News Home

Home - Index - Krisen 1992 - EMU - Economics - Cataclysm - Wall Street Bubbles - US Dollar - Houseprices

2007 - This time is different?

On Monday 13th May, I participated in a debate on austerity

organised by the New York Review of Books, held in the Sheldonian Theatre, Oxford.

The motion was: “Austerity in the Eurozone and the UK: Kill or Cure?”.

Those arguing in defence of austerity were Meghnad (Lord) Desai and Sir John Redwood MP.

On my side was Lord (Robert) Skidelsky.

Here is the speech I presented: Austerity has failed.

It has failed in the UK and it has failed in the eurozone.

Its failure was predictable and, by some at least, predicted.

Martin Wolf, May 23, 2013

As a result of heroic interventions by the monetary and fiscal authorities,

many crisis-hit countries enjoyed decent recoveries from the “great recession” of 2008-09.

This then stopped.

The evidence is clear. Fiscal contraction has, indeed, been contractionary.

When many countries contract simultaneously, the impact is far worse, of course,

since one country’s spending on imports is another country’s export demand.

This is why the concerted decision to retrench, strongly supported by our own government, was a huge mistake

Kenneth Rogoff - One of Us?:

“In a debt restructuring, the northern eurozone countries (including France) will see hundreds of billions of euros go up in smoke.

Northern taxpayers will be forced to inject massive amounts of capital into banks, even if the authorities impose significant losses on banks' large and wholesale creditors, as well they should.

These hundreds of billions of euros are already lost, and the game of pretending otherwise cannot continue indefinitely.”

Kenneth Rogoff, Project Syndicate 23 May 2013

How the Case for Austerity Has Crumbled

Paul Krugman, New York Times Review of Books, June 6, 2013

The Alchemists: Three Central Bankers and a World on Fire by Neil Irwin

Austerity: The History of a Dangerous Idea by Mark Blyth

The Great Deformation: The Corruption of Capitalism in America by David A. Stockman

I have enormous respect for Martin Wolf, as he knows, and never miss a single one of his brilliant and indispensable columns.

Indeed, I appreciate his responding, as did Paul Krugman and Joe Wiesenthal, to my recent FT article on the origins of recent eurozone austerity programs.

Mr Wolf’s implicit point that this ECB de facto guarantee of eurozone sovereign debt has reduced the need for austerity is largely correct.

While austerity was not optional for most of the 2010-13 sovereign debt and banking crisis, it is mostly optional now.

Roger Altman, FT 13 May 2013

Roger Altman of Evercore partners is a friend of mine, a distinguished public servant and a respected financial expert.

But his column “Blame bond markets, not politicians, for austerity” is, in my view, gravely mistaken.

Martin Wolf, Financial Times, 10 May 2013

Highly Recommended

I have written on the relevant points several times, most recently in a contribution to an IMF conference.

That presentation focuses on the contrasting experiences of the UK and Spain.

In it, I follow a brilliant 2011 article, “Managing a Fragile Eurozone”by Paul de Grauwe,

a Belgian economist now at the London School of Economics (see here and here).

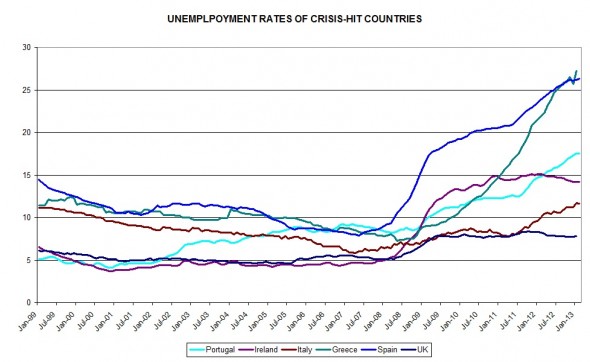

What explains this extraordinary divergence between the long-term interest rates of /Spain and the UK/ countries with very similar debt dynamics?

UK is a sovereign country, with its own finance ministry, central bank and floating currency, while Spain has a subordinate government inside a currency union that has no shared treasury and a super-national central bank

A central bank guarantees liquidity in the market for sovereign debt.That hugely reduces the risk of a sudden default. That, in turn, gives confidence to lenders.

The principal reason why interest rates in Spain are so much higher than those of the UK is that no such lender of last resort existed for the former. Spanish debt was subject to liquidity risk

Altman: ... markets triggered the Eurozone crisis, not politicians. The fiscal and banking restructuring that followed was the price of rebuilding market confidence.

Wolf again: The decline in yields on Spanish debt, shown so clearly in the chart, dates almost precisely to 26th July 2012, the date on which Mario Draghi, president of the ECB, told an audience in London that “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.”

This statement, in turn, led to the announcement by the ECB on August 2nd 2012 of “outright monetary transactions” which would be aimed “at safeguarding an appropriate monetary policy transmission and the singleness of the monetary policy”.

Rightly or wrongly, markets concluded that the risk of an outright default on Spanish bonds had largely disappeared.

Paul Krugman: Nobody has taught me as much about the euro crisis as Paul De Grauwe, Click

Martin Wolf och Rolf Englund om att den som har en sedelpress går inte i konkurs.

Ganska självklart, men vänta till Wolf har förklarat det vetenskapligt, Click

If you have a printing press you don´t go bankrupt

When a country enters a monetary union, like EMU, all debts become foreign debt

in the meaning that the central bank in the country cannot print money.

Rolf Englund 7 Nov 2011

There is a view that implementing the public sector austerity drive

will increase private spending by more than the public sector cutbacks,

thereby itself boosting the economy.

Some advocates suggest that this happens automatically as lower public borrowing reduces interest rates.

But this is plain nonsense.

Roger Bootle, DT 5 May 2013

Short-term interest rates are set by the authorities at whatever level they choose.

Long term rates are determined by the market's willingness to hold the stock of debt.

Yet this is far from being a rigid or mechanistic thing.

Over recent years, the lowest bond yields in the world have been registered in the G7 country with the highest debt, namely Japan.

To be clear, no one should be arguing to stabilise debt, much less bring it down,

until growth is more solidly entrenched – if there remains a choice, that is.

Kenneth Rogoff and Carmen Reinhart, Financial Times May 1, 2013

No one fully understands why rates have fallen so far so fast,

and therefore no one can be sure for how long their current low level will be sustained.

Economists simply have little idea how long it will be until rates begin to rise.

Kenneth Rogoff and Carmen Reinhart, Financial Times May 1, 2013

For Europe any reasonable endgame will require a large transfer from Germany to the periphery.

The sooner this implicit transfer becomes explicit,

the sooner Europe will be able to find its way towards a stable growth path.

Kenneth Rogoff and Carmen Reinhart, Financial Times May 1, 2013

Rogoff tycks mera ha varit intresserad av att odla sitt kändisskap

än att ta avstånd från hur forskningen använts politiskt

EU:s politiska ledare har tydligt ignorerat lärdomarna från den stora depressionen på 1930-talet.

Peter Wolodarski, signerat DN 28 april 2013

That Time - Trettiotalet - was different, i Tyskland

BBC har en artikel som väcker många tankar, vilket förmodligen var avsikten.

I USA och Storbritannien har man sedan 1930-talet en tradition av debatt mellan Kenynesianer och Hooverister.

Men som BBC skriver "In Germany, that argument did not happen. The politics of the 1930s in Germany were different".

Rolf Englund 27 april 2013

Austerity is hurting – but is it working?

Instant debt Armageddon is unlikely for big countries with their own currency

Financial Times, April 26, 2013

Reinhart, Rogoff... and Thomas Herndon

This week, economists have been astonished to find that a famous academic contains major errors.

Another surprise is that the mistakes, by two eminent Harvard professors, were spotted by a student doing his homework.

His professors at the University of Massachusetts Amherst had set his graduate class an assignment

- pick an economics paper and see if you can replicate the results. It's a good exercise for aspiring researchers.

No matter how he tried, he just couldn't replicate Reinhart and Rogoff's results.

BBC 19 April 2013

"My heart sank," he says. "I thought I had likely made a gross error. Because I'm a student the odds were I'd made the mistake, not the well-known Harvard professors."

His professors were also sure he must be doing something wrong.

"I remember I had a meeting with my professor, Michael Ash, where he basically said, 'Come on, Tom, this isn't too hard - you just gotta go sort this out.'"

So Herndon checked his work, and checked again.

By the end of the semester, when he still hadn't cracked the puzzle, his supervisors realised something was up.

Charge of the Right Brigade

The really smart Wall Street money - Jan Hatzius and the rest of the economics group at Goldman

have an underlying macroeconomic framework pretty much indistinguishable from mine.

Paul Krugman - New York Times Blog MARCH 16, 2014

The austerian position has imploded

Yet two big questions remain

How did austerity doctrine become so influential in the first place?

Will policy change at all now that crucial austerian claims have become fodder for late-night comics?

Paul Krugman, New York Times 25 April 2013

The dominance of austerians in influential circles should disturb anyone who likes to believe that policy is based on, or even strongly influenced by, actual evidence.

Part of the answer surely lies in the widespread desire to see economics as a morality play, to make it a tale of excess and its consequences. We lived beyond our means, the story goes, and now we’re paying the inevitable price.

The average American is somewhat worried about budget deficits,

which is no surprise given the constant barrage of deficit scare stories in the news media,

but the wealthy, by a large majority, regard deficits as the most important problem we face.

And how should the budget deficit be brought down?

The wealthy favor cutting federal spending on health care and Social Security — that is, “entitlements” —

while the public at large actually wants to see spending on those programs rise.

You get the idea: The austerity agenda looks a lot like a simple expression of upper-class preferences,

wrapped in a facade of academic rigor.

What the top 1 percent wants becomes what economic science says we must do.

Correspondents in Germany, France, Italy and Portugal, look at

whether or not governments and voters are yet ready to decisively move away from austerity

BBC 27 April 2013

Market veteran Art Cashin, the director of floor operations at UBS,

suggested the bounce be called the "Reinhart/Rogoff Rebuttal Rally."

CNBC 25 April 2013

"As the rebuttal made headlines, markets rallied — especially in Europe — as cries that austerity had seen its day came from leader after leader," Cashin said.

"Was it really the rebuttal that moved markets? We may never be able to prove it conclusively but the timing seems like a perfect fit."

It's true that the market is no shrinking violet when it comes to government debt.

In fact, it has thrived as the U.S. and other governments have amped up debt loads.

The Federal Reserve has been complicit in the run-up by buying more than $3 trillion of U.S. notes alone.

Worries of asset bubbles and inflation wait for another day.

"We are all Keynesians now"

Why do we pursue austerity when it seems not to work?

Rogoff and Reinhart?

John Mauldin 22 April 2013

Highly Recommended

In 1816, the net public debt of the UK reached 240 per cent of gross domestic product.

This was the fiscal legacy of 125 years of war against France.

What economic disaster followed this crushing burden of debt?

The industrial revolution.

Martin Wolf 23 April 2013

Professors Reinhart and Rogoff, their work and that of others supports the proposition that slower growth is associated with higher debt.

But an association is definitely not a cause.

Slow growth could cause high debt, a hypothesis supported by Arindrajit Dube, also at Amherst.

Consider Japan: is its high debt a cause of its slow growth or a consequence? My answer would be: the latter.

Usually, one can ignore the macroeconomic consequences of fiscal austerity: either private spending will be robust or monetary policy will be effective. But, after a financial crisis, a huge excess of desired private savings is likely to emerge, even when interest rates are very close to zero.

In that situation, immediate fiscal austerity will be counterproductive. It will drive the economy into a deep recession, while achieving only a limited reduction in deficits and debt.

Baltikum ger hopp till Europa

I går höll tankesmedjan Fores ett seminarium som

ställde frågan om Baltikum har lyckats spara sig ur krisen.

Det korta svaret är ja.

SvD ledarsida, Ivar Arpi 23 april 2013

Let me highlight a passage from the "Understanding Our Adversaries" evolution-of-economists'-views talk that I started giving three months ago, a passage based on work by Owen Zidar summarized by the graph above:

REINHART-ROGOFF WEBLOGGING:

NO, THEIR ARGUMENT FOR AUSTERITY NOW OUT OF FEAR OF DEBT DIDN'T SEEM TO ME TO MAKE THAT MUCH SENSE

The argument [for fiscal contraction and against fiscal expansion in the short run] is now:

never mind why, the costs of debt accumulation are very high.

This is the argument made by Reinhart, Reinhart, and Rogoff:

when your debt to annual GDP ratio rises above 90%, your growth tends to be slow.

Brad DeLong, April 19th, 2013

This is the most live argument today. So let me nibble away at it.

And let me start by presenting the RRR case in the form of Owen Zidar's graph.

First: note well: no cliff at 90%.

Second, RRR present a correlation - not a causal mechanism, and not a properly-instrumented regression.

There argument is a claim that high debt-to-GDP and slow subsequent growth go together,

without answering the question of which way causation runs.

Let us answer that question.

This week three economists at the University of Massachusetts at Amherst revealed problems with

the data behind one of Profs Reinhart and Rogoff’s ensuing articles

One cannot read their analysis and then conclude that the case for austerity – and a tough line on debt – is much weakened.

Anders Aslund, i.e. Åslund, Financial Times, April 19 2013

This has been presented as a blow to the case for austerity, of which Profs Reinhart and Rogoff have been prominent proponents.

Their work has been an important corrective to the view that fiscal stimulus is always right

– a position that is common across the Anglo-American economic commentariat, led by Paul Krugman in the New York Times.

Why Austerity Works and Stimulus Doesn’t

The starkest contrasts are Latvia and Greece, two small countries hit the worst by the crisis.

They have pursued different policies, Latvia strict austerity, and Greece late and limited austerity.

Anders Aslund, Bloomberg 8 January 2013

A dose of reality for the dismal science

Reinhart and Rogoff’s claim of a debt-level tipping point never made any sense

Adam Posen, Financial Times, April 19, 2013

For a few years, advocates of rapid fiscal austerity have argued as though public debt is like a black hole – once it reaches a certain size, it collapses in on itself under its own weight and pulls the economy down with it.

A 2010 academic paper by Carmen Reinhart and Kenneth Rogoff, two eminent economics professors, provided many pundits and politicians with the desired evidence for this instinctive view. They seemingly found that economic growth fell off sharply when national debts reached 90 per cent of gross domestic product.

A new study that has attracted lots of attention, however, shows that no such sharp fall-offs occur.

Put aside the details of Excel coding errors and statistical weights. In fact, forget that specific paper. The claim that there was a clear tipping point for the ratio of government debt to GDP past which an economy’s walls caved in never made any sense.

An American economist on the Bank of England’s monetary policy committee,

Mr. Posen is no academic scribbler or lonely blogger

New York Times 17 Sept 2011

Harvard economists, Carmen Reinhart and Kenneth Rogoff

Did an Excel coding error destroy the economies of the Western world?

First, they omitted some data; second, they used unusual and highly questionable statistical procedures

Paul Krugman, New York Times, April 18, 2013

At the beginning of 2010, two Harvard economists, Carmen Reinhart and Kenneth Rogoff, circulated a paper,

“Growth in a Time of Debt,” that purported to identify a critical “threshold,” a tipping point, for government indebtedness.

Once debt exceeds 90 percent of gross domestic product, they claimed, economic growth drops off sharply.

Ms. Reinhart and Mr. Rogoff had credibility thanks to a widely admired earlier book on the history of financial crises, and their timing was impeccable.

Reinhart-Rogoff quickly achieved almost sacred status among self-proclaimed guardians of fiscal responsibility;

their tipping-point claim was treated not as a disputed hypothesis but as unquestioned fact.

As soon as the paper was released, many economists pointed out that

a negative correlation between debt and economic performance need not mean that high debt causes low growth.

It could just as easily be the other way around, with poor economic performance leading to high debt.

Indeed, that’s obviously the case for Japan, which went deep into debt only after its growth collapsed in the early 1990s.

Finally, Ms. Reinhart and Mr. Rogoff allowed researchers at the University of Massachusetts to look at their original spreadsheet — and the mystery of the irreproducible results was solved.

First, they omitted some data; second, they used unusual and highly questionable statistical procedures; and finally, yes, they made an Excel coding error.

Correct these oddities and errors, and you get what other researchers have found:

some correlation between high debt and slow growth, with no indication of which is causing which,

but no sign at all of that 90 percent “threshold.”

In a new working paper, co-authored with Thomas Herndon, we found that these results were based on a series of data errors and unsupportable statistical techniques.

Robert Pollin and Michael Ash, Financial Times, 17 April 2013

Debunking austerity claims makes no difference to Europe's monks and zealots

Fresh research has refuted the famous Reinhart-Rogoff paper showing a cliff-edge fall in growth to minus 0.1pc once public debt reaches 90pc of GDP.

The greater conceptual error was to conflate correlation and cause

This was the paper seized upon by Tea Party Republicans, scorched-earth Schaublerians and Rehnites in Europe, our own dear Chancellor George Osborne, and

Austro-liquidationists the world over, to back calls for draconian, pro-cyclical, fiscal tightening.

Ambrose, April 18th, 2013

Empirical Economics Isn’t Yet as Smart as Dentistry

Clive Crook Apr 19, 2013

If economists could manage to get themselves thought of as humble,

competent people on a level with dentists, that would be splendid.

John Maynard Keynes

Read more at www.brainyquote.com

The academic evidence on Keynesian growth effects of fiscal deficits is thoroughly inconclusive.

Kenneth Rogoff, July 20 2010

The writer is professor of economics at Harvard University and co-author, with Carmen Reinhart, of This Time is Different: Eight Centuries of Financial Folly

Aggressive fiscal stimulus in the run-up to the financial crisis was reasonable as part of an all-out battle to avoid slipping into a depression.

The risk of a second Great Depression was palpable, the huge cost of insurance arguably worth it.

Today, the panic has abated, and a more sober cost-benefit analysis is required.

Importantly, governments that emphasise long-term fiscal sustainability are likely to have an easier time inducing their central banks to maintain highly supportive monetary conditions.

If a double-dip recession does threaten, then monetary policy, including aggressive measures to combat deflation, remains by far the most reliable first line of defence.

“Everyone wants to think they’re smarter than the poor souls in developing countries, and smarter than their predecessors,” says Carmen M. Reinhart

Ms. Reinhart and her collaborator from Harvard, Kenneth S. Rogoff, have spent years investigating wreckage scattered across documents from nearly a millennium of economic crises and collapses.

New York Times July 2, 2010

THE advertisement warns of speculative financial bubbles. It mocks a group of gullible Frenchmen seduced into a silly, 18th-century investment scheme, noting that the modern shareholder, armed with superior information, can avoid the pitfalls of the past. “How different the position of the investor today!” the ad enthuses.

It ran in The Saturday Evening Post on Sept. 14, 1929. A month later, the stock market crashed.

The cruel irony of the euro area’s predicament is that, in many ways,

the whole exercise was designed to produce the very credit explosion that bedevils it today

Kenneth Rogoff, FT May 5 2010

Lower interest rates, in turn, helped fuel greater borrowing, especially in the countries of the eurozone periphery. Thus, the spreading debt crisis is as much a product of the “success” of the euro as of its failure. The euro was designed to be a superior debt financing machine and, to a considerable extent, it has delivered. Unfortunately, it should have come with a warning sign: Europe’s leaders were far too quick to admit members who might have been better served with a much longer probation period. The Maastricht treaty and, more importantly its implementation, was simply too forgiving, especially for countries with chequered financial histories.

Economists have only a limited understanding of why sovereign nations ever repay their external debt, given the lack of any supranational legal authority that might force them to do so.

It is going to be extremely difficult for some of the peripheral eurozone economies to escape without large-scale defaults on their massive private external debts, public external debts, or both.

The writer is professor of economics at Harvard and co-author with Carmen Reinhart of ‘This Time is Different’

---

The IMF should impose default on Greece to end the charadeI just had lunch with Carmen Reinhart, author of `This Time is Different: Eight Centuries of Financial Folly” and a world authority on sovereign defaults.

Ambrose Evans-Pritchard Economics April 2nd, 2010

Rogoff varnar för fler bankkonkurser

"USA har inte klarat krisen.

Jag tror att finanskrisen kanske har nått halvvägs."

DI 2008-08-19

"USA har inte klarat krisen. Jag tror att finanskrisen kanske har nått halvvägs. Jag skulle till och med gå ännu längre och säga att det värsta återstår, sade Harvardprofessorn Kenneth Rogoff vid en konferens.

The global financial crisis is set to get worse, with a large US bank likely to collapse in the next few months, a former IMF chief economist has warned.

BBC 19/8 2008

Kenneth Rogoff's comments came as shares in Fannie Mae and Freddie Mac sank on a report that the home lenders would, in effect, be nationalised.

The world cannot grow its way out of this slowdown

The main macroeconomic challenges facing the world today are an excess demand for commodities and an excess supply of financial services

Need to introduce more banking discipline

Kenneth Rogoff, Financial Times July 29 2008

The writer is professor of economics at Harvard University and

former chief economist at the International Monetary Fund

In the light of the experience of the 1970s, it is surprising how many leading policymakers and economic pundits believe that policy should aim to keep pushing demand up.

In the US, the growth imperative has rationalised aggressive tax rebates, steep interest rate cuts and an ever-widening bail-out net for financial institutions.

If all regions try expanding demand, even the short-term benefit will be minimal. Commodity constraints will limit the real output response globally, and most of the excess demand will spill over into higher inflation.

For a myriad reasons, both technical and political, financial market regulation is never going to be stringent enough in booms. That is why it is important to be tougher in busts, so that investors and company executives have cause to pay serious attention to risks.

If poorly run financial institutions are not allowed to close their doors during recessions, when exactly are they going to be allowed to fail?

Of course, today’s mess was many years in the making and there is no easy, painless exit strategy.

But the need to introduce more banking discipline is yet another reason why the policymakers must refrain from excessively expansionary macroeconomic policy at this juncture and accept the slowdown that must inevitably come at the end of such an incredible boom.

This Time is Different: A Panoramic View of Eight Centuries of Financial Crises, NBER Working Paper 13882, March 2008

Same as it ever was

Is the 2007 US Sub-Prime Financial Crisis so Different?

Kenneth Rogoff, a professor at Harvard University, his paper sets out some parallels between America's subprime mess and 18 previous banking crises in the rich world.

The Economist Jan 2008

At the AEA conference, it fell to Alan Taylor of the University of California to make the case that things might not turn out quite as badly

If all of America's subprime borrowers defaulted and

only half of the $1.3 trillion lent to them was recovered,

the losses of $650 billion would amount to around 5% of GDP

Comment by Rolf Englund:

Is not 650 bn dollar rather much, especially comparet with the capital of the banks, not compared with GDP?

See also: A mere 5.4% decline in the value of Citigroup's assets would make Citigroup insolvent.

The U.S. housing stock is worth about $23 trillion, so a 15 percent drop in house prices represents a wealth erasure of $3.45 trillion

John Makin

Is the 2007 US Sub-Prime Financial Crisis so Different?

- Different from the Debt Crisis of the 80's?

Martin Wolf, FT January 8 2008

That there was a link between the savings glut and the financial fragility was evident. The former, I argued, generated the global imbalances and the monetary policy that drove household borrowing to the level required to absorb the capital inflow. Soaring house prices and rising household indebtedness were the vehicles through which policy worked.

As Carmen Reinhart of the University of Maryland and Kenneth Rogoff of Harvard note in a brilliant new paper*, this had similarities to the recycling of petrodollars to developing countries that preceded the debt crisis of the 1980s.

*Is the 2007 US Sub-Prime Financial Crisis so Different? An International Historical Comparison?

http://www.economics.harvard.edu/faculty/rogoff/files/Is_The_US_Subprime_Crisis_So_Different.pdf

This time, surplus savings were, in their words, “recycled to a developing country that exists within the US”: the subprime borrowers. The consequences for banks also look disturbingly similar.

The question that matters is whether the US will experience a lengthy period of weak growth in private demand. The chances that it will are high. This is the conclusion I draw from the paper by Professors Reinhart and Rogoff.