Martin Wolf, Financial Times, March 31, 1999

Few have realised the most dangerous feature of Emu: it has locked Germany into a seriously uncompetitive real exchange rate

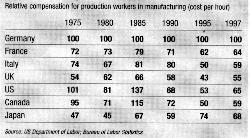

Just how good are German workers? Very good indeed is the answer: well-educated, expertly trained and highly motivated. But are they good enough to offset the cost disadvantage under which they are now toiling?

German production workers are some 50 per cent more expensive than those in any other member of the group of seven leading industrial countries. Worse, because of economic and monetary union, there is little Germany can do about it on its own.

The powerhouse of Europe has fallen into a trap. Its only escape is a weak euro.

The table shows Germany's cost disadvantage with depressing clarity. The data come from the web site of the bureau of labour statistics of the US department of labor.

They show hourly compensation costs for production workers in manufacturing. The costs are converted at actual exchange rates for the year in question and include direct pay, benefits (such as paid holidays) and expenditures on social insurance and contractual benefit plans.

These data are only for west Germany. In 1997, average costs in east Germany were 64 per cent of west German levels. Even so, east German labour was still as expensive as American and French and more expensive than Italian and British.

Moreover, the average hourly cost for Germany as a whole was only 3 per cent below that for west Germany, the reason being that 90 per cent of jobs in manufacturing were in the west.

This uneven distribution of employment is explained, in turn, by the uncompetitiveness of east German manufacturing at post-unification wages.

Three questions arise: Why have Germany's labour costs become so high? Does it matter? What, if anything, can be done about it?

Consider each in turn.

Germany has long been a country of relatively high wages. This, quite properly, reflects the strength of German manufacturing. But since the mid-1980s, its relative competitiveness has deteriorated markedly. This has happened for several reasons: the big decline in the value of the US dollar from its 1985 peak; devaluations within the old exchange rate mechanism of the European Monetary System, most significantly by Italy and Spain; and what French policy-makers refer to as "competitive disinflation".

Germany - of all countries - has lost the low inflation game.

Between 1986 (the year of the last French devaluation) and 1997, French hourly labour costs rose 47 per cent in domestic currency; Dutch labour costs rose a mere 35 per cent. Over the same period, west German costs increased 70 per cent.

Much is made of Dutch success with its reforms. What is most impressive is that in 1980 Dutch and German labour costs were nearly identical. By 1997, Dutch hourly costs were 27 per cent lower.

Turn to the second question. It can be argued that the high cost of labour is unimportant so long as high productivity offsets it. But this point, logically correct, is unconvincing in Germany's case.

One reason is that German output per hour in manufacturing is not high enough to offset the cost disadvantage. The McKinsey Global Institute has estimated that output per hour worked in manufacturing, between 1994 and 1996, was 20 per cent higher in the US and 10 per cent higher in France.* But German wage costs were almost twice US levels and one third higher than in France.

Another reason is that higher measured productivity can be a symptom of the underlying illness. Since companies must earn an internationally competitive return on capital, they dispense with activities (and jobs) in which workers are not productive enough to offset their cost. The significant question therefore is whether all the workers who want to work are employed. In today's Germany, the answer is no.

On the contrary, Germany shows the symptoms of an economy in which companies are adjusting to high costs by dispensing with less productive activities and workers.

What one sees includes: a strong improvement in profitability in the business sector; a faster fall in employment per unit of gross domestic product than in the US, Japan, France or the UK since 1992; a fall of 5 per cent in total employment over this period; and, perhaps most revealing, a modest rise in the stock of inward direct investment, from $111bn in 1990 to $138bn in 1997, but a huge rise in the stock of German investment abroad, from $152bn to $326bn.

Turn then to the third question: is there any way to retain long-term competitiveness without sacrificing jobs?

The answer depends on the efficiency of German workers. For businesses operating in the euro-zone, the issue is whether a given plant will yield returns greater, or less, in Spain or France than in Germany. Unless the German worker can produce 50 per cent more than the French or Spanish, the answer would seem to be "no".

Over time, then, one would expect marginal investment to occur outside Germany. Germany will remain the domicile of internationally strong manufacturing enterprises, but these will increasingly produce abroad.

One popular suggestion for lowering the cost of employing a worker in Germany (and other continental countries) is to reduce social insurance charges. Yet such charges are a lower share of compensation in Germany than in France, Italy or the Netherlands.

The difference between Germany and these countries is in direct pay, not overhead social charges.

Moreover, shifting the fiscal burden from direct charges to general taxation will not necessarily lower labour costs. Workers may react to the higher taxation of income or spending by demanding higher pay.

A second way to lower the cost of labour is via modest rises in nominal pay. Germany would then be playing the "competitive disinflation" game it lost over the past decade or more.

But this is going to be incredibly arduous, at least within the euro-zone. Assume, for example, that inflation averages only 1 per cent a year; that wages in most member countries rise at, say, 3 per cent a year; and that real wages in Germany remain unchanged, implying annual wage increases of only 1 per cent. Even on those wildly optimistic assumptions, it would take over 20 years for German and French compensation to converge.

The third way out is devaluation. But Germany cannot devalue against countries of the euro-zone, which took 42 per cent of its exports in 1997. It has to devalue against other countries. This includes members of the European Union outside the euro-zone - principally the UK, which took 8.5 per cent of German exports.

Germany needs a weak euro. It also needs sterling to enter the euro-zone at as high a rate as possible. But all this depends on whether the European Central Bank, the markets (and, for that matter, the British government) oblige.

The most fascinating feature of the long debate about monetary union is, in retrospect, that it focused so heavily on German demands for central bank independence, low inflation, and fiscal stability. Some attention was also paid to what would happen to peripheral European economies, once they lost the option of devaluation. Few analysts noticed that Europe's most important economy was about to lock itself in at what seems to be a significantly overvalued real exchange rate.

In the run up to Emu, France, Germany's chief rival and partner, has won game and set. But whether it goes on to win the match depends on how Germany responds to its plight.

* McKinsey Global Institute, Driving Productivity and Growth in the UK Economy, October 1998.

The lavish welfare state, financed from levies on wages, has raised average labour costs in the manufacturing sector to €27.60 ($33.70, £18.60) an hour, making German workers some of the most expensive to employ on the planet – Americans cost €18.76, Poles €3.29.

That has shrunk the pool of workers whose pay cheques fund the welfare state to 26m out of a population of 82m, one of the lowest proportions among industrialised nations.

Bertrand Benoit, Financial Times, 16/9 2005

En bilarbetare på Opels fabrik i tyska Rüsselsheim är 50 procent dyrare än sin kollega i Trollhättan

Det visar en sammanställning som Teknikföretagen gjort för Rapport.

Inklusive sociala avgifter blir det 209 kr/tim för en svensk arbetare medan en tysk arbetare kostar 305 kr/tim.

Rapport 7/9 2004

A trap of Berlin's own

invention

This is what happens to a country that enters

a currency union

at an overvalued real exchange rate

By Martin

Wolf

EMU bäddar för bråk

Stefan de Vylder Göteborgs-Posten 2002-10-22

Det är lågkonjunktur i EU. Den allra sämsta utvecklingen hittar vi i Tyskland

"Det faktum att den nominella räntan är gemensam i en valutaunion innebär automatiskt att realräntan blir lägst i de länder som har den högsta inflationen, det vill säga de som skulle behöva en hög ränta, och högst i de länder som skulle behöva stimulera ekonomin. En inbyggd perversitet."

Kommentar av Rolf Englund: Detta är ett inbyggt systemfel i EMU:s konstruktion.

Den förste i världen som formulerat detta i tryck var Stefan de Vylder

The price of a falling

dollar

By Martin Wolf

FT, June 25 2002 20:11

The eagle (the dollar) is

landing

Financial Times, editorial, June 24 2002

”EMU ÄR EN DUM

KONSTRUKTION”

P-O Edin, tidigare chefekonom på

LO

Affärsvärlden, nr 12, 2002-03-20

EU's recovery may have

been washed away

Anatole Kaletsky

The Times, August 29, 2002

Highly recommended

Euron spricker

när dollarn faller

Rolf Englund i EU-krönika i Nya

Wermlands-Tidningen 2001-01-08