News Home

Home - Index -

News - Economics - Cataclysm -

Wall Street Bubbles - Dollar

Houseprices

What Does a Recession Look Like?

A recession is a normal part of the business cycle.

It takes a major policy mistake by a government or central bank to create a depression.

John Mauldin, February 2, 2008

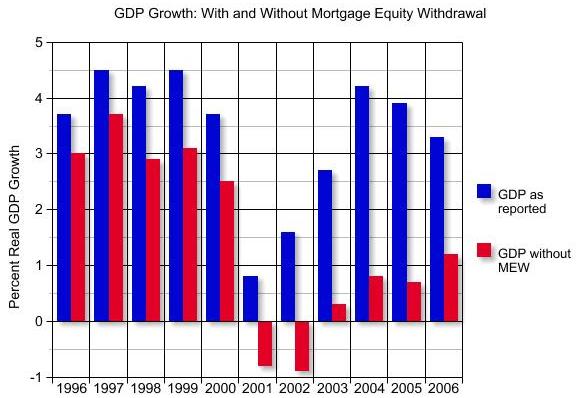

Notice that mortgage equity withdrawals (MEWs) accounted for 2-3% of the growth of overall GDP in 2001-6.

Without MEWs we would have seen two solid years of recession (the red bars) rather than a few quarters, and a decidedly below trend economy.

Such large MEWs were possible because of the bubble in housing prices and

the availability of cheap and easy mortgages.

I think Muddle Through is a perfect description of the economy we will see over the next year or so. So, with that in mind, let's look at what a recession looks like.

I have already lived through 5 recessions. And every one was different in nature and cause.

It is likely most of my readers, all except the youngest, have lived through at least 2 recessions

Congress can't repeal them, and central banks can only fight them, but not prevent them entirely.

Clearly, though, they can mitigate the immediate problem

(although the Austrian school of economics, otherwise known as the take-your-medicine-now school, contends that any such actions simply postpone the Day of Reckoning).

Today we are watching a slow motion bursting of the housing bubble.

Predictions of 2,000,000 homes in foreclosure made in late 2006 in this letter no longer look ridiculous. No wonder that many (including your humble analyst) forecast a drop of 20% or more in home values.

Further, there are 2.18 million homes that were vacant and for sale in the 4th quarter. We are edging ever closer to a national average of 12 months supply of homes for sale this spring,

with many more home owners who would like to sell simply not bothering to list their home.

While MEWs will not go away, especially with low rates coming back, they are not going to be the consumer spending force they have been.

Recessions are also associated with rising unemployment, and this one will prove to be no exception.

Why won't we go back to the 9-10% unemployment of recessions in the 70's and 80's?

Because we have shipped the cyclical manufacturing jobs offshore.

It is my contention that there are very long term cycles in the stock market

And this is important. There has never been a time when valuations dropped to the mean and then went back up again without visiting a much lower valuation.

Never. Not one time. Zip.

We are now back to the mean P/E ratio.

Now maybe this time it is different. But those are dangerous words.

If the stock market were to drop 20%, then the P/E ratio gets to 12, assuming earnings don't fall.

Of course, they will, but they are also likely to rebound as quickly as they did after the last recession.

Now, let me speculate. Go back to 1974.

Were we at the low in terms of valuations at that time?

No, the P/E was 11, which is admittedly low, but it was going to 7 in 1982 (note that took another EIGHT years).

There is a serious effort to figure out how to capitalize the monoline insurance companies. I think it is not unlikely that public money will eventually be brought into play, much like the Savings and Loan Crisis on the late 80's. In short, and no matter what your view is, the Fed and the Treasury are going to do what they have to do to keep the game going.

It is always a mistake to confuse a cycle with a trend.

In the case of corporate earnings, it is worse than a mistake, it is a huge blunder.

The intense cyclicality of corporate earnings is the most important reason why the unadjusted p/e ratio is a worthless indicator of value.

Martin Wolf, Financial Times, March 7, 2007

Huspriserna och recessionen

Rolf Englund blog 3/2 2008