Utdrag ur The Economists ledare 1998-04-18

AN ECONOMIST, it is said, is an expert who will know tomorrow why the things he predicted yesterday did not happen today. So what will be tomorrow’s explanation of why share prices continue to soar today despite frequent warnings from many commentators (including The Economist) that Wall Street is overvalued?

The most popular explanation within America is that it has entered

a new economic era of faster, inflation-free growth, and hence

stronger profits, thanks to new technology and globalisation. We beg

to differ: America is experiencing a serious asset-price bubble.

This week’s spring meetings of the IMF

and the World Bank were dominated by talks about the slump in Japan

and how to prevent another financial crisis like that in East Asia.

These subjects certainly still matter. But it is asset-price

inflation, especially in the United States, that now poses a bigger

and more imminent threat to the global economy.

America’s stockmarket has gained another 15% this year,

taking its total rise over the past two years to a massive 65%. This

is not the only symptom of a bubble: America’s commercial

property market is starting to get frothy, and mergers are running at

record levels

This talk about a “bubble” may seem odd

against the consensus view that the American economy can look forward

to many more years of steady, inflation-free growth.

Rising asset

prices are not necessarily bad. In part, America’s higher share

prices are justified by genuine improvements in performance.

Deregulation, increased competition, better corporate governance, and

more prudent fiscal policy have all played a part—but only a

part.

The boom in share prices has also been fuelled by excessive

monetary growth. America’s M3 money supply

has grown by almost 10% over the past year, its fastest since 1985.

It is true that real short-term interest rates have risen in America

as inflation has declined, but if calculated using the rise in asset

prices rather than consumer prices then real interest rates are

negative.

America’s financial bubble could harm its

economy in two ways. It might suddenly burst, causing financial

instability, destroying wealth and bringing about a recession.

Or asset-price inflation may spread, causing over-investment and a consumer-spending binge as shareholders spend some of their capital gains. The inevitable result would be consumer-price inflation.

In the late 1980s, rapid monetary growth first showed up in asset

prices, but it was ignored, and so inflation spread. There are

already some bad omens. Consumer spending is estimated to have risen

at an annual rate of 5% in the first quarter of this year. There are

some signs of a slowdown, but with unemployment at its lowest rate

for almost 30 years there is no slack left in the economy to absorb

such rapid spending growth.

With hindsight it is clear that

the Fed made a mistake in not raising interest rates last year to let

some air out of the bubble. Pricking a financial bubble is a risky

business, and it is better to act early to prevent one developing.

After fretting about “irrational exuberance” in

December 1996, Alan Greenspan then went quiet. If, in bursting the

bubble, the Fed triggers a recession, it will get all the blame. As

America’s 80m shareholders protest about their shrinking

wealth, it might not be long before Congress acts to curb the Fed’s

power.

Another problem is the enormous uncertainty about when and

by how much interest rates need to be raised to cap asset-price

inflation. There is no way to work out how much of a rise in share

prices is justified by better economic fundamentals.

As the Fed itself says: “There is no means of knowing beyond

question how far this recent rise in stock prices represents

excessive speculation and how far a readjustment of values to

increased industrial efficiency [ . . . ] and

larger profits.” Actually, it was not Alan Greenspan who said

that. This is an extract from the Fed’s minutes exactly 70

years ago, in 1928, on the eve of the Wall Street crash. ![]()

The Fed needs to raise interest rates now. Uncertainty is no

excuse for Mr Greenspan to sit on his hands. In the late 1920s the

Fed was also reluctant to raise interest rates in response to surging

share prices, leaving rampant bank lending to push prices higher

still. When the Fed did belatedly act, the bubble burst with a

vengeance. The longer that asset prices continue to be pumped up by

easy money, the more inflated the bubble will become and the more

painful the economic after-effects when it bursts.

Because the

Fed has again left it rather late, it will be hard to prick the

bubble without risking a recession. If one does come, central bankers

have at least now learnt to ease monetary policy, if necessary, to

prevent a dramatic crash in share prices turning into an economic

depression. One way or another, America’s stockmarket is about

to play a more important role in America’s monetary policy than

at any time since the 1920s.

It would be better if this were to happen sooner rather than later.

The Mess Greenspan Leaves

We can see here how the policy of inflating bubble after bubble to avoid the recessionary implications of previous bubbles has resulted in ever greater imbalances, with the savings rate falling ever lower after each bubble and the debt burden growing ever greater.

More disastrous, however, was the Federal Reserve's attempt to assist Great Britain who had been losing gold to us because the Bank of England refused to allow interest rates to rise

Stefan Karlsson, December 26, 2005

In this context, it seems appropriate to quote "Gold and Economic Freedom":

When business in the United States underwent a mild contraction in 1927, the Federal Reserve created more paper reserves in the hope of forestalling any possible bank reserve shortage. More disastrous, however, was the Federal Reserve's attempt to assist Great Britain who had been losing gold to us because the Bank of England refused to allow interest rates to rise when market forces dictated (it was politically unpalatable). The reasoning of the authorities involved was as follows: if the Federal Reserve pumped excessive paper reserves into American banks, interest rates in the United States would fall to a level comparable with those in Great Britain; this would act to stop Britain's gold loss and avoid the political embarrassment of having to raise interest rates. The "Fed" succeeded; it stopped the gold loss, but it nearly destroyed the economies of the world, in the process. The excess credit which the Fed pumped into the economy spilled over into the stock market — triggering a fantastic speculative boom. Belatedly, Federal Reserve officials attempted to sop up the excess reserves and finally succeeded in braking the boom. But it was too late: by 1929 the speculative imbalances had become so overwhelming that the attempt precipitated a sharp retrenching and a consequent demoralizing of business confidence.

Before he became Fed Chairman, some believers in sound money thought Greenspan might push for a less inflationary monetary policy. They pointed to his past as a close associate of Ayn Rand and author of the "Gold And Economic Freedom" chapter in Rand's Capitalism: The Unknown Ideal.

He also described the events leading to the Great Depression in much the same way that Murray Rothbard did in America's Great Depression.

Gold and Economic Freedom

by Alan Greenspan [written in 1966]

This article originally appeared in a newsletter: The Objectivist published in 1966

and was reprinted in Ayn Rand's Capitalism: The Unknown Ideal

Bank of England raised interest rates to 7 per cent in 1920.

The aim of this was to support the return to the prewar /USD-GBP/ parity.

Coupled with the consequent deflation, the result was extraordinarily high real interest rates.

This, then, was how the self-righteous fools in the British establishment greeted the hapless survivors of the hellish war.

Martin Wolf, Financial Times, 9 October 2012

The UK emerged from the first world war with public debt of 140 per cent of gross domestic product and prices more than double the prewar level.

The government resolved both to return to the gold standard at the prewar parity, which it did in 1925, and to pay off the public debt, to preserve creditworthiness.

Here was a country fit for the Tea Party.

What happens if a large, high-income economy, burdened with high levels of debt and an overvalued, fixed exchange rate, attempts to lower the debt and regain competitiveness?

This question is of current relevance, since this is the challenge confronting Italy and Spain.

Yet, as a chapter in the International Monetary Fund’s latest World Economic Outlook demonstrates,

a relevant historical experience exists: that of the UK between the two world wars.

This proves that the interaction between attempts at “internal devaluations” and the dynamics of debt are potentially lethal.

Moreover, the plight of Italy and Spain is, in many ways, worse than the UK’s was. The latter, after all, could go off the gold standard; exit from the eurozone is far harder.

Again, the UK had a central bank able and willing to reduce interest rates.

The European Central Bank may not be able and willing to do the same for Italy and Spain.

Interndevalvering (Ådals-metoden)

Churchill was appointed Chancellor of the Exchequer in 1924 under Stanley Baldwin and oversaw Britain's disastrous return to the Gold Standard, which resulted in deflation, unemployment, and the miners' strike that led to the General Strike of 1926.

This decision prompted the economist John Maynard Keynes to write The Economic Consequences of Mr. Churchill, arguing that the return to the gold standard would lead to a world depression.

Churchill later regarded this as one of the worst decisions of his life; he was not an economist and that he acted on the advice of the Governor of the Bank of England, Montagu Norman.

From "Churchill: A Biography" by Roy Jenkins

Gold and Strikes, page 399 ff

Norman, the Great Govenor was even more sublimely bland. In the opinion "of

ecucated and resonable men", he wrote, there was no alternative (RE: Den Enda Vägen, således)

to a return to gold. The Chancellor would no doubt be attacked whatever he did but

"In the former case (Gold)he will be abused the ignorant, the gamblers and the

antiquated industrialists; in the latter case (not Gold) /RE: ingen uppskrivnig av

pundet/ he will be abused by the instructed and by posterity."

Source according to Jenkins: Gilbert, Winston S. Churchill, V, p.94

Till en annan kritiker, Otto Niemeyer skrev Churchill, enligt Jenkins

The Treasury has never, it seems to me, faced the profound significance of what

Mr Keynes calls "the paradox of unemployment amidst dearth". The Govenor shows

himslef perfectly happy in the spectacle of Britain possesing the finest credit

in the world simualtanously with a million and a quarter unemployed. Obviously

if these million and a quarter were usefully and economically employed, they would

produce at least GBP 100 a year, instead of costing at least GBP 50 a head

in doles.

RE: Det var i alla fall inte för höga ersättningsnivåer i deras A-kassa.

RE: Därefter lade sig Churchill platt och handlade som rekommenderats av "ecucated and resonable men".

Jenkins skriver härom:

The momentum of conventional wisdom swept them (Keynes-McKenna) away...

a remarkable example of a strong not a weak minister nonetheless reluctantly succumbing,

grudgingly adjustning himself to the near unanimous, near irresistible flow of

establishment opinion.

As a result there was committed what is commonly regarded as the greatest mistake of that main Baldwin government, and the resonsibility for it came firmly to rest upon Churchill. Keynes, for instance, wrote a pamphlet to which, playing on the resounding success of his 1919 The Economic Consequences of the Peace he gave the title The Economic Consequences of Mr Churchill.

Churchill: A Biography by Roy Jenkins

Anne Wibble hade det heller inte så lätt

When Germany entered the euro it made the same mistakes as Britain did

when it rejoined the gold standard in 1925 and re-pegged the pound to the dollar after 1945.

Anatole Kaletsky

The

Times, August 29, 2002

Highly recommended

It is economic performance – not the European Union budget or any proposed constitution – that will determine the fate of the “European Project”.

After all, Hitler came to power in 1933 due to “ordinary economic voting behaviour” when the mainstream parties’ economic agendas were unconvincing, not because a majority of German voters then embraced Nazi ideology.

Adam Posen, Financial Times, August 3 2005

The punitive 1919 Treaty of Versailles leading inevitably to Hitler’s capture of power in a resentful Germany in 1933.

But in The Lights That Failed Steiner challenges this traditional view

The 1920s was an aftermath of the first world war and the 1930s was a prologue to the second, the two decades bordered by the “hinge years” of 1929-33, when the Wall Street crash engulfed Europe in depression

Jackie Wullschlager Financial Times April 29 2005

THE LIGHTS THAT FAILED:

European International History 1919-1933

by Zara Steiner, Oxford University Press £35, 938 pages

about the book at Amazon

By the 1920s most European states had stabilised their currencies and were willing to seek co-operative solutions to political conflicts. The League of Nations was a functioning institution that knit together the international community, world disarmament was actively pursued and Briand suggested in 1929 that “among peoples constituting geographical groups, like the peoples of Europe, there should be some kind of federal bond... primarily economic [which] might also do useful work politically and socially, and without affecting [national] sovereignty”.

Steiner does not dwell on German hyper-inflation of the early 1920s ... but emphasises instead continuing negotiations to diminish the Versailles terms, so that by 1929 Germany was receiving more in US loans than she was paying in reparations.

Germany - an emerging superpower?

Comparisons with the 1930s

Sara Moore [The European Journal, May 2008]

Peace Without Victory for the Allies, 1918-1932

by Sara Moore (Author)

How Hitler Came to Power

by Sara Moore

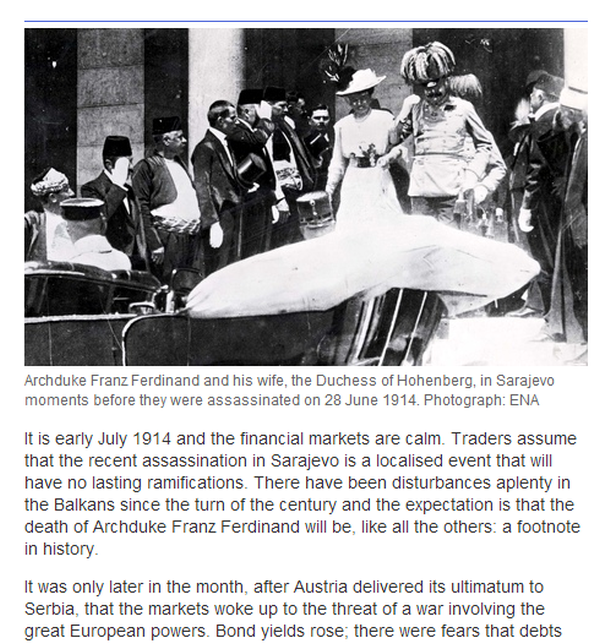

In the heat of the 1914 summer, the financial markets went into meltdown.

Crowds gathered outside the Bank of England. The London Stock Exchange shut on July 31 and stayed closed for five months.

About 50 countries experienced bank runs or market crashes. For six weeks, almost all the world’s stock exchanges were closed.

George Osborne, FT August 3, 2014

I think it is a blunder to use sanctions to give President Putin no choice but folding or fighting.

The blunders of a century ago led to the deaths of more than 10m people, mostly young men, drawn from all over the world.

As we commemorate the outbreak of the first world war, let no one swallow the old but tenacious lie that their “sacrifice” was a necessary and noble one.

On the contrary, the war is best understood as the greatest error of modern history

Niall Ferguson FT, August 1, 2014

Första Världskriget - What caused this catastrophe?

Just How Likely Is Another World War?

The Atlantic 30 July 2014

President John F. Kennedy would remind of his favorite answer, quoting German Chancellor Theobald von Bethmann Hollweg:

“Ah, if we only knew.”

As the best of the new books on this conflict, Christopher Clark’s The Sleepwalkers, concludes forthrightly, the available evidence can be marshaled to support an array of competing claims.

“The outbreak of war in 1914 is not an Agatha Christie drama at the end of which we will discover the culprit standing over a corpse in the conservatory with a smoking pistol,” Clark writes.

“There is no smoking gun in this story; or, rather, there is one in the hands of every major character.”

The Deluge:

The Great War and the Remaking of Global Order, 1916-1931

by Adam Tooze. Review by Tony Barber, FT May 30, 2014

Review by Adam Tooze, Nov. 21, 2014

Ring of Steel: Germany and Austria-Hungary at War, 1914-1918

‘We began the war, not the Germans and still less the Entente,”

Baron Leopold von Andrian-Werburg, a young Austrian diplomat, admitted in December 1918.

Von Andrian-Werburg’s crucial role at a Vienna war council on July 9, 1914, had been to advise his colleagues about the likely response of Russia to a severe Austrian ultimatum toward Serbia.

There were not many European leaders who in the wake of 1914 were willing to make an admission of this kind.

Most tried desperately to avoid accepting their own culpability.

But this sense of shouldering an awesome responsibility was common to the small clique of young Austrian diplomats

who conspired to take their country to war in July 1914.

They knew that they were the only group of decision-makers among the great powers deliberately aiming to unleash a war.

The culpability of Berlin, by contrast, lay in backing their challenge to the Franco-Russian alliance that stood behind Serbia.

In a year crowded with histories of World War I, Alexander Watson’s “Ring of Steel” makes a truly indispensable contribution

in allowing us to see from the inside out this disastrous alliance between Austria and imperial Germany.

Remarkably, his is the first single-volume, English-language history to treat the entirety of the war

from the vantage point of the two countries that led the aptly named Central Powers.

Their allies, Turkey and Bulgaria, were important combatants in their own right, but it was the German-Austrian partnership that widened Vienna’s Balkan entanglement

into a European war, which in turn escalated into a world-wide conflict.

It is a mark of talent in a historian to take familiar narratives and open them to new interpretation. Mr. Watson’s book is a brilliant demonstration of this skill.

RING OF STEEL, By Alexander Watson, at Amazon

The Sleepwalkers: How Europe Went to War in 1914

by Christopher Clark

amazon.com/The-Sleepwalkers

Faktum är att Vilhelm II inte ens var på plats när den kris som resulterade i första världskriget bröt ut

– han befann sig till havs på en sommarkryssning.

Om det fanns en tysk som var mer skyldig än de övriga till att landet bidrog till att första världskriget startade var det kansler Theobald von Bethmann Hollweg

Det är väl alldeles uppenbart vem som startade Första Världskriget?

Kejsaren av Österrike-Ungern - en Habsburgare - undertecknade ordern om angrepp på Serbien.

If you think the human race is a bunch of idiots now, consider what happened a century ago.

A Martian might have gazed down upon Europe in 1914 and seen a peaceful, prosperous continent with a shared culture.

The English listened to Wagner, Germans savored Shakespeare, Russian aristocrats mimicked the French, Mozart and Italian opera were loved by all.

Then, Europe imploded.

The Atlantic 27 July 2014

A hard-hearted peace treaty and a ravaged economy produced a “lost generation” of young Germans and led directly to the rise of Hitler.

The secret Sykes-Picot Agreement reached by Britain and France in 1916 drew arbitrary boundary lines across the postwar Middle East—around Iraq, for instance—that are returning deadly dividends to this day.

Although nobody at the time was aware, the six weeks from Sarajevo to the outbreak of the first world war marked the end of the inaugural era of globalisation that had London and the gold standard at its heart.

There had been occasional panics, some of them serious, but the international economic order seemed as stable and secure as the international balance of power.

It was only later in the month, after Austria delivered its ultimatum to Serbia...

The Guardian, 6 July 2014

The Consolations of Economics by Gerard Lyons; Faber & Faber

Jag tror man kan datera första världskriget till 1860-talet,

kriget Preussen/Italien – Österrike; sedan 1871 Preussens (det förenade Tysklands) förödmjukande seger över Frankrike.

Kriget kunde ha startats i september 1898, i konflikten över Fashoda mellan England och Frankrike.

Eller 1 juli 1911 när Tyskland skickade kanonbåten ”Panther” till Agadir, mot Frankrike.

Nils-Eric Sandberg, Kristianstadsbladet 30 juni 2014

Galenskapen kulminerade veckan 28 juli–4 augusti, med mobiliseringarna och krigsförklaringarna. Men galningarna agerade inte i ett vakuum.

Lundahistorikern Dick Harrison skisserade nyss i Svenska Dagbladet ett optimistiskt kontrafaktiskt perspektiv:

Om Princip missat hade kriget inte blivit av; Hitler hade blivit en hötorgsmålare i München;

Tyskland hade blivit välmående och fredligt; allt hade gått bra.

This year is the 100th anniversary of the start of the first world war,

the 70th anniversary of D-Day and

the 25th anniversaries of the collapse of the Soviet empire and the savage crackdown around Tiananmen Square.

Martin Wolf, Financial Times June 10, 2014

Historian Margaret MacMillan writes in her account of events leading to the great war,

with fewer miscalculations and a different interplay of characters Europe could have gone the other way in 1914.

Margaret MacMillan

The War That Ended Peace: The Road to 1914

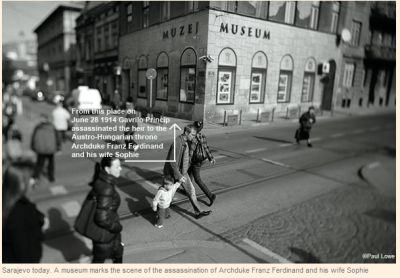

On a street corner here 100 years ago,

a 19-year-old Serb nationalist shot the heir to the Austro-Hungarian throne

and triggered the first world war.

Simon Kuper, FT, 21 March 2014

Cambridge historian Christopher Clark, in his seminal 2012 history The Sleepwalkers: How Europe Went to War in 1914, emphasises the event’s “raw modernity”

“It began,” he writes, “with a squad of suicide bombers and a cavalcade of automobiles” – premonitions of September 11 2001 and Dallas, 1963.

Austrians decided that the motorcade wouldn’t wend its way through the narrow Ottoman town, as per the original plan. Instead it would race along Appel Quay to the hospital.

Regrettably, nobody remembered to tell the chauffeur of the front car.

This bit of “bureaucratic slovenliness”, typical of the Austro-Hungarian empire, made the assassination possible, noted the British historian AJP Taylor.

It is tempting to think about what would have happened had US President Woodrow Wilson adhered to his original resolution to keep the United States out of the war.

Throughout most of the war, the Germans were tactically superior to their opponents.

What they lacked in materiel and manpower they managed to make up through battlefield strategy.

Indeed, in the summer of 1917 France was on the verge of collapse. The number of dead French soldiers had surpassed one million.

Der Spiegel, 7 February 2014

Under Article 231 of the treaty, Germany was forced to concede that it was solely responsible for the war -- a genuflection from which the victorious powers derived their claim for extensive reparations.

After a devastating offensive on the Aisne, in which the French lost 130,000 men within a few days, large parts of the army were refusing to continue fighting. After a flood of court martial proceedings, General Philippe Pétain held out the prospect of no longer engaging in major offensives.

When, on Sept. 27, the Allies penetrated the Siegfried Line, the German army's last defensive position to the West, the Supreme Army Command, under General Erich Ludendorff, knew that the war had been lost. The quartermaster general suffered a nervous breakdown. The next day, he asked the Kaiser to approve the initiation of cease-fire negotiations.

So much for the stab in the back that politicians on the home front had supposedly inflicted on the brave military.

Until 1929, the German economy had managed to keep itself more or less afloat, partly as a result of American investments. Now the creditors from abroad were withdrawing their money, plunging the German Reich directly into the vortex of the Great Depression.

The deflationary policy of Reich Chancellor Heinrich Brüning drove unemployment numbers to well over six million.

Reich Chancellor Heinrich Brüning

The Economic Consequences of the Peace, by John Maynard Keynes, 1919

I Frankrike är minnet av första världskriget däremot högst levande.

11 november då stilleståndsavtalet skrevs under är en dag då nationen enas och då man hedrar de 1,4 miljoner franska soldater som omkom i ”La Grande Guerre”.

Mellan 1920 och 1925 upprättades sammanlagt 36 000 ”Monuments aux morts”, krigsmonument tillägnade de stupade soldaterna och indirekt också de 4,3 miljoner krigsinvaliderna som återvände från slagfälten till ett förstört och ekonomiskt utarmat Frankrike där nästan en tredjedel av bruttonationalprodukten hade utraderats.

Vid dessa minnesmärken hålls varje år flammande tal som erinrar om patriotism, hjältemod och uppoffringar.

Minnet av andra världskriget har däremot en besk bismak av kollaboration med tyskarna och mindre hedervärda kompromisser som gärna sopas under mattan.

SvD 18 Juni 2014

In 1918 50m-100m people were killed by Spanish flu,

compared with 16m in the first world war

The Economist print, April 20th 2013

Despite progress, the world is still unprepared for a new pandemic disease

The risk of such an outbreak turning into a pandemic is low, but the danger, if it does, is huge

Spanska sjukan/Fågelvirus och andra pandemier

Britain entering first world war was 'biggest error in modern history'

Historian Niall Ferguson says Britain could have lived with German victory and should have stayed out of war

The Guardian, 30 January 2014

World War One

Supported by over 500 historical sources from across Europe, this resource examines key themes in the history of World War One.

Click

In the introduction to his book George Kennan tells us,

"I came to see World War I . . . as the great seminal catastrophe of this century - the event which . . . lay at the heart of the failure and decline of this Western civilization."

The Decline of Bismarck's European Order: Franco-Russian Relations 1875-1890

Whole empires were destroyed and societies brutalized.

But there’s another reason the war continues to haunt us: we still cannot agree why it happened.

Or would it never have happened had a random event in an Austro-Hungarian backwater not lit the fuse?

In the second year of the conflagration that engulfed most of Europe a bitter joke made the rounds:

“Have you seen today’s headline? ‘Archduke Found Alive: War a Mistake.’”

That is the most dispiriting explanation of all—that the war was simply a blunder that could have been avoided.

brookings.edu/research/essays/2013/rhyme-of-history

Archduke Franz Ferdinand Lives!

Suppose the heir to the Austrian emperor had not, through various accidents on the day,

become the victim of a Serbian assassin in Sarajevo in June 1914: what then?

Review by Peter Clarke of "Archduke Franz Ferdinand Lives! A World Without World War I"

by Richard Ned Lebow, FT 24 January 2014

Richard Ned Lebow is a prolific political scientist who uses counter-factual hypotheses. Not only does he imagine a “best plausible world” – no Soviet takeover, no Nazi regime, no Holocaust – but he also gives us worst-case scenarios.

Either way, we soon lose sight of the immediacy of the first world war itself and plunge into some far-reaching speculations, great and small alike. Thus Adolf Hitler, the unsuccessful artist, eventually “sets up a successful mail-order business that sells quack products”. Maybe; and yet again, maybe not.

Artikeln behandlar även böckerna

The Long Shadow: The Great War and the Twentieth Century, by David Reynolds

och

First World War: Still No End in Sight, by Frank Furedi

Peter Clarke is author of ‘Mr Churchill’s Profession: Statesman, Orator, Writer’

Kontrafaktisk historieskrivning - Alternate History

http://www.alternatehistory.com/

1968 - Tänk om dom fått igenom sina förslag

Rolf Englund blog, april 2008

The failures of Europe’s political, economic and intellectual elites created the disaster that befell their peoples between 1914 and 1945. The west is not immune to elite failures.

On the contrary, it is living with them. Here are three visible failures.

Martin Wolf, Financial Times 14 January 2014

Highly recommended

In 1914, national leaders were so keen to appear strong and to protect their honour

or “credibility” as they would call it nowadays),

that they were unable to step back from the brink of conflict.

Gideon Rachman, Financial Times, 6 January 2014

Efter första världskriget tvingades Tyskland acceptera den kontroversiella krigsskuldsparagrafen.

Enligt denna bar den tyska riksledningen ansvaret för att kriget började.

På just denna punkt är den moderna historieforskningen enig: så enkelt var det inte.

De tyska förhandlarna i Versailles gick endast med på paragrafen för att de var därtill nödda och tvungna, inte för att de på allvar höll med om dess innehåll.

Österrike-Ungerns politiker beslöt att utnyttja morden politiskt för att stoppa Serbiens ambitioner på Balkan. Den 23 juli sändes ett ultimatum till Belgrad, i vilket man krävde att serberna skulle hjälpa till att utreda mordet och samtidigt gå till aktion mot anti-österrikiska kretsar i landet. Faktum är att serberna gick med på nästan allt, och i Wien borde man inte haft några större problem att inhösta en diplomatisk vinst.

Men österrikarna var inte nöjda – de ville ha krig.

Dick Harrison, SvD, 1 januari 2014

Dick Harrison: Det hade hänt om Sarajevoskotten aldrig avlossats

Miljoner liv hade sparats och Hitler stannat som hötorgskonstnär

http://www.svd.se/kultur/dick-harrison-det-hade-hant-om-skotten-i-srajevo-aldrig-avlossats_3665896.svd

Idag för hundra år sedan förklarade Österrike-Ungern krig mot Serbien,

och den ”svarta vecka” som resulterade i första världskriget tog sin början.

Efter kriget tvingades Tyskland ta på sig en krigsskuld som i efterhand har blivit djupt, och med rätta, kritiserad,

eftersom orsakerna till att kriget började var betydligt mer komplicerade.

Den enskilde tysk som blev mest kritiserad var kejsaren själv, Vilhelm II. Hur skyldig var han egentligen? Drev han personligen på Österrike-Ungern att förklara krig?

Faktum är att Vilhelm II inte ens var på plats när den kris som resulterade i första världskriget bröt ut – han befann sig till havs på en sommarkryssning.

Om det fanns en tysk som var mer skyldig än de övriga till att landet bidrog till att första världskriget startade var det

kansler Theobald von Bethmann Hollweg, som innehade ämbetet mellan 1909 och 1917.

http://blog.svd.se/historia/2014/07/28/hur-skyldig-var-kaiser-wilhelm/

Kommentar av Rolf Englund 2004:

Det är väl alldeles uppenbart vem som startade Första Världskriget?

Kejsaren av Österrike-Ungern - en Habsburgare - undertecknade ordern om angrepp på Serbien.

Rome, Habsburg and the European Union

There are uncomfortable parallels with the era that led to the outbreak of the first world war

The Economist, Dec 21st 2013 print

Globalisation and new technology — the telephone, the steamship, the train—had knitted the world together.

John Maynard Keynes has a wonderful image of a Londoner of the time, “sipping his morning tea in bed” and ordering “the various products of the whole earth” to his door, much as he might today from Amazon — and regarding this state of affairs as “normal, certain and permanent, except in the direction of further improvement”.

The Londoner might well have had by his bedside table a copy of Norman Angell’s “The Great Illusion”, which laid out the argument that Europe’s economies were so integrated that war was futile.

Yet within a year, the world was embroiled in a most horrific war. It cost 9m lives—and many times that number if you take in the various geopolitical tragedies it left in its wake, from the creation of Soviet Russia to the too-casual redrawing of Middle Eastern borders and the rise of Hitler.

Första världskriget var inte nödvändigt

Inför hundraårsdagen 2014 stundar en strid ström av böcker. Få kommer att kunna mäta sig med The Sleepwalkers av Christopher Clark.

Andreas Danielsen, Axess Magasin nr 9, december 2012

Vi fick lära oss att 1900-talets urkatastrof, första världskriget, var oundvikligt. Stormakternas nationalism och kapprustning störtade dem i avgrunden.

Men få historiker köper idag denna förklaring till krigsutbrottet, även om de fortfarande tvistar om de verkliga orsakerna.

Efter snart 100 år och oräkneliga studier om tragedins förspel vet vi i detalj vad som utspelade sig sommaren 1914, men vi är fortfarande förvånansvärt okunniga om varför det hände.

Enligt min mening kan den enda rimliga förklaringen sammanfattas i ett ord: heder. För makthavarna och deras aristokratiska värderingar var krig att likna vid dueller mellan stater.

Franz Ferdinand, rikets tronföljare och framtidshopp, hade mördats på eget territorium av en fiendemakts hantlangare. Attentatet var en exempellös förolämpning av en barbarisk uppkomling mot den anrika monarkin.

Flera av stormakterna kanske snubblade aningslöst mot ruinens brant, men Österrike-Ungern marscherade med berått mod dithän.

Let’s not be beastly to the Germans

Nigel Jones, The Spectator 27 September 2012

The question of how Europe stumbled into the horrific abyss of the First World War, the catastrophe which The Economist once called ‘the greatest tragedy in human history’ is obviously of much more than purely academic interest. (Though it is chiefly academics who have been arguing about it ever since).

As we approach the centenary of the conflict’s outbreak, one of them, Christopher Clark, Professor of Modern History at Cambridge University, has written a magnificently detailed study of the diplomatic dance that led the continent up to and over the edge.

The Sleepwalkers should be required reading for politicians and decision-makers fumblingly steering the world in our own age, an epoch perhaps even more dangerous than the era of 1914.

The Sleepwalkers: How Europe Went to War in 1914, av Christopher Clark hos Amazon

Start of First World War at Intcom

Vi kommer aldrig att bli färdiga med första världskriget

Den totala ringaktning för människoliv som präglade dess generaler,

den kataklysmiska effekt konflikten fick på Europas samhällsordning och

de miljoner och åter miljoner av mänskliga tragedier som utspelade sig i skyttegravar och fattiga soldathem

Dick Harrison, understreckare SvD 28 februari 2012

James Barr’s new book, A Line in the Sand

Review by Patrick Seale, FT August 26, 2011

The story of how Britain and France carved up the Arab world between them after the first world war

has often been told but James Barr’s new book, A Line in the Sand, adds some spice to the usual accounts of this

decisive moment in the history of the Middle East.

It was a cynical act of imperial greed.

I’ve been reading A Line in the Sand, a riveting book by James Barr.

It’s about the incredible manner in which the British and the French re-made the map of the Middle East during and after the First World War.

Barr tells a sordid tale of hubris and eye-popping political skulduggery, as two colonial powers cooked up the Sykes-Picot Agreement of 1916,

dividing Le Moyen Orient along a line drawn from the Mediterranean to the Persian frontier.

Liam Halligan, 21 Jun 2014

The Run-Up to World War One

December 13th, 2010 | Author: Pater Tenebrarum

Europas sista sommar. Vem startade första världskriget?

Till den allt större floran av böcker om kriget 1914-1918 kan vi nu lägga ytterligare två till svenska översatta alster, den amerikanske historikern David Fromkins Europas sista sommar. Vem startade första världskriget? och militärhistorikern H P Willmotts Första världskriget.

Dick Harrison SvD 11/11 (vapenstilleståndsdagen) 2004

Kommentar av Rolf Englund:

Det är väl alldeles uppenbart vem som startade Första Världskriget?

Kejsaren av Österrike-Ungern - en Habsburgare - undertecknade ordern om angrepp på Serbien.

När EU och NATO angrep Serbien med stöd av Anna Lindh, vägrade Österrike att upplåta sitt luftrum åt EU/NATO. I Österrike visste man att det kunde gå illa om man angrep Serbien...

Pappenheim (Vi känner våra pappenheimare)

Tysk kejserlig fältherre; greve. Pappenheim var Tillys närmaste underbefälhavare i slagen vid Vita berget, vid Magdeburgs stormning och vid Breitenfeld samt Wallensteins närmaste man i slaget vid Lützen, där han stupade.

Ordspråk: känna sina pappenheimare: 'känna sitt folk', citat ur Friedrich von Schillers Wallensteins Tod.

-Stålhandske, sade han (Gustav II Adolf) och hejdade sin kolossala mörkbruna springare vid finnarnes sista led - I förstån väl hvarför jag ställt eder ytterst.

Mot oss står Pappenheim med sina walloner.... mer här

Gula Brigadens Hjältar, Pojkarnas Julbok 1944

Habsburg

From Wikipedia, the free encyclopedia.

The terrible price of austerity

Chancellor Brüning's austerity policies went far beyond keeping interest rates high to stay on the gold standard and stem capital flight.

A series of draconian fiscal budgets imposed severe spending cuts and tax rises

Frances Coppola 28 December 2017

Each 1 standard deviation increase in fiscal consolidation was associated with between 2 and 5 percentage point increase in votes to the Nazis or up to one quarter or one half of one standard deviation of the dependent variable.

Yes, I know - correlation isn't causation, and all that. But it clearly isn't possible for causation to be the other way round

Interndevalvering (Ådals-metoden)

Heinrich Brüning

Popular mythology in Germany has it that the Weimar hyperinflation of 1922-23 led directly to the rise of Hitler. This is not true.

Frances Coppola 31 August 2014

The Nazi party was formed soon after the end of the First World War, but it struggled to achieve electoral success throughout the 1920s. In the German election of 1928, the Nazi party only managed to win 12 seats in the Reichstag. Four years later, in 1932, it was by far the largest party, winning 230 seats with 37% of the vote.

What changed during that time?

Brüning used the memory of the earlier Weimar hyperinflation, together with popular hatred of war reparations, to justify extreme austerity measures.

And because the scars left by that hyperinflation are so very painful, he got away with it.

When the Reichstag threw out his austerity budget, it was imposed by presidential decree. Among other things, sickness benefits and pensions were cut, unemployment insurance was reduced and workers were required to pay higher contributions. There was also a brutal internal devaluation caused by deliberately tight monetary policy: during the two years of Brüning's chancellorship wages, salaries, rents and prices fell by 20%. The result was similar to the Hoover/Mellon liquidationism in the US: it made what was already a deep recession triggered by a financial crisis far, far worse. By 1932 unemployment was nearly 30%, RGDP was falling by 8% per annum and everyone had had enough.

Hitler won the 1932 general election with a landslide. The rest, as they say, is history.

Here is an excerpt from a speech given by German Chancellor Heinrich Brüning in 1931, at the height of the Great Depression in Europe

Weimar and Greece

Paul Krugman, 15 February 2015

Weimar, it’s never about the deflationary effects of the gold standard and austerity in 1930-32,

which is, you know, what brought you-know-who to power.

The Nazis only won 32 Reichstag seats in the election of May 1924, and just 12 in 1928.

The Nazi party did not become a popular political force until long after the hyperinflation period ended.

The Economist, November 15th 2013

The tragedy of the interwar years in Germany was that the Social Democrats - then the world’s foremost socialist party -

became fatally tainted by acquiescing in /accepting/ Bruning’s deflation torture from 1930 to 1932.

They did so, of course, because they dared not confront the orthodoxies of the Gold Standard.

The result in Germany was the Reichstag election of July 1932 when the Communists and Nazis won over the half the seats.

Ambrose Evans-Pritchard 23 May 2010

Med sjunkande privata inkomster följde minskade offentliga

skatteinkomster, och 1932 måste kommuner, städer och till

och med en delstat gå i konkurs och ställa sig under

riksadministration...

Då Brünings sparsamhetsiver till

slut också riktades mot statsbidragen till godsägarna

öster om Elbe, tröt /president/ Hindenburgs tålamod,

och den 30 maj 1932 tillträdde en ny regering under ledning

ytterst konservative tidigare centrumpolitikern Franz von Papen. Hans

regering hade praktiskt taget inget parlamentariskt stöd och

förbluffade samtiden genom att majoriteten av ministrarna var

adliga.

Socialdemokraterna fällde regeringen. Därefter utlystes nyval.

To me it is striking to what extent the economic and political situation in Greece resembles that of Germany in the early 1930s.

The Market Monetarisr 13 February 2015

In 1931 the German economy was in a deep crisis with deflation and ever mounting debt – both public and private.

A rigid monetary regime – the gold standard – was strangulating the German economy – while extremist parties on the left and right became increasingly popular among voters.

At the same time the position of French government was uncompromising – Germany’s problems is of her own making. The answer was more austerity and there could be no talk of a new debt deal for Germany.

Full textEMU Replay of the 30´s

nejtillemu

Nationalsocialistiska tyska arbetarepartiet, (Nationalsozialistische Deutsche Arbeiterpartei (info), förkortat NSDAP)

Wikipedia

Överstatligheten ökar

Till framgångarna hör att nyordningen kommer att kunna genomföras relativt snabbt

SvD-ledare 10 december 2011

“The year 1941 will be, I am convinced, the historical year of a great European New Order.”

Adolf Hitler

Reneging on its debt obligations would make the U.S.

the first major Western government to default since Nazi Germany 80 years ago.

John Glover, Bloomberg, Oct 14, 2013

Germany unilaterally ceased payments on long-term borrowings on May 6, 1933, three months after Adolf Hitler was installed as Chancellor.

The default helped cement Hitler’s power base following years of political instability as the Weimar Republic struggled with its crushing debts.

Rogoff tycks mera ha varit intresserad av att odla sitt kändisskap

än att ta avstånd från hur forskningen använts politiskt

EU:s politiska ledare har tydligt ignorerat lärdomarna från den stora depressionen på 1930-talet.

Peter Wolodarski, signerat DN 28 april 2013

Finanskrisen gjorde Harvardekonomen Kenneth Rogoff till världskändis.

Hösten 2009 deltog jag i en stor journalistkonferens i Köpenhamn och såg uppståndelsen på nära håll.

Redaktörer från hela världen ställde sig i kö för att få Rogoff att signera ett exemplar av boken ”This time is different”

Budskapet kan sammanfattas så här: finanskriser är ett återkommande fenomen i mänsklighetens historia.

Varje gång de slår till tror många att något nytt och oväntat inträffat. Men tittar man bakåt framträder likheterna.

Bubblor blåses upp och spricker, vilket slår hårt mot ekonomin, jobben och statens finanser, ofta under segdragna perioder.

Denna del av Rogoffs och Reinarts arbete har aldrig varit omstridd.

Problemet uppstod när ekonomerna också gjorde gällande att BNP-tillväxten börjar ta allvarlig skada

när statsskulden överstiger 90 procent av bruttonationalprodukten.

Om staten bara återställer balansen i sin budget kommer ekonomin att återhämta sig, har budskapet lytt.

I dag är det deprimerande tydligt hur fel detta tänkande slagit. I stora delar av Europa, inklusive Storbritannien, har åtstramningarna bidragit till den sämsta utvecklingen sedan andra världskriget.

Mycket av det som händer för direkt tankarna till 1930-talet, konstaterar ekonomerna Barry Eichengreen och Brad DeLong i en aktuell essä.

Den gången begicks liknande allvarliga felgrepp i den ekonomiska politiken, vilket banade väg för nazisternas demokratiska maktövertagande i Tyskland.

Då som nu försöker land efter land att spara sig ur problemen, vilket resulterar i en kollektiv kollaps av efterfrågan.

I torsdagens New York Times försöker Rogoff och Reinhart ärerädda sig själva.

De medger misstaget och distanserar sig från hur deras forskning utnyttjats politiskt.

Vi har aldrig förespråkat omedelbara åtstramningar, hävdar de två, men pekar ändå på ett visst samband mellan höga skulder och låg tillväxt.

Så har det inte låtit när Rogoff åkt på världsturné de senaste åren.

Han tycks mera ha varit intresserad av att odla sitt kändisskap än att ta avstånd från hur forskningen använts politiskt, främst av konservativa partier.

Jag kan inte minnas några ljudliga protester när stora delar av Europa försökt kapa sina budgetunderskott på en och samma gång, mitt i depressionen.

EU:s politiska ledare har tydligt ignorerat lärdomarna från den stora depressionen på 1930-talet.

The destruction of the Reichsmark’s value is an important historical lesson.

But missing from that narrative is the painful deflation that followed hyperinflation.

In 1923, at the height of the hyperinflation, 751,000 Germans were without work.

By 1932, as deflation began to bite, unemployment hit 5.6m.

Financial Times 18 January 2015

“There is a strand of historical thinking that the hyperinflation of the 1920s prepared the German people for the rise of Hitler, when in fact the Weimar Republic survived that but not the deflation of the early 1930s,” says Adam Tooze, an economic historian at Yale University.

While Milton Friedman and Anna Schwartz’s seminal text, A Monetary History of the United States, has helped ensure the US policy mistakes that led to deflation are remembered, there is no equivalent in Germany.

That Time - Trettiotalet - was different, i Tyskland

BBC har en artikel som väcker många tankar, vilket förmodligen var avsikten.

I USA och Storbritannien har man sedan 1930-talet en tradition av debatt mellan Kenynesianer och Hooverister.

Men som BBC skriver "In Germany, that argument did not happen. The politics of the 1930s in Germany were different".

Rolf Englund 27 april 2013

In the US and Britain, economists argue over whether government spending is the best way of prompting depressed economies into life.

It is an echo of the argument in the 1930s between "orthodox economics" and the new economics of John Maynard Keynes who argued that governments needed to spend

when interest rates were at rock bottom and there was substantial slack in the economy.

In Germany, that argument did not happen.

The politics of the 1930s in Germany were different, so today there is no Keynesian tradition.

Peter Wolodarski ställde frånga om vi har glömt lärdomarna från början av 1930-talet,

då president Hoover i USA och kansler Brüning i Weimar-Tyskland stod för ett förödande åtstramningstänkande?

Bra Böckers Världshistoria, Band 13, sid 156-157:

När dåvarande tyska regeringschefen Brünings sparsamhetsiver till slut också riktades mot statsbidragen till godsägarna öster om Elbe,

tröt /president/ Hindenburgs tålamod, och den 30 maj 1932 tillträdde en ny regering under ledning av den ytterst konservative tidigare centrumpolitikern Franz von Papen.

Hans regering hade praktiskt taget inget parlamentariskt stöd och förbluffade samtiden genom att majoriteten av ministrarna var adliga.

Socialdemokraterna fällde regeringen. Därefter utlystes nyval.

Resten är historia,som man brukar säga.

Europe is in more danger than at any time since the 1930s.

I believe that the dominant form of political organisation over the next decade will be nationalism.

We are one charismatic leader away from a complete re-ordering of the continent.

Thomas Pascoe, Telegeraph July 13th, 2012

The problem with reparations, halted under the Nazi Party in 1933, was not that the Germans were unable to pay a debt which amounted to 83pct of GDP in 1923: on the contrary, they were (I recommend AJP Taylor’s Origins of the Second World War on this point).

Instead, it was that neither Germany nor pre-Anschluss Austria recognised the "war guilt" clause in the Treaty of Versailles which justified such payments.

Not only did the debtors believe the debts unjust, so did the creditors. Sophisticated opinion in Britain, shared by Cabinet ministers and Keynes, held that the peace terms were unduly harsh on the Germans and would cause unnecessary deprivation. This combination of stubbornness and sympathy ensured that when debts eventually went unpaid, no nation intervened to support the existing financial system.

Betraktar man de senaste årens utveckling i Europa inser man att 30-talskollapsen inte alls är obegriplig eller omöjlig att upprepa.

Den dystra sanningen är ju att eurokrisen bär på många av de frön som en gång framkallade den stora depressionen.

Peter Wolodarski, Dagens Nyheter 10 juni 2012

Highly recommended

The Nazis only won 32 Reichstag seats in the election of May 1924, and just 12 in 1928.

Germany's hyperinflation-phobia

The Nazi party did not become a popular political force until long after the hyperinflation period ended.

The Economist, November 15th 2013

As Paul Krugman has pointed out, “the 1923 hyperinflation didn’t bring Hitler to power; it was the Brüning deflation” of the early-1930s.

A study of hyperinflation published earlier this year by the British historian Frederick Taylor has confirmed that the Nazis benefitted much more from deflation than they did from rising prices.

"Everybody knows you can draw a straight line from its hyperinflation to Hitler, but, in this case, what everybody knows is wrong.

The Nazis didn't take power when prices were doubling every 4 days in 1923-- they tried, and failed -- but rather when prices were falling in 1933."

Lenin's Brilliant Plot to Destroy Capitalism And its essential lessons about money and the economy today

MATTHEW O'BRIEN, The Atlantic, September 26, 2013

Thank You The Market Monetarist Lars Christensen for the link

”Vi lär oss igen den hårda vägen att denna typ av åtstramningar, som tillämpas mitt under brinnande finanskris, bara leder till depression”, konstaterar den tidigare tyske utrikesministern Joschka Fischer i en aktuell kolumn (Project syndicate 25/5)

Han frågar: Har vi glömt lärdomarna från början av 1930-talet, då president Hoover i USA och kansler Brüning i Weimar-Tyskland stod för ett förödande åtstramningstänkande?

Peter Wolodarski, DN 27 maj 2012

Brüning

Europe's political centre is starting to crumble, replicating the pattern of the early 1930s

as the crisis ground into its third year under a similar mix of fiscal and monetary contraction.

Elected governments have already been swept away - or replaced by EU technocrats without a vote, indeed to prevent a vote

- in every eurozone state where unemployment has reached double-digits: Spain (23.6pc), Greece (21pc), Portugal (15pc), Ireland (14.7pc) and Slovakia (14pc).

Ambrose Evans-Pritchard, 24 April 2012

Chancellor Heinrich Bruening’s austerity administration,

politically stalemated by the parliament, had begun governing by presidential fiat.

In a December 1931 decree, Bruening assumed "control of the whole economic machinery of the country" and

"reprieved Germany from imminent collapse," the Economist wrote

Bloomerg 28 februari 2012

German banks, unable to cope with reparations demands and massive conversions of Reichsmarks to gold, collapsed in late 1931, threatening both the financial system and the state. The Berlin stock market had faltered in1928. It soon became clear that banks hadn't revalued their book assets downward; selling them now meant serious losses. In this context, gold withdrawals triggered a panic.

Grekland, Carl Rudbeck, Melodifestivalen, Brüning, Ann-Charlotte Marteus och Don't mention the war

Rolf Englund blog 19 februari 2012

Heinrich Brüning

It is sometimes said that German attitudes to the economy and the current crisis are instructed by experience of Weimar inflation

Yet it wasn't hyperinflation that brought Hitler to power, but rather the depression of the early 1930s,

which in Germany's case was greatly exaggerated by the pro-cyclical austerity the government of the time insisted on applying to the problem.

Jeremy Warner, February 17th, 2012

While on the subject of historical parallels, there's another which has not yet been given sufficient an airing.

This was the vexing question of German war reparations after the slaughter of the First World War,

brilliantly identified by John Maynard Keynes at the time in his polemic, "Economic Consequences of the Peace",

as fundamentally unfair on the Germans. Keynes branded the Treaty of Versailles a "Carthaginian Peace".

"the 1930s are not so far away"

It is considered bad manners to accuse the inventors of the fiscal pact for the eurozone of not having learnt the lesson of German reparations after the first world war.

But the pact enshrines a similar intellectual error, and this needs saying.

Martin Taylor, Financial Times 10 February 2012

That it may be necessary to secure German support is beside the point: reparations were essential (with rather more justification) for French support at Versailles in 1919.

Grekland Albrecht Ritsch

Uppror, kaos och extremism ligger i luften.

En skrämmande parallell till Weimarrepublikens Tyskland när brutala åtstramningar

under Reichskanzler Heinrich Brüning banade väg för nazisterna i början av 1930-talet?

Tomas Lundin, SvD Näringsliv 8 februari 2012

Det hävdar historikern Albrecht Ritsch vid London School of Economics som säger att Lucas Papademos, Greklands premiärminister, på många sätt står inför samma situation. Då som nu var det gigantiska utlandsskulder som skulle betalas tillbaka, då som nu krävdes enorma uppoffringar av befolkningen.

The fixed-exchange mechanism had gone horribly wrong

The tragedy of the interwar years in Germany was that the Social Democrats - then the world’s foremost socialist party - became fatally tainted by acquiescing in /accepting/ Bruning’s deflation torture from 1930 to 1932.

They did so, of course, because they dared not confront the orthodoxies of the Gold Standard.

The result in Germany was the Reichstag election of July 1932 when the Communists and Nazis won over the half the seats.

Ambrose Evans-Pritchard 23 May 2010

By then the fixed-exchange mechanism had gone horribly wrong - in much the same way that EMU has gone horribly wrong - because the surplus countries were not recycling demand to maintain equilibrium. It had become a job-destruction machine.

Stabiliserinspolitik - Rebalancing - Finanskrisen - EMU - Tyskland och EMU

Hitler och skuldkrisen

Det finns en sak som mer än något annat skrämmer slag på tyskar och det är inflation.

Martin Ahlquist, Fokus, 11 november 2011

Det är visserligen 90 år sedan den tyska regeringen gjorde medborgarnas besparingar värdelösa genom att ohämmat trycka sedlar, men tyskarna har inte glömt vad det ledde fram till. Förtroendet för staten var lika med noll och grogrunden var lagd för Adolf Hitlers entré i politiken.

Rädslan för inflation är också huvudskälet till varför Tyskland för allt i världen inte vill ge Europeiska centralbanken alla de befogenheter som krävs för att bekämpa krisen

Det var inte inflationen som förde Hitler till makten,

som Fokus och många andra tror, det var arbetslösheten

Rolf Englund blog 13 november 2011

Det var inte inflationen - det var Depressionen

Germany "the new democracy survived serious threats to its existence in the early postwar years and

found a semblance of stability from 1924 to 1928,

only to be submerged by the collapse of the economy after the Wall Street crash of 1929."

Ian Kershaw, New York Times, February 3, 2008

Ian Kershaw, a professor of modern history at Sheffield University,

is the author of the forthcoming “Hitler, the Germans and the Final Solution.”

The Nazis’ spectacular surge in popular support

(2.6 percent of the vote in the 1928 legislative elections,

18.3 percent in 1930, 37.4 percent in July 1932) reflected the anger, frustration and resentment — but also hope — that Hitler was able to tap among millions of Germans.

Kommentar RE: Det intressanta är här bl a erinradet om att det var en felaktig penningpolitik som ledde till Kraschen 1929 och Depressionen, och därmed Hitler och det Andra Världskriget. Det finns de, se t ex Robert J. Samuelson i Newsweek, som med rätta anser jag, hävdar att den alltför låga räntan i USA var ett resultat av att USA vill stödja det engelska pundet som den engelska finansministern (han hette lustigt nog Winston Churchill) mot Keynes enträgna protester, 1925 hade bundit mot guldet och därmed mot dollarn vid den kurs som rådde före det Första Världskriget.

Se även Keynes ord om sparande och investeringar

Utan bindningen av pundkursen kanske Hitler i stället hade fortsatt som konstnär. En del säger att han var dålig konstnär, men nog var hans tavlor snyggare än den uppstoppade get som dumma borgare står och begrundar på det Moderna Museum som en regering, jag vill inte säga vilken, (Nu 2008 kan det sägas: Det var Bildt-regeringen) har låtit bygga för skattebetalarnas pengar.

Bra Böckers Världshistoria, Band 13, sid 156-157 anför härom:

Inrikespolitiskt lyckades man /i Tyskland/ stabilisera ekonomin

genom att införa ett nytt penningsystem 1923-24.

Inflationssedlarna växlades in till en kurs av en ny mark mot en

biljon gamla. Inflationsprocessen hade verkat som en storstilad

skuldsanering och därmed hade staten på nytt blivit

solvent. Slutet av tjugotalet präglades i Tyskland av ekonomisk

framgång och med den följde också en viss politisk

stabilisering... 1928 bildades en ny majoritetsregering med

socialdemokraten Herman Müller som kansler och den konservative

Gustav Stresemann som utrikesminister... I valet 1928 placerade

sig /Hitlers parti/ NSDAP - Nationalsocialistiska Tyska

Arbetareartiet / i raden av de många småpartierna och

fick 2,6 procent av rösterna...

Världskrisen ledde till

att regeringen sprack i mars 1930. Den avlöstes av en borgerlig

minoritetsregering under ledning av det katolska centrumpartiets

Heinrich Brüning.... Brüning, som var ekonom av

facket, mötte som så många andra länders

statsmän krisen med en deflationspolitik, och han gjorde det mer

konsekvent och energiskt än de flesta. Enligt hans mening gällde

det att anpassa hela ekonomin till de sjunkande priserna. Lönerna

och helst också skatterna måste reduceras, och

framförallt måste den offentliga budgeten balanseras för

att man skullel undgå en inflation. Resultatet blev en kraftig

nedskärning av köpkraften på hemmamarknaden, något

som gjorde det onda värre. Många företag gick i

konkurs. Den tunga industrin och byggnadsindustrin lamslogs nästan

helt, och 1932 registrerades nästan 6 miljoner arbetslösa.

Till dessa bör man troligen lägga ännu en miljon

långtidslediga som helt hade glidit ur det sociala systemet.

Med sjunkande privata inkomster följde minskade offentliga

skatteinkomster, och 1932 måste kommuner, städer och till

och med en delstat gå i konkurs och ställa sig under

riksadministration...

Då Brünings sparsamhetsiver till

slut också riktades mot statsbidragen till godsägarna

öster om Elbe, tröt /president/ Hindenburgs tålamod,

och den 30 maj 1932 tillträdde en ny regering under ledning

ytterst konservative tidigare centrumpolitikern Franz von Papen. Hans

regering hade praktiskt taget inget parlamentariskt stöd och

förbluffade samtiden genom att majoriteten av ministrarna var

adliga.

Socialdemokraterna fällde regeringen. Därefter utlystes nyval.

Det kan vara av intresse att ta del av motsvarande beskrivning i Encyclopedia Britannica Online:

Upon the fall of the coalition government of the Social Democrat Hermann Müller, Brüning was called on to form a new, more conservative ministry on March 28, 1930, without a Reichstag majority.

His policies, formed in response to the onset of the Great Depression, involved increased taxation, reduced government expenditure, high tariffs on foreign agricultural products, cutbacks in salaries and unemployment insurance benefits, and continued payment of the reparations imposed on Germany by the Treaty of Versailles (1919).

Brüning's austerity measures prevented any renewal of inflation, but they also paralyzed the German economy and resulted in skyrocketing unemployment and a drastic fall in German workers' standard of living.

On July 16, 1930, after the Reichstag rejected a major part of his plans, Brüning began governing by presidential emergency decree, using Article 48 of the Weimar Constitution as a basis for this step. On July 18 he dissolved the Reichstag, which returned after new elections in September 1930 with Communist and, more important, Nazi representation greatly increased. To accommodate this shift to the right, the Chancellor enacted a more nationalistic foreign policy. In October 1931, Brüning took over the foreign ministry while retaining the chancellorship. He helped President Paul von Hindenburg win reelection in the spring of 1932, but on May 30 of that year Brüning resigned, a victim of intrigues by General Kurt von Schleicher and others around Hindenburg.

The immediate cause of his dismissal was his project to partition several bankrupt East Elbian estates. Hindenburg, himself an eastern landowner, considered this plan Bolshevism, and his withdrawal of confidence left Brüning with no choice but to resign.

Brüning left Germany in 1934 and ultimately ended up in the United States, where he taught political science at Harvard University from 1937 to 1952.

We should not try to avoid 1929. We have already failed.

The best we can do now is to avoid 1930, 1931 and 1932

What about the €200bn European Union stimulus package that was agreed in a watered-down form by EU leaders on Friday?

Unfortunately, it is a public relations exercise first and foremost, designed to dupe people into believing that the EU is finally doing something.

Wolfgang Münchau, Financial Times, December 14 2008

Mars 1918

Överbefälhavaren Ferdinand Foch, Frankrikes konseljpresident Georges Clemenceau och general Philippe Pétain stod lutade över frontkartor i Fochs högkvarter mellan Beauvais och Compiègne.

Herrarna var bekymrade, mycket bekymrade.

Gates den 10 juni: USA kan inte fortsätta med ”att lägga allt knappare medel på länder som uppenbarligen är ovilliga att själva satsa resurser … på sitt eget försvar”

Per T Ohlsson, Sydsvenskan 26 juni 2011 med bra länkar

Germany’s incoming “grand coalition” of Christian Democrats and Social Democrats is about to commit the biggest economic policy error since unification – the attempt to pursue budget consolidation at the expense of all other economic policy goals. In doing so, it risks turning a five-year-long stagnation into a full-scale depression.

It would be more accurate, perhaps, to compare her /Ms Merkel/ to Heinrich Brüning, a Christian conservative who was German chancellor from 1930 to 1932.

Wolfgang Munchau, Financial Times, 7/11 2005

Wolfgang Munchau is an associate editor of the Financial Times

THE WORLD HITLER NEVER MADE:

Alternate History and the Memory of Nazism,

by Gavriel D. Rosenfeld, Cambridge University Press £19.99, 518 pages

reviewd by Vernon Bogdanor, Financial Times; May 28, 2005

Visions of Victory: The Hopes of Eight World War II Leaders, by Gerhard L. Weinberg, Cambridge University Press £16.99, 284 pages

We are obsessed because we do not understand. How could such a man achieve and wield power in a sophisticated modern society and with popular support?

Even today Hitler remains a more frightening phenomenon than Stalin. For while Soviet communism imposed itself upon a largely unwilling people, there can be little doubt that Hitler would have won a free election in Germany at any time between 1933 and 1942.

Nazism is also an obsession of American historians. These two books are attempts to exorcise it. Gavriel Rosenfeld has had the interesting idea of analysing the numerous alternative histories of Hitler. He explores four counterfactual themes - that the Nazis won the second world war; that Hitler escaped death in 1945 and survived into the postwar era; that he died before 1933; and that the Holocaust was completed, avenged or undone altogether.

Gerhard Weinberg is probably the world's leading expert on Hitler's foreign policy and his book on the second world war, A World At Arms, published in 1994, is by far the best single-volume history of that global conflict. In Visions of Victory, he explores how eight leaders - Hitler, Mussolini, Tojo, Chiang Kai-shek, Stalin, Churchill, de Gaulle and Roosevelt - imagined the world that would succeed the war, a world that is, after all, still very much the one in which we live.

That this nightmare vision did not come to pass is largely due to Winston Churchill. Admittedly, Britain could not, on its own, defeat Hitler, but in 1940, when Stalin was his ally, Britain could ensure that he did not win. Yet the postwar world was not to be Churchill's world, since he did not recognise the force of the idea of self-determination of colonial peoples. Churchill, Roosevelt declared, "thinks only of the colour of their skin; it is when he talks of India and China that you remember he is a Victorian".

It was because Roosevelt understood that the colonial peoples would achieve independence that his postwar vision "came to be realised to a greater extent than that of any of the other World War II leaders".

Few Germans regret that they do not rule Ukraine, few Italians regret the loss of their African empire and few Japanese wish that they still controlled Borneo. And, it may be added, there are not many in Britain who would like to see Britain ruling India.

Visions of Victory is a beautifully written and wide-ranging synthesis of a large and burgeoning literature. It is based on deep knowledge and profound judgment. It is a masterpiece of historical writing that should be read by anyone interested in the origins of the world in which we live.

Farewell to the Mark

By Amity Shlaes

member of The Wall Street Journal's editorial board.

Tyskarna lever med erfarenheterna av det kaos som inflationen skapade i början av 30-talet.

När Churchill som finansminister annonserade återgången till guldmyntfot till förkrigsparitet i april 1925

ansåg Keynes att denna innebar en tioprocentig övervärdering av pundet och skrev en omtalad artikel "The Econocmic Consequences of Mr Churchill", där han anklagade finansministeriets experter för felaktiga kalkyler och för att de underskattat svårigheterna att få till stånd lönesänkningar för att återställa en rimlig pundkurs och undvika arbetslöshet. .. Ett urval av de bästa artiklarna (under mellankrigstiden), som visar Keynes litterära storhet, gavs ut med titeln "Essays in Persuasion" (1931).

Mer här