Rolf Englund IntCom internetional

Home - Index - News - EMU - Cataclysm - Financial Crisis - Houseprices - Dollarn - My other Guru Economists

- ContactDet är inte svårt att förstå vad som händer i världsekonomin.

Det är bara att läsa vad Martin Wolf skriver i Financial Times.

Rolf Englund blog 10 oktober 2014

Why so little has changed since the financial crash

Martin Wolf FT 4 september 2018

Big questions to be answered concern timing, consequences and even what is meant by ‘normalisation’

Prophets of doom predict (or hope) that the world will at last suffer for the sins of activist central bankers.

Martin Wolf, FT 21 January 2018, state of the art article with nice charts

Unfinished Business:

The Unexplored Causes of the Financial Crisis and the Lessons Yet to be Learned, by Tamim Bayoumi

Martin Wolf, 1 December 2017

We’re in bubble territory again, but this time might be different

Martin Wolf, FT 10 November 2017

Populism and immigration

The financial crisis and consequent economic shocks not only had huge costs.

They also damaged confidence in — and so the legitimacy of — financial and policymaking elites.

These emperors turned out to be naked.

Martin Wolf FT 27 June 2017

Remarkably, real domestic demand in the eurozone was 1.1 per cent lower

in the second quarter of 2016 than it had been in the first quarter of 2008.

This extreme weakness of demand should not have happened. It represents a huge failure.

Martin Wolf, FT 6 December 2016

Capitalism and democracy

Martin Wolf FT 30 August 2016

Monetary policy is not exhausted, and active use of it is essential.

But undue reliance on monetary policy is problematic.

Martin Wolf, FT 25 May 2016

Negative rates are not the fault of central banks

The world economy is suffering from a glut of savings relative to investment opportunities.

Martin Wolf, FT 12 April 2016

The world economy is in no position to absorb another big deflationary shock.

The possibility of another big deflationary shock from China over the next several years is real.

Martin Wolf, FT 29 March 2016

Will IT disrupt finance?

Martin Wolf FT 8 March 2016

Donald Trump embodies how great republics meet their end

The US is the greatest republic since Rome, the bastion of democracy, the guarantor of the liberal global order.

It would be a global disaster if Mr Trump were to become president.

Even if he fails, he has rendered the unthinkable sayable.

Martin Wolf, FT 1 March 2016

Helicopter drops might not be far away

The world economy is slowing, both structurally and cyclically.

How might policy respond? With desperate improvisations, no doubt.

Martin Wolf, FT 23 Febr 2016

Martin Wolf:

What might central banks do if the next recession hit while interest rates were still far below pre-2008 levels?

FT February 2016

Donald Trump, Marine Le Pen, Nigel Farage

The economic losers are in revolt against the elites

Martin Wolf January 26, 2016

Germany wants IMF-style conditionality imposed on Greece more or less indefinitely.

But both the Greek government and the staff of the IMF dislike this possibility.

The former hates it because it wants a free hand.

The latter hate it because they fear the conditions for successful programmes do not exist.

This being so, they cannot, in good conscience, recommend one to the board.

Martin Wolf, FT 22 December 2015

US and Europe still live with the legacies of the financial crisis of 2007-09 and the subsequent eurozone crisis.

Could better policies have prevented that outcome; and, if so, what might they have been?

Martin Wolf, FT 10 November 2015

Lunch with Ben Bernanke

I turn, finally, to perhaps the biggest question about the crisis. Could they have avoided the failure of Lehman in September 2008?

“No,” he responds firmly. “It was completely unavoidable. Without a buyer, there was no one to guarantee their liabilities. So no one would lend to them. There was a complete run of all the creditors, all of the counterparties, all of the customers.

And if we had lent them the money and somehow conjured up some fake collateral, in violation of the law, we would have ended up owning the firm, and it would have been a non-viable firm.”

Martin Wolf, FT 23 October 2015

Solid growth is harder than blowing bubbles

The world economy has lost its last significant credit-fuelled engine of demand - China.

The result is almost certain to be a further boost to the global “savings glut” or, as Lawrence Summers calls it, “secular stagnation” — the tendency for demand to be weak relative to potential supply.

Martin Wolf, FT October 13, 2015

The case for keeping US interest rates low

After nearly seven years of zero interest rates, the inflation of which critics warned is invisible

Martin Wolf, FT September 8, 2015

Relative to US levels, China’s GDP per head is where South Korea’s was in the mid-1980s.

South Korea’s real GDP per head has since nearly quadrupled in real terms, to reach almost 70 per cent of US levels.

Martin Wolf, Financial Times September 1, 2015

Recent events must be seen in the context of a deeper concern.

If they can, the economy will also sustain growth of 6-7 per cent.

If they cannot, economic and political instability threatens.

Martin Wolf, FT 25 August 2015

Martin Wolf:

There are no /Greek/ government deficits to finance consumption (or almost none).

So money would be used to pay interest and amounts due

Rolf Englund blog 9 July 2015

Output is financially sustainable when spending patterns and the distribution of income are such that the fruit of economic activity can be absorbed without creating dangerous imbalances in the financial system.

It is unsustainable if generating enough demand to absorb the output of the economy requires too much borrowing, real rates of interest rates that are far below zero, or both.

Martin Wolf, FT 14 April 2015

Houseprices - Change will come only once people recognise how unjust this situation has become

Massive transfers of resources across generations —

and, within generations, to people whose parents own properties — which is arguably more important.

Martin Wolf, FT January 8, 2015

Finanskrisen

Martin Wolf på Financial Times är, vågar jag påstå, den världsledande journalisten på området finansiell ekonomi.

När han analyserar den globala finanskris som fortfarande pågår lyssnar alla som vill förstå.

Nils Lundgren, Axess Magasin nr 8, november 2014

In my book, The Shifts and the Shocks, I suggest that a number of shifts in the world economy

created chronically weak demand in the absence of credit booms.

US, the eurozone, Japan and the UK have been suffering from “chronic demand deficiency syndrome”.

More precisely, their private sectors have failed to spend enough to bring output close to its potential

without the inducements of ultra-aggressive monetary policies, large fiscal deficits, or both.

Martin Wolf, FT November 25, 2014

Today’s most important economic illness: chronic demand deficiency syndrome.

David Cameron “red warning lights are once again flashing on the dashboard of the global economy”.

Martin Wolf, Financial Times 18 november 2014

In my book The Shifts and the Shocks, I argue that pre-crisis trends

– huge global current account imbalances, rising inequality and weak propensity to invest –

had already created weak underlying demand in high-income countries.

The de facto response of policy makers was toleration, if not promotion, of credit booms.

When these collapsed, extraordinary policy easing was needed both to replace the lost demand impetus from the credit bubbles and to

offset the drag on demand from debt overhangs, predominantly in private sectors:

too many people had borrowed too much.

Martin Wolf, FT October 9, 2014

Read the Editorial Reviews of the Book at Amazon Kindle

Why Weren’t Alarm Bells Ringing?

The Shifts and the Shocks: What We’ve Learned—and Have Still to Learn—from the Financial Crisis by Martin Wolf

Paul Krugman, New York Review of Books, October 23, 2014 Issue

Posterity will regard the economic performance we are now witnessing as a golden age.

It will also know, although we do not, how long this era lasts.

Martin Wolf, FT, 2/5 2007

I have enormous respect for Martin Wolf, as he knows,

and never miss a single one of his brilliant and indispensable columns.

Roger Altman, FT 13 May 2013

Will the asset quality review and stress tests conducted by the European Central Bank and the European Banking Authority mark a turning point in the eurozone’s crisis?

Leverage is 20 to 1 in Spain and Italy; 25 to 1 in Germany and France; and 30 Lto 1 in the Netherlands.

It is questionable whether this is enough loss-absorbing capital.

Martin Wolf, FT October 28, 2014

Withdrawal of mortgage equity, financed by borrowing, has collapsed.

Martin Wolf, FT September 30, 2014

The financial crises and the years of economic malaise that followed represent profound failures of the economy and of policy.

Above all, they were failures of understanding.

We have learnt much since. But we have not learnt enough to avoid a repeat of this painful experience.

As I argue in a new book, we retain unbalanced and financially fragile economies.

Martin Wolf, Financial Times, September 3, 2014

Summer reading: Economics

Martin Wolf picks his books of the year so far

FT, June 27, 2014

How much of the world’s fossil fuel reserves will eventually be burnt?

Either the world will abandon its pledge to keep emissions below the level thought to produce a temperature rise of 2C

or the fossil fuel companies are holding stranded assets and investing in unusable ones.

Investors are implicitly betting on the former possibility.

Martin Wolf, Financial Times 17 June 2014

Three events that shaped our world

This year is the 100th anniversary of the start of the first world war,

the 70th anniversary of D-Day and

the 25th anniversaries of the collapse of the Soviet empire and the savage crackdown around Tiananmen Square.

Martin Wolf, Financial Times June 10, 2014

Mr Draghi this time seeks to end the threat of deflation. Will he be equally successful?

Experience suggests that only the brave would bet against him.

Yet to succeed twice would be quite a remarkable achievement.

Martin Wolf, Financial Times June 6, 2014

Are financial crises an inevitable feature of capitalism?

Must the government rescue the system when huge crises occur?

In his book Stress Test, Timothy Geithner answers “yes” to both questions.

Yet these answers also harm the legitimacy of a market economy.

Martin Wolf, Financial Times, 27 May 2014

Tim Geithner

Stress Test: Reflections on Financial Crises, lunch with Martin Wolf

"the big persistent misperception is that we acted out of an excessive concern for the banks"

Financial Times 15 May 2014

At present the world’s high propensity to save is not matched by a desire to invest.

High-income economies have had ultra-cheap money for more than five years. Japan has lived with it for almost 20.

The highest interest rate charged by any of the four most important central banks in the high-income economies is 0.5 per cent at the Bank of England.

Martin Wolf, FT May 6, 2014

Why are real interest rates so low? And will they stay this low for long?

If they do – as it seems they might – the implications will be profound:

good for debtors, bad for creditors and above all, worrying for the vigour of global demand.

Martin Wolf, FT April 29, 2014

Only the ignorant live in fear of hyperinflation

Failure to understand the monetary system has made it more difficult for central banks to act

Martin Wolf, FT April 10, 2014

There is no easy path to democracy

The basic needs are true citizens, honest guardians, proper markets and just laws

Martin Wolf, FT 4 March 2014

My starting point is that government accountable to the governed is the only form suitable for grown-ups.

All other forms of government treat people as children.

In the past, when most people were illiterate, such paternalism might have been justified.

That can no longer be true. As the population becomes more informed, governments that treat their peoples in this way will be less acceptable.

I expect (or hope) that, in the long run, this will be true even of China.

Ben Bernanke – a distinguished scholar, he brought to the Fed a brilliant and well-informed mind.

His knowledge of economic history helped him halt a terrifying panic.

But he also made mistakes.

History will probably judge him kindly. But there is much to be learnt from his time at the Fed.

Martin Wolf, FT 21 January 2014

The failures of Europe’s political, economic and intellectual elites created the disaster that befell their peoples between 1914 and 1945. The west is not immune to elite failures.

On the contrary, it is living with them. Here are three visible failures.

Martin Wolf, Financial Times 14 January 2014

Highly recommended

If the /UK/ economy was not massively overheated in 2007 and fiscal policy had not been hugely irresponsible,

what caused the post-crisis losses of output and consequent fiscal deterioration?

The answer to the first question is the global financial crisis.

Martin Wolf, Financial Times 19 December 2013

A concern is that the monetary policy of the ECB is unsuitable for Germany and might even cause asset price bubbles.

This is surely true, just as the monetary policy pursued before 2007 was unsuitable for Ireland and Spain and did indeed drive asset price bubbles.

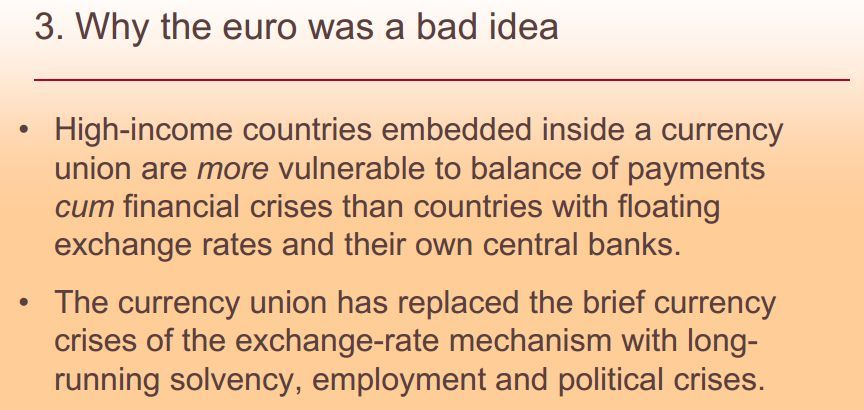

A central bank called upon to deliver a target rate of inflation in a union of diverse economies will destabilise nearly all the members at some time.

But that is what joining a currency union entails for all members, including even the largest.

Martin Wolf, FT, November 12, 2013

The German finance ministry responded that its current account surplus was “no cause for concern, neither for Germany, nor for the eurozone, or the global economy”.

This reaction is as predictable as it is wrong.

The surplus, forecast by the IMF at $215bn this year (virtually the same as China’s) is indeed a big issue, above all for the future of the eurozone.

Martin Wolf, Financial Times, 5 Novermber 2013

The four most important central banks – Fed, ECB, Bank of Japan and the Bank of England – all have short-term interest rates of half a per cent, or less.

These rates have remained extremely low for four years, or more.

What then has all this monetary activism bought? Disappointment.

Martin Wolf, FT October 10, 2013

Inordinate reliance on monetary policy, often highly unconventional monetary policy, whose effects on the economy are at least as uncertain as those of fiscal stimulus.

Future economists may wonder about our extraordinary belief in the efficacy of monetary policy during what is, quite clearly, a private sector savings glut.

Martin Wolf, 8 October 2013

In a democracy, people overturn laws by winning elections, not by threatening the closure of government or even an outright default.

It is impossible to run the government of a serious country under blackmail threats of this kind.

Every time the administration gives in, it stores up more difficulty for itself. It has to stop doing so.

Martin Wolf, FT October 1, 2013

Det allra svåraste - att landa på ett hangarfartyg, link to Youtube

Risks of a hard landing for China

The pilot is allowing the plane to slow down, but if it slows too much,

it will fall below stall speed and drop out of the sky.

Martin Wolf, Financial Times, July 2, 2013

Via Rolf Englund blog dagens länkar 3 juli 2013

What is the “stall speed” of an economy?

The parallels drawn by Mr Schäuble between Germany’s reforms in the 2000s

and the position of today’s vulnerable countries are absurd.

Martin Wolf, Financial Times, September 24, 2013

At the heart of the new global economy are what Peter Nolan, professor of Chinese development at Cambridge university, calls “systems integrator” companies – businesses with dominant brands and superior technologies, which are at the apex of value chains that serve the global middle classes.

Prof Nolan concludes that the number of globally dominant businesses in the manufacture of large commercial aircraft and carbonated drinks was two;

of mobile telecommunications infrastructure and smart phones, just three;

of beer, elevators, heavy-duty trucks and personal computers, four; of digital cameras, six; and of

motor vehicles and pharmaceuticals, 10.

Martin Wolf, Financial Times, July 9, 2013

Yes, yields on US conventional 10-year bonds are up about 40 basis points over the past month.

But they are still just over 2 per cent. This is hardly a bond market Armageddon.

If recovery takes hold, as we hope, yields will rise further.

Nobody can have supposed that nominal and real long-term interest rates would remain at basement levels forever.

Martin Wolf, 4 June 2013

On Monday 13th May, I participated in a debate on austerity

organised by the New York Review of Books, held in the Sheldonian Theatre, Oxford.

The motion was: “Austerity in the Eurozone and the UK: Kill or Cure?”.

Those arguing in defence of austerity were Meghnad (Lord) Desai and Sir John Redwood MP.

On my side was Lord (Robert) Skidelsky.

Here is the speech I presented: Austerity has failed.

It has failed in the UK and it has failed in the eurozone.

Its failure was predictable and, by some at least, predicted.

Martin Wolf, May 23, 2013

The mistaken consensus swiftly emerged, notably in Berlin, that this was a fiscal crisis.

But that was to confuse symptoms with causes, except in the case of Greece.

"this analysis of “imbalances” close to indefensible"

Martin Wolf, Financial Times May 7, 2013

Roger Altman of Evercore partners is a friend of mine, a distinguished public servant and a respected financial expert.

But his column “Blame bond markets, not politicians, for austerity” is, in my view, gravely mistaken.

I follow a brilliant 2011 article, “Managing a Fragile Eurozone”by Paul de Grauwe

(Paul Krugman: Nobody has taught me as much about the euro crisis as Paul De Grauwe)

Martin Wolf, Financial Times, 10 May 2013

“Managing a Fragile Eurozone”by Paul de Grauwe

The decline in yields on Spanish debt, shown so clearly in the chart, dates almost precisely to 26th July 2012, the date on which Mario Draghi, president of the ECB, told an audience in London that “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.”

This statement, in turn, led to the announcement by the ECB on August 2nd 2012 of “outright monetary transactions” which would be aimed “at safeguarding an appropriate monetary policy transmission and the singleness of the monetary policy”.

Rightly or wrongly, markets concluded that the risk of an outright default on Spanish bonds had largely disappeared.

Martin Wolf, Financial Times, 10 May 2013

Why should countries with such similar fiscal positions face such different bond yields?

Relevant is the fact that Spanish bonds may still be thought subject to the catastrophic risk of a eurozone break-up,

despite the European Central Bank’s promise to intervene via its programme of outright monetary transactions.

The ability and desire of the Bank of England to prevent outright default is more credible

than that of an independent, supranational central bank.

Martin Wolf, Financial Times, 25 April 2013

As Belgian economist Paul De Grauwe of the London School of Economics has noted...

Martin Wolfs presentation at IMF

If you have a printing press you don´t go bankrupt

When a country enters a monetary union, like EMU, all debts become foreign debt

in the meaning that the central bank in the country cannot print money.

Rolf Englund 7 Nov 2011

In 1816, the net public debt of the UK reached 240 per cent of gross domestic product.

This was the fiscal legacy of 125 years of war against France.

What economic disaster followed this crushing burden of debt?

The industrial revolution.

Martin Wolf 23 April 2013

It is weird that inflation has remained so stable,

despite huge shortfalls in output, relative to pre-crisis trends, and prolonged high unemployment.

Understanding why this is the case is important because the answer determines the correct policy action.

Martin Wolf, Financail Times 16 April 2013

Britain’s perilous austerity bunker

Cameron’s arguments against fiscal policy flexibility are wrong

Martin Wolf, Financial Times, March 12, 2013

Highly recomended

A case to reset basis of monetary policy

The current regime is meant to stabilise inflation

and help stabilise the economy. It has failed

Martin Wolf, FT February 7, 2013

In the eurozone, the ECB succeeded in removing the tail risk of a eurozone break-up by gaining German support for a promise to buy sovereign bonds.

It was victorious without firing a shot. But that does not tell us what would happen if it had to start firing.

The ECB might still be forced to deliver on its promises to buy. Nobody knows what would happen

Martin Wolf, FT January 29, 2013

Let us look at alternative ways of accelerating deleveraging.

Broadly there are two: capital transactions and default.

The latter, in turn, comes in two varieties: plain vanilla default and inflationary default.

Martin Wolf, Financial Times 30 July 2012

Minsky moment

In 2009, the world was in a state of shock.

Now, despite successful efforts at stabilising economies, people are closer to despair.

Something seems to be wrong with the system. But what, and what needs to be done?

Martin Wolf, FT, January 22, 2012

The big divide is between those – the Austrians

– who hold that the mistakes are made by governments while the solution is to let the distorted financial edifice collapse

and those – the post-Keynesians

– who hold that a modern economy is inherently unstable, while letting it collapse would take us back to the 1930s.

I am decidedly in the latter camp.

Martin Wolf, Financial Times, January 3, 2012

The eurozone sovereigns lack a true lender of last resort.

They are what Charles Goodhart of the London School of Economics calls "subsidiary sovereigns".

Martin Wolf, FT 2011-11-23

“Perhaps future historians will consider Maastricht a decisive step towards the emergence of a stable, European-wide power. Yet there is another, darker possibility ... The effort to bind states together may lead, instead, to a huge increase in frictions among them. If so, the event would meet the classical definition of tragedy: hubris (arrogance), ate (folly); nemesis (destruction).”

I wrote the above in the Financial Times almost 20 years ago.

My fears are coming true.

This crisis has done more than demonstrate that the initial design of the eurozone was defective, as most intelligent analysts then knew;

it has also revealed – and, in the process, exacerbated – a fundamental lack of trust, let alone sense of shared identity,

among the peoples locked together in what has become a marriage of inconvenience.

Martin Wolf, FT, 13 September 2011

Many ask whether high-income countries are at risk of a “double dip” recession. My answer is: no,

because the first one did not end.

The question is, rather, how much deeper and longer this recession or “contraction” might become.

Martin Wolf, Financial Times, 30 August 2011

I find it unforgivable that the last Irish government guaranteed bank debt so insouciantly

and that the rest of the European Union has supported this decision.

For a sovereign to destroy its own credit, to save creditors of its banks, is plainly wrong.

It does not make it better, but worse, that it is doing so largely to protect financial systems in other countries.

Martin Wolf, FT March 8 2011

Is it possible for the vast mass of humanity to enjoy the living standards of today’s high-income countries?

This is, arguably, the biggest question confronting humanity in the 21st century.

Martin Wolf, Financial Times June 10 2008

Some, knowing of my opposition to UK membership of the eurozone,

may suppose that I find some pleasure in these looming difficulties.

On the contrary, I fear the dangerous consequences.

Martin Wolf, January 19 2010

Moment of truth for the eurozone

Martin Wolf, Financial Times, 5 July, 2011

Why austerity alone risks a disaster

Martin Wolf, Financial Times June 28, 2011

When an outcome is inevitable, it is necessary to plan for it.

A default is a necessary, but not a sufficient, condition for a return to economic health.

Martin Wolf, Financial Times 21 June 2011

The debate over post-crisis monetary and fiscal policy has been heating up, on both sides of the Atlantic.

So who is right? It will come as no surprise that economists disagree deeply.

Martin Wolf, Financial Times, 2 June 2011

The eurozone, as designed, has failed.

It was based on a set of principles that have proved unworkable at the first contact with a financial and fiscal crisis.

It has only two options: to go forwards towards a closer union or backwards towards at least partial dissolution. This is what is at stake.

Martin Wolf, Financial Times, 31 May 2011

The underlying economics of the /Euro/crises are clear

During the boom years, a number of countries were able to borrow more and on more favourable terms than ever before. They, then, ran huge current account deficits.

The latter turned out to be the leading indicator of future crises, not fiscal deficits, as Germany’s mistaken conventional wisdom would have it.

Martin Wolf, Financial Times 18 May 2011

The problem with the strategy of imposing the burden on taxpayers in borrowing countries is that it is unlikely to work.

As an ever greater proportion of the financing ends up with official sources, the latter are likely to end up bearing politically explosive costs when debts are written off.

Martin Wolf, Financial Times 18 May 2011

The eurozone’s journey to defaults

Martin Wolf, Financial Times, May 10 2011

Martin Wolf argues that the eurozone faces a choice between permanent pro-cyclical adjustments, a break-up; or closer union

Financial Times 3/5 2011

The crisis has not proved a great turning point, so far.

The ratio of private gross debt to US gross domestic product rose from 123 per cent in 1981 to 293 per cent in 2009.

By the third quarter of last year, the ratio had fallen to 263 per cent.

Martin Wolf, February 1 2011

Between 2010 and 2015, the UK is forecast to have the third largest reduction in the share of government borrowing in national income among 29 high-income countries:

only Iceland and Ireland are to cut more.

The reduction in cyclically adjusted borrowing, is even forecast to be the second largest, after Greece.

Yet the UK has had no fiscal crisis. That makes its austerity remarkable.

Martin Wolf, FT 8/2 2011

Martin Wolf about low interest rates and leverage

December 9 2010

Under a floating exchange rate, some of the pressure would be relieved by a rising exchange rate in the boom and a falling rate in the bust.

With a pegged rate, the collapse in the currency would normally restore competitiveness and growth.

In a currency union, these safety valves are lost. Instead, we have a joint credit and competitiveness crisis.

The solution for the loss of competitiveness is a sharp fall in prices.

But that worsens the credit crisis: this, then, is debt deflation, as Ireland knows

Martin Wolf, FT November 30 2010

Imagine what would have happened, in the absence of the euro.

The exchange rate of the D-Mark would have exploded upwards

The absence of such shocks has greatly enhanced the prospects for the German recovery.

The creation of the eurozone was, for this reason alone, much more than a favour Germany did for its partners. It was also a big economic (not to mention political) gain for Germany.

German industrialists are clear on this, as is the government.

Martin Wolf, FT 7/9 2010

The conservative counter-revolution

The Great Recession almost certainly marks its end

Martin Wolf's Exchange August 23, 2010

Suppose that the US presidential election of 1932 had, in fact, taken place in 1930, at an early stage in the Great Depression.

Suppose, too, that Franklin Delano Roosevelt had won then, though not by the landslide of 1932. How different subsequent events might have been. The president might have watched helplessly as output and employment collapsed. The decades of Democratic dominance might not have happened.

On such chances the wheel of history turns.

Martin Wolf, FT, August 31 2010

As Raghuram Rajan of the University of Chicago Booth School of Business and former chief economist of the International Monetary Fund notes in a thought-provoking new book, the underlying “fault lines” are still with us.

Martin Wolf July 13 2010

Halting the financial doomsday machine

The combination of state insurance (which protects creditors)

with limited liability (which protects shareholders) creates a financial doomsday machine.

Martin Wolf, FT April 21 2010

China and Germany unite to impose global deflation

Germany is in a supposedly irrevocable currency union with some of its principal customers. It now wants them to deflate their way to prosperity in a world of chronically weak aggregate demand.

I am beginning to wonder whether the open global economy is going to survive this crisis.

The eurozone may also be in some danger.

Martin Wolf, FT March 16 2010

Establishing the EMF would require a new treaty

We must note an even greater difficulty. The notion that the big threat is fiscal indiscipline is false.

Martin Wolf FT March 9 2010

Anybody who looks carefully at the world economy will recognise that

a degree of monetary and fiscal stimulus

unprecedented in peacetime is all that is prodding it along

The conventional wisdom is that it will also be possible to manage a smooth exit.

Nothing seems less likely. So let us consider the endgame, instead.

Martin Wolf, FT February 23 2010

The Greek government has promised to slash its fiscal deficit

from an estimated 12.7 per cent of gross domestic product last year to 3 per cent in 2012.

Is it plausible that this will happen? Not very.

But Greece is merely the canary in the fiscal coal mine.

Other eurozone members are also under pressure to slash fiscal deficits.

What might such pressure do to vulnerable members, to the eurozone and to the world economy?

Martin Wolf, January 19 2010

Finanskrisens problem löstes genom att socialisera riskerna och efterfrågan

Det behövs ”en uthållig ökning av den privata sektorns efterfrågan”

"alla länder kan inte samtidigt ha exportledd tillväxt"

Martin Wolf intervjuad i SvD/e24 av Johan Myrsten 2010-01-16

Japan’s experience strongly suggests that even sustained fiscal deficits, zero interest rates and quantitative easing will not lead to soaring inflation in post-bubble economies suffering from excess capacity and a balance-sheet overhang, such as the US.

It also suggests that unwinding from such excesses is a long-term process.

Martin Wolf, January 12 2010

Det räcker med att läsa Martin Wolf

Varför skall vi vanliga dödliga småtyckare anstränga oss, läsa fundera och skriva?

Rolf Englund blog 6/1 2010

The eurozone’s next decade will be tough

Many have argued that, within a currency union, current account deficits do not matter

any more than between Yorkshire and Lancashire.

They are wrong.

Martin Wolf January 5 2010

Arvind Subramanian argues that economics has redeemed itself by rescuing the world economy from the crisis. I agree, but only up to a point.

These extraordinary interventions have not returned the patient to health. They have merely prevented him from dying.

We now must heal five chronic conditions, instead of survive last year’s brutal heart attack.

Martin Wolf, December 29 2009

The rest of the world was inclined to believe that the west, whatever its faults, knew what it was doing, particularly where running a market economy was concerned. But then the teacher failed the examination.

Thirty years of surging growth in private sector leverage, in the balance sheets of the financial sector and in notional profitability of the financial sector in the US and other high-income countries has ended in calamity.

The emergence of massive global current account “imbalances” has proved highly destabilising.

Martin Wolf December 23 2009

Having accumulated $2,273bn in foreign currency reserves, China has kept its exchange rate down, to a degree unmatched in world economic history.

China has, as a result, distorted its own economy and that of the rest of the world.

Martin Wolf, FT December 8 2009

Barack Obama, president of the US, met Hu Jintao, president of the People’s Republic of China,

This, then, was an opportunity for Mr Obama to tell some brutal truths. I hope he did

Martin Wolf, FT November 17 2009

Victory in the cold war was a start as well as an ending

In the case of this crisis, the failure lies not so much with the market system as a whole,

but with defects in the world’s financial and monetary systems.

Marin Wolf, FT November 10 2009

Time for a debate on immigration

Martin Wolf

November 5 2009

Why it is still too early to start withdrawing stimulus

Two groups of thinkers reject this viewpoint.

One argues that the economy is always in equilibrium.

Both the guilty and the innocent must suffer

Martin Wolf, FT September 8 2009

In contemporary banks, leverage of 30 to one is normal.

Higher leverage is not rare.

Reform of regulation has to start by altering incentives

Banks central activity is creating and trading assets of uncertain value, while their liabilities are, as we have been reminded, guaranteed by the state.

This is a licence to gamble with taxpayers’ money. The mystery is that crises erupt so rarely.

Martin Wolf, Financial Times, June 23 2009

What gave the Great Depression its name was a brutal decline over three years.

This time the world is applying the lessons taken from that event by John Maynard Keynes and Milton Friedman, the two most influential economists of the 20th century.

The policy response suggests that the disaster will not be repeated.

Martin Wolf, Financial Times, June 16 2009

Did inflation targeting fail?

Central banks have mostly escaped blame for the crisis.

How can it have gone so wrong? Also about The Taylor Rule

Martin Wolf, Financial Times, May 5 2009

What is needed is both a large increase in aggregate demand and

a shift in its distribution, away from chronic deficit countries, towards surplus ones.

Unless and until surplus countries recognise that this cannot continue,

no durable escape from the crisis will be achieved.

Martin Wolf, Financial Times March 31 2009

This is not a true market mechanism, because the government is subsidising the risk-bearing.

Prices may not prove low enough to entice buyers or high enough to satisfy sellers.

Martin Wolf, Financial Times March 24 2009

The scheme may improve the dire state of banks’ trading books.

This cannot be a bad thing, can it?

Well, yes, it can, if it gets in the way of more fundamental solutions,

because almost nobody – certainly not the Treasury – thinks this scheme will end the chronic under-capitalisation of US finance.

Indeed, it might make clearer how much further the assets held on longer-term banking books need to be written down.

The new plan seems to make sense if and only if the principal problem is illiquidity.

Two contrasting views have been held on what ails the financial system.

The first is that this is essentially a panic.

The second is that this is a problem of insolvency.

Martin Wolf, Financial Times 10/2 2009

The statement that systemic breakdowns are surprisingly rare

in the free-wheeling Anglo-Saxon model is false.

Martin Wolf February 9, 2009

Finally, there is inflation.

If central banks and governments are aggressive enough, they can generate inflation, which will lower the debt burden.

But they will imperil – if not terminate – the experiment with unbacked fiat (or man-made) money that started in 1971.

Martin Wolf, Financial Times January 27 2009

Keynes offers us the best way to think about the financial crisis

Martin Wolf, Financial Times, December 23 2008

Highly recommended

This is the endgame for the global imbalances

If the surplus countries do not expand domestic demand relative to potential output, the open world economy may even break down.

As in the 1930s, this is now a real danger.

Martin Wolf, Financial Times, December 2 2008

One might not expect much from economists, but one would surely expect them to warn us of a crisis on this scale.

Speech given by Martin Wolf, chief economics commentator, at the FT’s annual economists’ drinks party in London

Financial Times, 27/11 2008

These are historic times.

Collapse of an asset price bubble and consequent disintegration of the credit mechanism

More pressing than discretionary fiscal action is getting the banks to lend.

Martin Wolf, Financial Times 30/10 2008

Informed observers suggest an additional $1,500bn in capital might be needed.

So double this and assume it all comes from the state:

it would still “only” be 10 per cent of US and European GDP

Martin Wolf, Financial Times October 14 2008

As John Maynard Keynes is alleged to have said: “When the facts change, I change my mind. What do you do, sir?”

It took me a while – arguably, too long – to realise the full dangers.

Maybe it was errors at the US Treasury, particularly the decision to let Lehman fail, that triggered today’s panic.

Martin Wolf, FT, October 7 2008

The fundamental problem with the Paulson scheme is that it is neither a necessary nor an efficient solution.

It is not necessary, because the Federal Reserve is able to manage illiquidity through its many lender-of-last resort operations.

It is not efficient, because it can only deal with insolvency by buying bad assets at far above their true value, thereby guaranteeing big losses for taxpayers and providing an open-ended bail-out to the most irresponsible investors.

Martin Wolf, Financial Times, September 23 2008

Over the past few weeks three experiences have helped clear my mind on this crisis.

First, I reread Hyman Minsky’s masterpiece, Stabilizing an Unstable Economy.

Martin Wolf, Financial Times, September 16 2008

It is now almost a year since the US subprime crisis went global.

It has, in all likelihood, not even passed the end of its beginning.

The creditworthiness of the US government cannot be taken for granted.

Martin Wolf, Financial Times, July 15 2008

Bank for International Settlements annual report

“How,” asks the report, “could a huge shadow banking system emerge without provoking clear statements of official concern?”

How, indeed?

How big are the risks now? The answer is: very large.

As I argued in a speech at a BIS conference last week...

Martin Wolf, Financial Times, July 1 2008

How to see world economy through two crises

Martin Wolf, Financial Times, June 24, 2008

How imbalances led to credit crunch and inflation

Martin Wolf, Financial Times, June 17, 2008

How well can an economy long characterised by soaring house prices, exploding debt and a dynamic financial sector adjust to a new world?

Martin Wolf, Financial Times May 1 2008

How do we persuade citizens that the rise of the emerging countries, the brightest story of our era, is to be welcomed, rather than resented or even resisted,

when what they experience is financial disarray, falling house prices, recession and soaring costs of essential commodities?

Martin Wolf, Financial Times, April 22 2008

First, anybody who thinks it is a duty of the state to help keep housing expensive is crazy;

second, policymakers should respond only to clear market failures; and,

third, with a floating exchange rate and an independent central bank, the UK can weather the storm if it keeps its head.

Martin Wolf, Financial Times April 17 2008

Fed bailout of Bear Stearns

Remember Friday March 14 2008

it was the day the dream of global free-market capitalism died.

Martin Wolf, Financial Times, March 26 2008

The financial system is a subsidiary of the state.

A creditworthy government can and will mount a rescue.

That is both the advantage – and the drawback – of contemporary financial

capitalism.

Martin Wolf, Financial Times February 26 2008

Highly recommended

America’s economy risks mother of all meltdowns

The connection between the bursting of the housing bubble and the fragility of the financial system

has created huge dangers, for the US and the rest of the world.

Martin Wolf, Financial Times, February 19 2008

In times of panic, grown-ups keep their nerve.

In a financial crisis, central banks must be the grown-ups.

Martin Wolf

Is the 2007 US Sub-Prime Financial Crisis so Different?

(Different from the Debt Crisis of the 80's?)

Martin Wolf, FT January 8 2008

These are historic moments for the world economy.

First and most important, what is happening in credit markets today is a huge blow to the credibility of the Anglo-Saxon model of transactions-orientated financial capitalism.

A mixture of crony capitalism and gross incompetence has been on display in the core financial markets of New York and London.

Martin Wolf, FT 12/12 2007

The central bank helicopters are planning a co-ordinated drop of liquidity on troubled market waters.

One point is clear: central banks must be pretty worried to take such a joint action.

Martin Wolf. FT December 12 2007 18:01

The public sector subsidises the banks risk-taking. It does so because banks provide a utility.

What the banks give in return, however, is gung-ho speculation.

Martin Wolf, FT November 27 2007

Sverige bör, liksom England, hålla sig utanför euron så länge som möjligt.

Det säger Martin Wolf, biträdande chefredaktör på Financial Times

Ekonominyheterna 4/12 2006

Let us call a spade a spade.

The blame for the vulnerability of Northern Rock lies with its management

Would it not be better to let mismanaged institutions go under, while protecting small depositors effectively?

Answer: yes, it would.

Martin Wolf, Financial Times November 15 2007

Questions and answers on the debt crisis

Martin Wolf, September 5 2007

If holders of the dollar conclude it is no longer a secure store of value

they will dump both the currency and assets dependent on its future value.

If that were to happen, the Fed would confront a dreadful dilemma

– whether or not to cut rates as the dollar plunged and long-term interest rates soared.

Martin Wolf, Financial Times 26/9 2007

Central banks should not rescue fools

Martin Wolf, Financial Times, August 29 2007

The Fed can indeed be accused of being a serial bubble-blower.

But this is not because it has been managed by incompetents.

It is because it has been managed by competent people responding to exceptional circumstances.

Martin Wolf, August 22 2007

Fear makes a welcome return

This is not new. It is as old as financial capitalism itself.

The late Hyman Minsky, who taught at the University of California, Berkeley, laid down the canonical model.

Martin Wolf, Financial Times 15/8 2007

Posterity will regard the economic performance we are now witnessing as a golden age.

It will also know, although we do not, how long this era lasts.

Martin Wolf, FT, 2/5 2007

The G7 should, instead, be replaced by a multilateral body that can address such issues more effectively.

Martin Wolf FT 30/5 2007

Globalisation

How to promote employment while protecting the low-paid

The Globalization of Labor, IMF World Economic Outlook

Martin Wolf, FT, April 11 2007

Equities look overvalued,

but where is the turning point?

Martin Wolf, Financial Times, March 7, 2007

Sven Rydenfelt-föreläsning

Martin Wolf om varför globaliseringen fungerar

Timbro 19/1 2005

För åttonde gången anordnade Timbro en föreläsning för att hylla Sven Rydenfelts långa och framgångsrika kamp för de liberala värdena. Bland tidigare föreläsare kan nämnas Per Ahlmark och Deepak Lal. Till årets föreläsning var Martin Wolf inbjuden. Inför tvåhundrafemtio åhörare talade han om globaliseringens framgångar.

Sven Rydenfelt - Sven Rydenfelt om EMU

Book review:

The Writing on the Wall: China and the West in the 21st Century by Will Hutton

Hutton takes on the most important political and economic story of our time. He has also produced a thought-provoking, wide-ranging and largely correct analysis.

The book advances five fundamental and, in my view, fundamentally correct propositions.

First, for all its manifest achievements, the Chinese attempt to marry a communist party-state with the market is unsustainable.

Martin Wolf 4/2 2007

Can 1.5m people be wrong? Yes, they can.

In a representative democracy, the government can also ignore them. It should do so.

Road pricing is not only a good idea, but an inevitable one.

Martin Wolf, Financial Times 16/2 2007

Why America will need some elements of a welfare state

Martin Wolf, Financial Times, 14/2 2007

The more persuasive is this “liquidity” story, the more plausible it becomes that the correction is going to be more painful than conventional wisdom believes.

Commenting on Wolfgang Münchau and Lawrence Summers

Martin Wolf, FT 10/1 2007

UK housing boom will end, but how

Will it end with a bang or a whimper? That is indeed the big question.

Martin Wolf, FT 24/11 2006

Why have markets reached their exposed position? The answer is that success breeds excess.

This is the argument of a fascinating new paper from William White, economic adviser to the Bank for International Settlements.

Martin Wolf, Financial Times 24/5 2006

Let dollar fall or risk global disorder

Is it possible to reduce the US deficit substantially without exchange-rate changes. The answer is that it would be possible, but catastrophic for all participants, because it would demand a deep US recession

Martin Wolf, Financial Times, May 9 2006

Why should we remain concerned about global imbalances? The answer is that they are undesirable, cannot continue indefinitely and the longer they last, the bigger and more painful the adjustment will be.

What is undesirable ought to change. What is unsustainable will change. What is dangerous must change. Yet, if the world is to avoid a serious recession, adjustment must start in the surplus countries.

Martin Wolf, Financial Times 29/3 2006

As two distinguished financial economists, John Campbell of Harvard and Robert Shiller of Yale, have shown,

returns demonstrate “negative serial correlation”.*

They revert to average valuations.

Martin Wolf, Financial Times 22/3 2006

What could go wrong and, more important, whether the risks of its doing so are adequately priced. They are not.

On a cyclically adjusted basis, the US stock market is as highly valued as in any period of the past 120 years, except the late 1920s and the late 1990s.

Martin Wolf 3/1 2006

The late Herbert Stein is famous for saying that what can’t go on forever, won’t.

This then is a world of strong growth.

Martin Wolf, Finacial Times 21/12 2005

Dear Ben, Congratulations on your nomination as chairman of the Federal Reserve

Do not believe for a moment that targeting inflation is all there is to being a successful Fed chairman

You will need to react strongly to low probability, high cost dangers.

Martin Wolf, Financial Times, October 26 2005

It is little wonder that Mr Greenspan has become an almost legendary figure. Yet how good has his performance been and what lessons does his tenure bequeath?

Mr Volcker had to crush inflation. Mr Greenspan had merely to keep the show on the road.

Another reason for questioning the unique sagacity of the chairman is that low inflation has broken out all over the world.

Surprisingly for a man once known as a gold bug and disciple of Ayn Rand’s libertarian philosophy, Mr Greenspan has emerged as the policymaker closest in spirit to Maynard Keynes.

Martin Wolf, Financial Times, 19/10 2005

It cannot go on forever. The question is how and when it will stop

There are risks of a much more abrupt reversal, triggered by a big increase in protectionism in the US, a sudden decline in the world's demand for US assets or, more probably, both together. This could generate a sharp slowdown in the US and the rest of the world, possibly even a world recession.

We do know that the explosive increase in US current account deficits cannot continue indefinitely. It is possible that a smooth adjustment will indeed occur. It is also quite likely that the ultimate adjustment will be both swift and brutal.

Martin Wolf, Financial Times 8/10 2005

The IEA argues that remaining oil reserves could cover only 70 years

at the average annual consumption between 2003 and 2030.

Martin Wolf, Financial Times, 22/6 2005

As Maurice Obstfeld of the University of California at Berkeley and Kenneth Rogoff of Harvard note,

a big reduction in the US current account deficit that does not include sizeable exchange rate and macroeconomic adjustments in Asia

would impose a devastating shock on the already troubled eurozone.

Martin Wolf, Financial Times, June 29 2005

The rejection of the constitutional treaty by the voters of France and the Netherlands gives the European Union a chance to reconsider its future.

Those in charge should realise that they have made a mistake.

Their hope was for an EU that was more efficient and more democratic. But there is a conflict between these two objectives.

Now it is possible to embark on a new journey that recognises this truth.

Martin Wolf Financial Times June 15 2005

Strange things are happening in the world economy: falling interest rates on long-term securities, declining spreads between returns on safe and riskier assets, large fiscal deficits and huge global current account “imbalances” should not, in normal circumstances, coincide. So what is going on?

The answer, in a nutshell, is a global excess of desired savings against the background of weak investment, low inflation and ever more integrated economies.

To understand the present we need to go back to the 1930s. The “paradox of thrift” was the most counterintuitive and, to the classically trained economist, morally, theoretically and practically objectionable idea in John Maynard Keynes’ General Theory of Employment, Interest and Money, published in 1936, in response to the Great Depression.

Martin Wolf Financial Times June 13 2005

It is essential for the UK to avoid joining the eurozone, which looks quite as dysfunctional as prescient(perceptive, cautious, foresighted) critics feared,

About a recent book from the Institute of Economic Affairs: Should Britain Leave the EU? An Economic Analysis of a Troubled Relationship, Patrick Minford and others

Martin Wolf, FT 3/6 2005

Embrace diversity and decentralisation. That is the conclusion

The countries of Europe are different. They cannot be shoe-horned into a single political process.

The French, for example, want to keep their high-cost, high-regulation leviathan. Let them do so. The UK has, rightly, chosen a different path.

Martin Wolf Financial Times 3/6 2005

Let us think the unthinkable:

Could the eurozone disintegrate?

The answer is yes.

If /Italy/ fails to rise to the challenge it confronts, a default or even a forced withdrawal

from the eurozone is perfectly conceivable.

Martin Wolf Financial Times 25/5 2005

The new constitution, with its nonsense about a "social union", makes the wrong choices.

Within an integrated labour market it is impossible for one region to offer much better benefits than others without generating a ruinously costly inflow of benefit seekers.

That is what happened to New York in the 1970s.

This is why welfare states must work at the level of the entire labour market.

Martin Wolf Financial Times 6/4 2005

The growing external deficits of the world's "sole superpower" have put the global economy

on a path that is not merely unsustainable but also dangerously so.

US and Asian policymakers seem determined to take no decisive action in response.

This is understandable, but a big mistake.

Martin Wolf Financial Times December 8 2004

Few, if any, leaders are prepared to recognise a simple truth: neither European enlargement nor monetary union, for that matter, can succeed without far more flexible labour markets.

Back in 1990, we should remember, the then West Germany absorbed the former East Germany.

So what can be learnt from that experience?

Martin Wolf, Financial Times 30/3 2005

Very Important Article

To bring about a substantial reduction in the external deficit without a deep recession, the US needs a huge change in internal relative prices.

About Maurice Obstfeld and Kenneth Rogoff The Unsustainable US Current Account Position Revealed

Martin Wolf Financial Times 1/12 2004

Den 19 januari 2005 ger Martin Wolf den årliga Sven Rydenfelt-föreläsningen i Lund.

Läs mer hos Timbro.

Adjusting to the dollar's inevitable fall

Altering the path of the US external accounts, while sustaining global economic activity, is among the biggest challenges now confronting policymakers.

Martin Wolf Financial Times November 24 2004

America on the comfortable path to ruin

These two facts - the rest of the world's surplus output and the US goal of full employment - explain the global macro-economic picture

Martin Wolf, Financial Times, August 18 2004

America's dangerous deficit

Since the high and rising

US current account deficit is one of the most remarkable features of the world

economy, deciding whether it matters is of some significance

Martin Wolf, Financial Times August 24 2004

There are big medium-term risks ahead

Global

macroeconomic imbalances, the impact of a rising Asia, protectionism and

vulnerability to terrorist outrages

Martin Wolf 20/7 2004

A housing market collapse draws nearer

Martin Wolf, Financial Times 16/4

2004

Bubbles have three stages: expansionary; then contractionary; and,

finally, perhaps inflationary.

The world economy is now in the second stage.

That is why today's worry is deflation. But it is unlikely to stay there for

ever. Ultimately, efforts to ward off post-bubble deflation risk creating its

opposite.

Martin Wolf Financial Times 28/5 2003

The dollar, said John Connolly, treasury secretary

to Richard Nixon, "is our currency, but your problem".

Gerhard

Schröder, Germany's chancellor, knows what he meant

A world in which

macroeconomic health can be achieved only at the expense of ever greater

private and public debt accumulation in its biggest and richest economy is

unstable. It is also perverse.

Martin Wolf,

Financial Times 1/3 2004

Martin Wolf, A testing

year for the world

Financial Times, January 3, 2001-01-03

The first

test is for Alan Greenspan - The second test is of the “new economy”

- The third test is for the US stock market

Risking a hard

landing

Martin Wolf , Financial Times, December 6, 2000

Europe's constitutional dilemma

Martin Wolf, FT, July 4, 2000

Analysis of companies' net

worth suggests that Wall Street's high-flying stocks remain fundamentally

over-valued

From Marintin Wolf, FT, June 27, 2000

Growing too fast for

comfort

A rapid rise in productivity has raised the US growth rate but

brought with it an unsustainable level of demand

Martin Wolf, FT, 4 Apr

2000 Something remarkable is happening in the US economy.

To some it is a

bright "new economy". To others it is the bubble to end all bubbles.

US ECONOMY: Walking on

troubled waters

Martin Wolf, FT, January 12, 2000

Dear Mr

Greenspan, Congratulations on your renomination as chairman of the Federal

Reserve.

A

miraculous error

Martin Wolf, FT, September 29 1999

The Federal

Reserve inadvertently allowed unsustainable growth in the US,

but this

helped to offset the collapse of demand elsewhere and avoid deep world

recession

Martin Wolf: Threats of

depression

Financial Times 98-08-26

Martin Wolf on NAIRU, May, 1999

The

Risks and Rewards of EMU

Martin Wolf, Financial Times, May 26, 1999

German handicap

Martin Wolf, Financial Times, March 31, 1999

Few have realised the most

dangerous feature of Emu:

it has locked Germany into a seriously

uncompetitive real exchange rate