Home - News - Alan Greenspan - Real Interest rates - New Era - Economics - EMU - Cataclysm - Contact

US Trade Deficit - Dollar - Egobest

2001-05-21

U.S. Trade Deficit:

Causes, Magnitude and Consequenses

"Shop until the exchange rates of the dollar drop"

Stein's Law: If something cannot go on

for ever it will stop.

Herbert

Stein The Public Interest nr 97 Fall 1989

The optimists will be right until they are wrong.

Wolfgang Munchau

Financial Times 11/12 2006

Some facts -

We have a problem - We have a big

problem - We have no problem -

It is not the End of the World

Conclustion

These imbalances simply can't go on forever.

How long can the global economy endure America's enormous trade deficits or China's growing trade surplus of almost $500 million a day?

- the United States borrows close to $3 billion a day -

Joseph E. Stiglitz, Herald Tribune, October 3, 2006

It cannot go on forever. The question is how and when it will stop

There are risks of a much more abrupt reversal, triggered by a big increase in protectionism in the US, a sudden decline in the world's demand for US assets or, more probably, both together. This could generate a sharp slowdown in the US and the rest of the world, possibly even a world recession.

We do know that the explosive increase in US current account deficits cannot continue indefinitely. It is possible that a smooth adjustment will indeed occur. It is also quite likely that the ultimate adjustment will be both swift and brutal.

Martin Wolf, Financial Times 8/10 2005

So what will happen? Nobody knows.

Asking about the implications of a dollar collapse is a different ball game from predicting its likelihood or timing.

Instead of hopeless crystal ball gazing we can ask what this event would mean and what kind of policies should be adopted in response.

Samuel Brittan, Financial Times, 16/6 2006

Latest charts at Wall Street Journal - Ed Yardeni US Charts - Fed Charts

Why is the

external value of the euro currently low?

By Giancarlo Corsetti

University of Bologna, Yale and CEPR

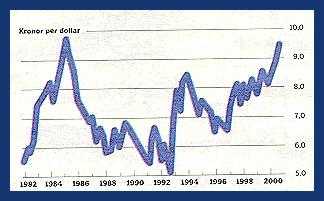

USD/SEK 1982-2000

Dollar puzzle

Financial Times Editorial, March 22, 2001

The recent performance of the dollar against the euro is, to put it mildly, puzzling. The US economy is flirting with recession and US interest rates are down 1.5 percentage points. So why has the dollar been so strong? Since the start of the year, the euro’s value has fallen back below Dollars 0.90 from Dollars 0.95: the dollar is at a 15-year high on a trade-weighted basis.

Well-rehearsed reasons for past dollar strength against the euro no longer apply. First, relatively poor economic growth in Europe can no longer be blamed. Published growth rates and economic forecasts have fallen by more in the US than in the euro-zone.

Second, US interest rates have declined relative to those in the euro-zone, both at the short and long end.

Various other explanations for the dollar’s strength have been doing the rounds. Perhaps the currency markets expect a short US downturn, and are already looking towards the green fields beyond.

Maybe US and Japanese investors have been selling their European equities first.

Perhaps investors still see the US as a safe haven in turbulent times.

Theoretically, the currency markets might expect large US tax cuts to push up real interest rates as they did in the early Reagan years.

None of these explanations holds water, particularly as they are not consistent with moves in other financial markets.

For Europe, a weak currency is not much of a concern. It helps exports and should not seriously affect thinking at the European Central Bank.

For America, a strong dollar is more problematic. It means the US will find it harder to mitigate its downturn through higher exports. But policymakers cannot call for a gradual dollar decline for fear that things might get out of hand.

So the strength of the dollar seems to defy explanation. But so - until recently - did the enduring strength of equity markets. There must be a chance that soon, with some trigger, the dollar will fall from grace.

Some facts -

We have a problem - We have a big

problem - We have no problem -

It is not the End of the World - Conclustion

Back

Home

BIS says in its 70th Annual Report: I. Introduction: old problems in a new era?, dated Basel, 5 June 2000 that a further reason for tempering optimism is that many of the imbalances and structural deficiencies which had characterised the global economy in the previous few years came no closer to being redressed. Indeed, in some respects they worsened.

Foremost amongst these imbalances was the unprecedented gap between the record high rate of private saving in Japan and the record low rate in the United States.

While shifts in fiscal positions moderated the impact of these extremes, albeit at the cost of a steep deterioration in the public finances of Japan, large current account imbalances remained, carrying risks of exchange rate consequences.

The divergence in the saving behaviour of the US and Japanese economies was mirrored in the record US current account deficit and the persistently large Japanese current account surplus.

Indeed, the US deficit rose to a record high as a proportion of GDP.

To read more click on "I. Introduction: old problems in a

new era?"

Full text

- Will the American consumer's willingness to borrow and spend finally be the downfall of the economy? The Organisation for Economic Co-operation and Development, in its Economic Outlook on Thursday, investigates whether overindebtedness in the US is a risk to the global recovery. While there are some worrying signs, US households are not in such bad shape as some measures might suggest, Financial Times wrote on May 3, 2001 under the heading "An expansion bought on credit" .... more

- Think the unthinkable. Suppose the US economy were to fall into recession. The probability is uncertain, but bigger than zero. Since it is good to be forearmed, let us examine what this might mean for the world Martin Wolf wrote in Financial Times, December 13, 2000:

Provided the US trade adjustment occurred over a few years, most countries should easily avoid recessions caused directly by changes in trade balances.

The second channel would be a weak dollar. If inward capital flows were interrupted, as seems probable, the dollar could fall by a third, or even more, against the yen and the euro. Similar declines have occurred in the past.

The fall would be accelerated by the inevitable reduction in short-term US interest rates.

The euro-zone would also be squeezed by a falling dollar. But it is in a far more comfortable position than Japan. Provided the European Central Bank cut interest rates promptly, it could shield the euro-zone and help stabilise the world economy. .... more

On March 6, 2001 he wrote about, Wim Duisenberg, the president of the European Central Bank, who had told the European parliament there are at present no convincing signs that the slowdown in the US economy is having significant and lasting spill-over effects on the euro area economy.

Yet a sustained slowdown in an economy that generates nearly 30 per cent of global output is bound to have significant effects on much of the world. Once upon a time, pundits insisted that the business cycle was dead. Now they argue that any slowdown will soon pass. They are likely to be wrong yet again. .... more

Very important article

German handicap (Martin Wolf, Financial

Times, March 31, 1999):

Few have realised the most dangerous feature

of EMU: it has locked Germany into a seriously uncompetitive real exchange

rate. .... more

United States can continue to sustain current account deficit;

the capital account surplus is more problematical

Institute for

International Economics

March 2001

In 1999, Institute Senior Fellow Catherine L. Mann concluded in

Is the

U.S. Trade Deficit Sustainable? (published September 1999)

that the

current account deficit was sustainable "for two to three more years" but the

trajectory for that deficit meant that it was ultimately not sustainable. A

sustainable trajectory would require a change in the underlying fundamentals of

household savings rates and international liberalization of services, as well

as faster global growth than projected.

At an Institute luncheon on 1 March

2001, Mann presented a follow-up on the issue. She concludes that the current

account deficit remains sustainable but capital account sustainability is

questionable ....

more

Samuel

Brittan: Watch the dollar, not the euro

Financial Times, October 12,

2000

The biggest flaw in the world economy is the US current account deficit, which could place a strain on the currency

So far a hard landing has been avoided. But if US equities were too high in 1998-99, they are still too high today. While most market commentators have warned about the inflationary implications of Wall Street’s behaviour, a minority of discerning commentators including Wynne Godley of Cambridge, Bill Martin of Philips & Drew and the Clare group of British economists, have worried much more about the threat of an ensuing recession if US savings recover to a normal level.

According to the official national accounts, a large private sector deficit in the US is offset partly by the government budget surplus and partly by the overseas inflow.

One version of the argument is that the US private sector has been willing to spend above its income because of the wealth effect from rising equity prices and real estate values. If the asset boom comes to an end, the fear has been that savings would return to normal, and slump rather than overheating would be the problem. .... more

The US currency is creating policy problems around the world Alan Beattie and Christopher Swann wrote in the Financial Times; Apr 5, 2001:

- Strategists are almost unanimous that the dollar is overvalued. Consensus Economics, an economic pollster, says the average prediction is for the euro to rise towards 1:1 parity with the dollar by the summer. Without such a correction, the dollar's strength is creating policy problems and exacerbating imbalances around the world. At home, it means the weakness of domestic demand is compounded by US exports becoming less competitive, threatening continued large trade deficits and further falls in business confidence.

Extreme and rapid moves in currencies, such as the sharp dollar-yen swings during the Asian crisis, contribute to a drying up of financial markets and uncertainty among companies, investors and consumers. But the longer the dollar goes on defying gravity, the greater the imbalances become and the further and faster the currency may have to fall. .... more

The Commission was created in the Omnibus

Appropriations Bill signed into law on October 21, 1998. The Commission has a

one-year life dating from the date of the first technical meeting to be held in

Washington, DC on August 19, 1999.

The Commission will examine and report to

the President, the Committee on Ways and Means of the House of Representatives,

the Committee on Finance of the Senate, and other appropriate committees of

Congress

Two other interesting reports from the Commission are:

Macroeconomic Consequences and Implications of the U.S. Trade and

Current Account Deficits

By

Allen Sinai, Ph.D., Chief

Global Economist, Decision Economics, Inc. -- December 2000

downloadable pdf from

http://www.ustdrc.gov/research/research.html

and

The U.S. Trade Deficit: A View from Europe

By Dr. Karl H. Pitz,

Center Agenda Consulting,

Frankfurt, Germany and Washington, DC - October

2000

downloadable pdf from

http://www.ustdrc.gov/research/research.html

Will the American consumer's willingness to borrow and spend finally be the downfall of the economy, asked Gerard Baker in Financial Times, April 26, 2001

The second uncertainty is in the international outlook. For the past five years the US has been the principal engine of global growth. But with growth this year expected to be about 1.5 per cent, it is now the US that needs strong expansion elsewhere. This would help its exporters offset some of the domestic weakness and reduce the US current account deficit. The latter currently runs at about 4 per cent of gross domestic product, which constantly threatens the dollar’s strength. But Japan is in recession, with a threat of worse to come.

Meanwhile Europe, for all the confidence of central bank officials that they can avoid the worst effects of the US slowdown, is unlikely to remain immune. Without stronger growth in Europe, the US and the world face both weak economic conditions and current account imbalances among the world’s main economic blocs. This could have a destabilising effect on the world economy. .... more

Ernest H. Preeg, senior fellow at the Hudson Institute in Washington, wrote in Financial Times, August 5, 1999 about what he called "The Deficit Trap":

The US current account deficit could reach a record $350bn this year, the 18th deficit in a row. The accumulation of deficits means the US is likely to be a net debtor to the tune of $2,000bn early in the next decade, despite having been a $350m net creditor in 1980.

The country's foreign debt is equivalent to 20 per cent of gross domestic product, and could reach 30 per cent by 2005. Yet many - perhaps most - observers think this is nothing to worry about, and could even be beneficial to the US. I disagree..... more

Stephen Roach is chief economist and director of global economics at Morgan Stanley. In two articles he has issued serious warnings.

In "Prepare for a hard landing"Financial Times, November 23, 2000, he wrote that the risks of a hard landing, or an outright recession, are high and rising - especially in the US. I would assign a 40 per cent probability to such an outcome in the first half of next year. For me, that is tantamount to maximum alert.

In "The shape of the US recovery" FT.com site; May 15, 2001, he referred to the popular play the alphabet game about predicting the shape of the coming recovery in the US and the global economy. My vote is for an American-style L, he wrote and man some disturbing comparisons with Japan.

*

If we had a New Era things could perhaps not be so dangerous. But if the United States economy is an ordinary, even if big, Bubble, we might soon live in interesting times.

For a brief description of earlier bubbles, see "Bonfire of the

insanities The Economist, September 25, 1999:

Some economists believe that

there is no such thing as a bubble because markets are always rational and

efficient. But history suggests otherwise. In their time, tulips, canals,

railways, gold, silver, property and share prices have all bubbled up and then

gone “pop”. Each time investors convince themselves that this time it

will be different. It never is. .... more

One part of the New Era Paradigm was the fast rise in productivity.

Everett Ehrlich, president of ESC Company, an economics consulting firm, and former undersecretary of commerce for economic affairs, questioned that in an article, The mystery of the missing millions in Financial Times, Mar 7, 2001

And The Economist wrote 2001-05-10 that America's productivity declined

The announcement on May 8th that America's productivity declined in the first quarter of 2001 at an annual rate of 0.1%, compared with growth of more than 5% during the year to June 2000, is a blow for the IT-powered new economy. One by one, its claims to be special are being exposed as myths. Now it seems that the widely-held belief that America's sustainable rate of productivity growth had doubled to around 3% was also mere myth. That does not mean, however, that the new economy was entirely hot air.

Others had been more optimistic, among them Chairman Alan Greenspan, who saw Productivity Continuing Despite Slowdown in Economic Growth, Wall Street Journal, April 27, 2001.... more

History’s biggest credit bubble will

collapse

By KIM EVANS

Financial Times, Dec 19, 2000, LETTERS TO THE

EDITOR

Sir, Prof Rudi Dornbusch has it half right (”A rendezvous with bankruptcy”, December 15). The US does matter - and he glosses over the extent of our problems. Yes, Japan is in parlous circumstances and yes, unless they let their debts liquidate and markets clear, there is no solution on the horizon.

US indebtedness is a much bigger problem. It now exceeds Dollars 2,600bn. The vaunted US surplus is a chimera, as the Federal budget is in deep deficit. Why? The unfunded Social Security and Medicare obligations of the US, coupled with unfunded government workers’ retirement, are a black hole. If there were an actuarial requirement to provide for these obligations, the US budget would show a deficit by one reckoning that pushed Dollars 1,000bn a year.

Since 1995, broad money in the US expanded by Dollars 2,600bn and total credit by Dollars 9,300bn, yet nominal GDP was up only Dollars 2,700bn. In the second quarter of 2000, credit expanded by Dollars 1,400bn, a record pace.

Credit has been growing at 4-5 times the rate of GDP growth. Consumer credit has never been greater, mortgage indebtedness as a percentage of total housing value has never been greater and US corporate indebtedness has exploded as US executives have bought back shares to make their options profitable.

The US debt situation and credit bubble make Japan look prudent fiscally. No amount of Fed legerdemain can overcome the collapse of the greatest credit bubble in history. more

Some facts -

We have a problem - We have a big

problem - We have no problem -

It is not the End of the World - Conclustion

Back

Home

Nothing Wrong with

America's Deficit

John H. Makin, Financial Times, 2000-09-13

The Meaningless

Trade Deficit

National Center for Policy Analysis - NCPA

The

trade deficit is essentially a meaningless statistic. This can easily be shown

by the fact that no one knows or cares what the trade balance is among the 50

states. As Adam Smith explained more than 200 years ago, "Nothing...can be more

absurd than this whole doctrine of the balance of trade."

The U.S. Trade

Deficit: A Dangerous Obsession

By Joseph Quinlan and Marc

Chandler

Foreign Affairs, May/June 2001

America's Record Trade Deficit - A Symbol

of Economic Strength

by Daniel T. Griswold, associate director of

the Cato Institute's Center for Trade Policy Studies

Some facts -

We have a problem - We have a big

problem - We have no problem -

It is not the End of the World

Back

Home

A stock market bubble exists when the value of stocks has more impact on the economy than the economy has on the value of stocks.

John H. Makin, American Enterprise Institute

November

2000

Japan’s Lost Decade: Lessons for America, February 2001

One of the keys to a normal U.S. recovery is to avoid Japan’s serious policy errors of the 1990s. Will the United States Repeat Japan’s Mistakes? It seems highly unlikely that American policymakers will repeat the postbubble mistakes of Japanese policymakers. But difficult problems still face the designers of both monetary and fiscal policy in the United States.

Such mistakes should be easy to avoid, yet a need for caution arises from the fact that such mistakes were made by Japan even with the benefit of lessons provided by John Maynard Keynes’s monumental General Theory of Employment, Interest, and Money, published in 1936, and Milton Friedman and Anna Schwartz’s Monetary History of the United States, published in 1963. .... more

Why the Dollar Is Strong, John H. Makin, May 2001

The rise in the

dollar over the past year by an average of more than 10 percent against other

major currencies has been a surprise to many analysts. The expectation was that

the large U.S. current account deficit, a slowing U.S. economy, falling U.S.

interest rates, and an end to the U.S. stock market bubble would all cause the

dollar to weaken. Many analysts expected that the euro would be the strongest

currency of 2001.

....

more

US have a large trade deficit. It cannot go on for ever. When it stops the dollar will drop. It is disturbing that the only time US had a near zero deficit was in 1992 and the dollar was low against the swedish krona.

Updates can be found at Trends of Trade

This report has been produced by Rolf Englund at IntCom