gauge of trade, hit a record $338.92 billion in 1999.

Perhaps most notably, in the current political climate, the U.S. trade deficit with China rose to $6.03 billion for the month, 24% wider than a year earlier. Exports to China rose 12% year over year but were outstripped by the 22% increase in imports from the mainland.

The news coincides with the Clinton administration's push on Capitol Hill to secure permanent normal trading status for China. That is an integral part of last year's accord, under which China would grant U.S. companies greater market access in exchange for membership in the World Trade Organization.

"Passing permanent normal trade relations can only improve our trade with China, because our market stays just as open either way, but a 'yes' vote will dramatically open China's market to our exports," said White House economic adviser Gene Sperling.

The administration continues to wrestle with China-trade opponents on both the right and left but won a concession Tuesday when House Majority Leader Dick Armey of Texas said he was willing to set a date for a vote. Clinton officials believe such a move would put pressure on wavering Democrats. "If setting a date certain helps us ... get those votes, then I'm certainly willing to do it," Mr. Armey told reporters.

The overall trade report, however, is likely to encourage critics of trade accords, especially among unions who fear jobs will move overseas.

Still, the expanding trade gap highlights a question that has loomed over the U.S. economy for years: How long will foreigners be willing to lend the U.S. money to finance American imports? The answer could spell the difference between a gentle reversal of the deficit as foreigners buy more U.S. goods, and a rough landing accompanied by a weaker dollar, flight from U.S. financial markets, inflationary pressures and rising interest rates.

"So long as the U.S. has a very healthy rate of return on investments in U.S. enterprises, we'll continue to attract the financing we need to carry the trade deficit," said Robert Shapiro, undersecretary of commerce for economic policy.

The ever-growing demand for imports shows that U.S. consumers and businesses are still shopping with abandon. Many analysts expect the Fed to raise rates at least once more in order to slow the economy and stem any incipient inflationary pressures.

US record trade deficit

BBC 15 March, 2000

The US economy is sucking in imports at an alarming rate The downside of the US economic boom was in evidence on Wednesday when the US economy posted its biggest-ever trade deficit.

The total current account deficit, the broadest measure of the trade deficit, reached $338bn, more than $100bn more than the previous year.

The rise of 53%, from $220bn in 1998, threatens to rekindle protectionist pressures in the United States during the Presidential election year.

It also poses a threat to the viability of the economic boom - the longest in economic history.

The 1999 current account deficit, which measures the flow of goods and services, set records in all four quarters, ending with a deficit of $99.8bn in the fourth quarter of the year, at least $5bn higher than expected by analysts.

The total deficit on goods alone was $347bn, while the surplus on services like travel, tourism and insurance continued to shrink.

Unsustainable boom

The reason for the deficit was the booming US economy, which has been sucking in overseas imports at an alarming rate.

The US economy grew at an annual rate of more than 6% in the last quarter of 1999 - a rate that the central bank, the Federal Reserve, believes is unsustainable.

But the efforts to slow down the economy may be hampered by the vulnerability of the dollar to a sudden slowdown.

The US also has a big deficit on its capital account, which has made it the world’s largest debtor nation.

So a sudden collapse of the economy could cause foreigners to withdraw their money that is currently invested in the US stock market, causing the currency to fall sharply.

A sharp fall in the dollar, however, would accelerate that capital flight, as foreign assets in the United States would become less valuable.

Worrries about the dollar are one reason that the Fed is proceeding cautiously about slowing down the economy.

But it is still expected to raise interest rates by 0.25% when it meets next week.

In the long run, a slowdown in the US economy will reduce the trade gap by reducing imports.

But, as the US experience in the l980s shows, that can take rather a long time to work through - leaving a tricky passage for the economy to navigate.

För en mer troskyldig förklaring till USAs ekonomi - klicka här för Mats Johansson om Moses-teorin

THE WALL STREET JOURNAL March 16, 2000

The U.S. current-account deficit, the broadest measure of the imbalance in the nation's foreign trade, totaled $338.92 billion last year, a record and 50% wider than 1998's deficit.

The report came as the Labor Department released data showing that import prices, led by oil, rose 1.9% in February, the biggest monthly increase in more than nine years. The surge raises chances that the days when cheap foreign goods and commodities helped to restrain U.S. inflation may be waning.

The current-account deficit also hit a record in the fourth quarter, reaching $99.78 billion, wider than a revised $89.09 billion during the prior three months, the Commerce Department's Bureau of Economic Analysis reported.

The gap was larger than many analysts expected, and will likely complicate the Clinton administration's already-difficult campaign to win congressional support for permanent normal trading status for China. Labor unions, in particular, are likely to seize on the numbers as evidence foreign trade threatens U.S. jobs, despite an unemployment rate of just 4.1%.

House Ways and Means Committee Chairman Bill Archer (R., Texas) urged President Clinton to make a prime-time, televised appeal to win public support for the China deal. "He can do this, he must do this, because without his involvement our historic opportunity will be lost," Mr. Archer told a business audience.

Most economists see the trade deficit as a result of big differences in economic performance between the booming U.S. economy and the weaker economies of Japan and, to some extent, Europe. As Americans prosper, they import more, while foreigners invest their money in the U.S. financial markets and companies.

But economists also say that the U.S. can't borrow abroad to finance its spending on imports forever. The question is whether that shift from deficit to surplus will occur gradually and benignly, as foreign economies grow and foreigners buy more U.S. exports, or suddenly and painfully, as the dollar falls, foreigners pull their money out of U.S. stocks and bonds, prices rise and interest rates increase.

"I do find it quite troubling, not only the numbers, but also the view that things can gradually correct themselves without any recognition that the trade deficit is a problem," said Dimitri Papadimitriou of the Jerome Levy Economics Institute at Bard College, Annandale-on-Hudson, N.Y.

Not all economists are so pessimistic. Many believe that the Federal Reserve can ease back growth in the U.S. economy, cutting demand for imports as foreigners buy more American products and services. "Overall, these are awful numbers, but they do not guarantee either higher rates or a weaker dollar in the near term," wrote Ian Shepherdson, chief U.S. economist at High Frequency Economics Ltd., a Valhalla, N.Y., research firm.

Foreigners still seem inclined to put their money here. The Commerce Department said that foreign direct investment in the U.S. -- foreigners' purchases of plants, offices and companies -- reached a record $277.51 billion last year, compared with $188.96 billion in 1998.

But with every record current-account deficit, worries grow about how long the combination of low unemployment, low inflation and strong growth can last. U.S. exports of goods and services rose to $251.1 billion in the fourth quarter, but were still outstripped by imports of $326.6 billion. The goods-and-services deficit widened to $75.5 billion from $72.6 billion in the third period.

The current account measures trade in goods and services, plus investment flows and spending on foreign aid. The 1999 figure measures 3.7% of gross domestic product, surpassing a high set in 1987.

Another factor clouding the U.S. economic outlook is the rise in import prices. The strong dollar and low commodity prices have been major factors contributing to low inflation in the U.S. Fed Chairman Alan Greenspan has warned that the central bank will remain "vigilant" about combating inflation. Indeed, the Fed has raised interest rates four times since June in an effort to cool the torrid economy, and many analysts expect another rate increase this month.

Fed concerns about rising prices are likely to be fueled further by the fact that February's import-prices increase was the largest in over nine years. Export prices, meanwhile, rose 0.5%, the biggest gain since April 1996, after climbing 0.1% in January.

"The sharp increase in import prices will have an adverse impact on the dollar," Chase Securities Inc. warned its clients.

Most of the 1.9% increase in import prices stems from the ongoing run-up in petroleum-import prices, which jumped 13.9% last month. The total cost of U.S. petroleum imports has skyrocketed 168.4% since February 1999.

Even without petroleum costs, import prices rose a stronger-than-expected 0.3% for the month, the largest gain since November and the second highest increase of the past 12 months. In January, by contrast, import prices declined 0.1%.

Record US trade deficit of $271.3bn

casts shadow over booming economy FT, 2000-02-19 The US trade deficit

narrowed slightly in December on the back of improved exports but easily

reached a new all-time high of $271.3bn for the year fuelling concerns that the

imbalance could eventually destabilise the surging US economy. FT, 2000-02-19

U.S. Trade Gap Narrowed To $24.1 Billion in August

Wall Street Journal, October 20, 1999

The U.S. trade gap narrowed in August amid signs that shipments of goods abroad continued to improve. The gap in goods and services shrank 3.2% to $24.1 billion, its lowest level since May.

Perhaps more importantly than the overall number, however, was the third straight gain in exports of goods. Exports rose 3.7% to $82.03 billion in the report, a sign that demand from overseas markets is on the upswing after the global financial turmoil seen last year.

Imports increased as well in August, as they have in each month of 1999. Commerce said imports grew 2% to $106.12 billion.

The July trade deficit was revised downward to $24.89 billion from the previously reported $25.18 billion.

Civilian aircraft exports totaled $3.46 billion in August, up from $1.79 billion in the month before, while industrial supplies and materials exports were $12.47 billion, up from $11.53 billion in July.

The import gain was led by petroleum products and autos and auto parts, Commerce said. Leading the way were $4.94 billion in crude oil imports. Automotive imports totaled $15.84 billion in August, up from $15.47 billion in July.

The trade deficits with the major U.S. trading partners were mostly higher. The exceptions were Japan and the 11 countries that adopted the euro currency earlier this year. The gap with the euro member countries fell to $3.97 billion in August from $5.28 billion. The trade deficit with Japan slipped to $6.39 billion from $6.78 billion in July. But the trade deficits with China, Mexico and Canada all went higher in August.

The politically sensitive gap with China rose to $6.87 billion, the highest monthly deficit with any country since the Commerce Department began tracking trade with individual nations.

The gap with Canada increased to a record $3.51 billion from $3.09 billion, while the deficit with Mexico increased to $2.17 billion in August from July's $2.11 billion level.

Bloombergs, 21 Sep, 1999: U.S. Trade Deficit Unexpectedly Widens in July, Hits Record $25.183 Bln

The U.S. international trade deficit in goods and services unexpectedly widened in July to a record, as consumer spending drove up imports.

The deficit grew to $25.2 billion for July from $24.6 billion in June. Analysts had expected a July deficit of $23.8 billion.``It's the strong U.S. economy pulling in imports that's ballooning the trade deficit,'' said Rosanne Cahn, chief equity economist for Credit Suisse First Boston in New York.

U.S. exports also rose, helping U.S. companies and still reflecting an improved global economy.

The dollar and bonds fell after the report, which showed a record trade gap of $6.8 billion with Japan and suggested U.S. demand could overheat the economy. That added to speculation Federal Reserve policy-makers would have to raise interest rates a third time this year to keep inflation in check.

``The booming trade deficit poses all sorts of problems for the Fed,'' said Christopher Low, an economist at First Tennessee Capital Markets in New York. ``We cannot export out of it. We are already producing just about as much as we can.''

The trade deficit with China also set a record, widening to $6.3 billion. The U.S. posted record trade deficits with Canada and Western Europe as well.

The dollar fell to 104 yen from 106.15 yesterday.

Imports of goods and services rose 1 percent to a record $104.2 billion during July, led by oil, consumer goods, aircraft and autos.

Exports rose 0.5 percent to $79 billion in July, the highest in eight months, led by semiconductors, medical equipment, oil drilling rigs and consumer goods.

Through the first seven months of the year, the deficit totaled $143.9 billion. That's up from $90 billion during the first seven months of last year.

At that current pace the trade deficit for all of 1999 is on target to top last year's record of $164.3 billion, by $80 billion, reflecting strong import demand.

Consumer spending has been fueled by the lowest unemployment rate in three decades, rising incomes, low inflation and historic stock markets gains.

The merchandise deficit with Japan rose to a record $6.8 billion in July from $6.3 billion during June and $5.2 billion in July 1998. The yen has climbed 17 percent against the dollar since a low on May 20.

While the dollar has fallen 29 percent against the yen from a peak of 147.26 on Aug. 11, 1998, its value is off only 8 percent over the same period on a trade-weighted basis as measured by the Federal Reserve. That index is adjusted to account for the amount of trade the U.S. conducts with 17 other large countries.

The U.S. imports more than half its crude oil. World oil prices have doubled this year as producers made much of their promised production cuts, reducing a glut that pushed crude oil to a 12-year low last December.

The deficit with Western Europe rose to a record $6.8 billion.

Wall Street Journal, September 21, 1999. Trade Gap Widens to $25.2 Billion As Imports Continue to Flood U.S.

Financial markets are likely to take the data badly, as they imply an even worse current-account deficit in the third quarter and still mighty rates of domestic consumption.

The U.S. dollar dropped sharply last week after news of the record $80.67 billion current account deficit in the first quarter, could fall again. A weaker currency helps to redress a trade deficit because it makes imports relatively more expensive.

Analysts had expected the deficit to narrow for the first time since April to around $23.7 billion.

Current account deficit worse than 1998 record

The deficit

in the USA's current account climbed 17.5% in the April-June quarter, above the

first quarter imbalance of $68.7 billion, which had also been a record.

The current account is the broadest measure of trade because it includes not only goods and services, which are tracked in monthly government reports, but also investment flows and a category that includes U.S. foreign-aid payments.

The deficit is running at an annual rate of $299 billion, far surpassing the imbalance for all of 1998 of $220.6 billion, the biggest deficit in history.

The big rise in the current account deficit in the second quarter was

led by a 14% increase in the deficit in goods, which climbed to $84.6 billion

in the spring.

U.S. goods exports increased 0.9% with manufactured goods

and farm exports both showing increases.

However, this small improvement

was swamped by a 4.9% rise in imports, led by a sharp increase in world

petroleum prices.

The U.S. still had a surplus in services, covering such

things as airlines fares and insurance sales, but it declined to $19.6 billion

in the second quarter, down from $20.2 billion in the first quarter.

The

deficit in investment earnings edged up to $4.4 billion in the second quarter,

from $4.3 billion in the first three months of the year, while a category that

includes U.S. foreign aid rose to a deficit of $11.3 billion in the second

quarter, up from $10.3 billion.

U.S. Trade Deficit Unexpectedly Widens in

June to Record $24.6 Billion

Bloomberg, 19 Aug,

1999

Trade Gap Hit Another Record, Widening to $21.34 Billion in May

Wall Street Journal, July 20, 1999

The U.S. international trade deficit widened in May, hitting another record as foreign oil prices jumped and U.S. exporters were battered by weak global demand. (RE: Efterfrågan? Är det inte strukturellt?)

The Commerce Department reported Tuesday that the trade deficit widened to $21.34 billion, 14.8% wider than the revised $18.6 billion deficit in April.

Imports of goods and services climbed 2.2% to a record high of $98.9 billion in May, reflecting higher oil prices and a big jump in auto shipments.

At the same time, U.S. exports fell 0.8% to $77.6 billion as demand dropped sharply for commercial aircraft, farm products and U.S.-made autos.

Exports were also hindered by the strength of the dollar, which makes U.S. products more expensive relative to foreign goods and therefore less competitive on global markets.

For instance, the trade deficit with the 11 European countries using the euro, which has been suffering a steady decline, rose to $2.74 billion in May.

For the year-to-date, the gap was $11.38 billion, far wider than $7.99 billion in the same period in 1998.

So far this year, the U.S. trade deficit is running at an annual rate of $225 billion, more than one-third wider than last year's $164.3 billion, which had been a record gap.

At the same time, however, the strong import numbers gave the latest evidence of this year's consumer spending spree. Personal spending grew at a 6.7% annual pace in the first quarter and analysts expect that they slowed only somewhat in the second quarter, to around a 4% yearly pace.

In May, the price of crude oil jumped to $14.54 a barrel, up from $12.71 in April and the highest price since December 1997. Rising crude prices offset a smaller volume of imported oil as the bill for foreign oil rose 12.8%, to $5.3 billion.

With the exception of Japan, the trade picture with most of the U.S.'s largest trading partners worsened, presenting a problem for the Clinton administration, which is facing calls for protection from the U.S. steel industry, among others.

The politically troublesome U.S. deficit with China jumped by 9.7% in May to $5.3 billion and this year is running 16% above the same period in 1998.

The U.S. deficit with Japan shrank by 6.7% in May to $5.3 billion, but for the first five months of this year is still running 6.5% above the 1998 levels.

The May deficit with Western Europe rose to $3.6 billion, the biggest imbalance since July 1998. Rising trade tensions with Europe have led the Clinton administration to impose economic sanctions on more than $300 million in European luxury imports in disputes involving U.S. banana companies and beef producers.

The deficit with Mexico in May climbed to $2.2 billion, the second-highest level on record.