Home

Economics - Cataclysm -

Stockmarket chrashes - Finanskrisen The Great Recessiom - Secular Stagnation

ZIRP - QE

Niall Ferguson, FT February 10 2010

John Authers, FT 30 January 2018

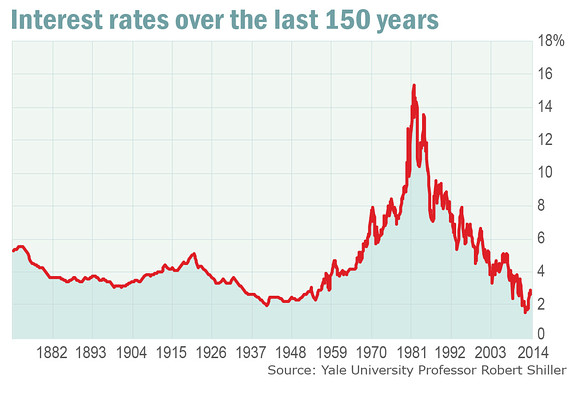

Räntorna är de lägsta på åtminstone 5 000 år.

Detta betyder att priset på obligationer är de högsta på 5 000 år.

Andreas Cervenka, SvD 27 januari 2016

Rolf Englund blog 13 augusti 2013

zc

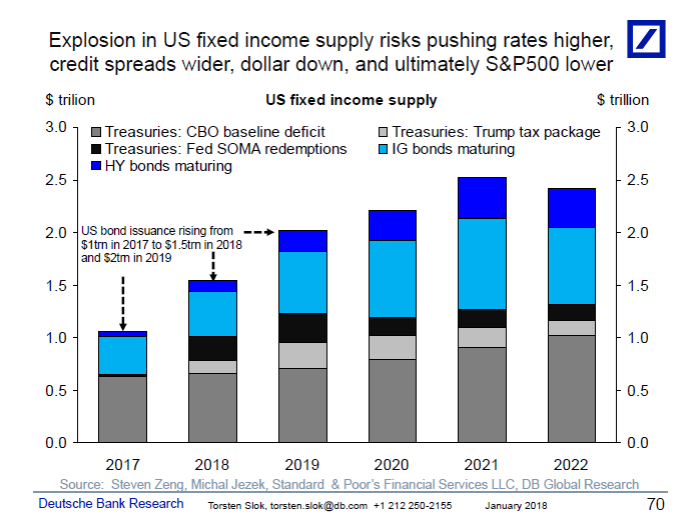

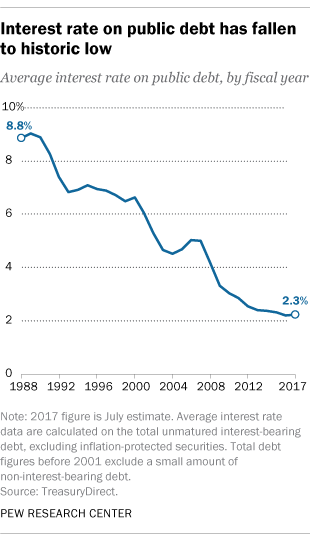

Investors start to fret about ballooning US public debt

The CBO calculates that servicing costs will triple in size to nearly $1tn by 2028

Gillian Tett FT 8 November 2018

US government currently pays $1.43bn each day (yes, day) to service its public debt — 10 times more than any other G7 country (Italy is a distant second in this grim league).

What is doubly thought-provoking is that this $1bn bill has materialised when interest rates are still fairly low by historical standards. And that invites a crucial question for the US Congress: what will happen to that debt, and servicing costs, if (or when) interest rates climb to a more normal level?

Until recently, neither investors nor voters seemed to care particularly.

US government deficit will be (drumroll, please) approximately $1.4 trillion per year for the next five years, which will mean $29 trillion total debt by 2024.

And that’s without a recession. Throw in a recession, and we’ll get to $30 trillion long before then.

Stocks just a sideshow to the real drama of bond markets

Banking’s diminished role in lending has enormous, still under-appreciated implications

Robin Wiggglesworth FT 2 November 2018

U.S. inflation is the world's most important economic variable.

CNBC 8 October 2018

Starting this month and for an indefinite period, the Fed will be dumping existing Treasury debt into the bond pits at a $600 billion rate---even as the borrowing requirement during the year now underway is projected to soar toward the $1.2 trillion mark.

That means there will be $1.8 trillion of homeless Federal debt swirling around the financial markets,---and it will eventually be absorbed.

The huge question, of course, is a what yield

David Stockman October 5th, 2018

Stockman: The mother of all yield shocks

The ECB has bought €2.5tn of eurozone debt securities under a QE programme that is set to stop at the end of this year.

The central bank’s monthly purchases halve to €15bn of bonds in October.

FT 4 October 2018

The chance of an inflation shock may be higher than you think

Dan McCrum FT Alphaville 13 August 2018

The funny thing is that Trump has an overwhelming case.

US experienced its last annual trade (goods) surplus in 1975.

David Stockman 5 March 2018

$2.34tn of treasuries will be sold in the next two years.

The main, obsessive focus for debate around the Fed right now is whether it will raise policy rates three or four times this year.

Gillian Tett 7 June 2018

But if Urjit Patel, the governor of India’s central bank, is correct, this obsession with US interest rates misses the point.

The US central bank is planning to shed trillions in assets, but markets are calm

Gillian Tett FT 1 March 2018

This turnround is remarkable, particularly now that we are in uncharted waters.

More specifically, after quadrupling its balance sheet between 2009 and 2017, the Fed is now trying to shed an eye-popping $2tn of assets in a mere four years.

Nothing remotely like that has ever been attempted by a central bank.

Wall Street players - including the financial press - have been prospering inside the Bubble so long that they do indeed think it is reality.

We had a close encounter yesterday during an appearance on CNBC.

David Stockman 28 February 2018

The thirty-something anchors were shocked to hear that Washington's upcoming $1.8 trillion 2019 Treasury borrowing might generate a resounding "yield shock",

thereby upending the current huge stock market bubble where 4%+ bond yields are most definitely not priced in.

Inflation risk spooks equity markets (nice charts)

Lars Christensen, 14 February 2018

Increase in US inflation sparks bond market sell-off

Treasury yields hit 4-year highs as Wall St fears sharper rate increases

FT 15 February 2018

Man Who Says "Bubbles Only Identified When They Burst" Detects Bubbles

Alan Greenspan says there are "Bubbles in Stocks and Bonds".

Mike "Mish" Shedlock, 2 February 2018

Vincent Deluard of INTL FCStone

I believe that 2018 will be the mirror opposite of 1999.

A triple squeeze will drain global excess savings: the U.S. will become the world’s largest oil producer,

Germany will abandon its policy of budget surpluses, and India’s economic growth will outstrip China’s.

The three gluts arose together, and together they will vanish.

Who will supply the world’s capital after the retirement of these massive hoarders?

John Authers, FT 7 February 2018

It will take much higher yields to convince Americans and other impecunious borrowers to quit their decade-long addiction to foreign savings. Hence, my answer to the original question is that yields will rise much higher, and that the bond bear market will last much longer.

I hate to admit this, but I think I have found a good historical parallel for what is happening in the markets.

And it is with spring and summer of 2007, on the eve of the credit crisis.

John Authers, FT 6 February 2018

No hedge fund that wishes to survive is going to sit patiently on their repo silos at 95% leverage

To the contrary they are likely to not only begin selling with malice aforethought,

but also to actually pivot to the other side.

David Stockman, Friday, February 2nd, 2018

That is, start "shorting" what in effect the Fed has announced it will be shorting to the tune of $600 billion per year commencing next October.

Rädslan sprider sig efter apokalyptiskt börstapp

SvD 4 februari 2018

Tappet med 666 punkter i fredags fick Twitter att explodera. Sifferkombinationen är nämligen en biblisk symbol för ett odjur som visar sig under apokalypsen: "Number of the beast".

A bond market shock of biblical proportions is now just around the corner

David Stockman, Thursday, February 1st, 2018

At the same time, the casino gamblers have built an edifice of grotesquely inflated financial asset prices that depend entirely on the ultra-low yields and cap rates that have been confected by the central banks and their front runners.

The pity is that a bond market shock of biblical proportions is now just around the corner---yet neither end of the Acela Corridor sees it coming.

So now is the time to head for the emergency exits.

---

Acela is Amtrak's flagship service along the Northeast Corridor (NEC) in the Northeastern United States

between Washington, D.C. and Boston via 14 intermediate stops including Baltimore, Philadelphia, and New York City. /Wikipedia

US bond market sell-off deepens

10-year Treasury yield rises to fresh four-year high at just under 2.8%

FT 2 February 2018

“We think that the current level of rates do not yet pose a major risk for equity multiples,” Marko Kolanovic, a senior strategist at JPMorgan, wrote in a note on Thursday.

Cash it's not about a return on your money; it's about return of your money.

Mitch Goldberg, CNBC 1 February 2018

The next global economic downturn – probably in 2019 – will be traumatic for everybody,

given that we have already used up our monetary and fiscal powder, and exhausted popular consent for globalisation.

Ambrose Evans-Pritchard 31 January 2018

Resistance is broken. Now what?

US Treasury yields on Monday broke through what had long been billed as an important point of resistance, at 2.66 per cent, and rose above 2.7 per cent.

That appeared to break the fabled long-term downtrend in 10-year Treasury yields

John Authers, FT 30 January 2018

Big questions to be answered concern timing, consequences and even what is meant by ‘normalisation’

Prophets of doom predict (or hope) that the world will at last suffer for the sins of activist central bankers.

Martin Wolf, FT 21 January 2018, state of the art article with nice charts

On timing, the BIS is far from alone in arguing that policy should have tightened long ago.

If central banks do not deliver a robust economic take-off, they will surely fail to achieve the policy room they would like. Yet, even if they do achieve such a take-off, they may still not gain that room because the new normal turns out different from the old one. Worse, if pessimists are right, the policies used to achieve take-off may raise the chances of a subsequent crisis.

Wells Fargo's head of interest rate strategy is detecting a major trouble spot in the bond market.

Michael Schumacher's chief concern right now: Who's going to buy all those extra Treasury notes?

CNBC, 25 Jan 2018

---

As the US Treasury gets set to issue upwards of $1.2 trillion of new bonds in the fiscal year (2019) starting in October

and the Fed ramps its bond dumping rate to $600 billion per year, the question recurs:

Who is going to buy $1.8 trillion of bonds within a 12-month period at current rates (2.65%).

David Stockman 26 January 2018

We'd lay odds on nobody.

And we'd further bet that the Donald's delusional triumphalism at Davos will soon be mocked by the bond market carnage that lies just around the bend.

zerohedge.com/news/2018-01-22/we-cant-pretend-interest-payments-arent-rising-anymore

Treasury Department to issue $1 trillion of debt in 2018,

almost double the amount seen in 2017

Market Watch 16 January 2018

“All the market indicators right now look very similar to what we saw before the Lehman crisis,

but the lesson has somehow been forgotten,” said William White

Ambrose Evans-Pritchard, 22 January 2018

The latest stability report by the US Treasury’s Office of Financial Research (OFR) warned that a 100 basis point rate rise would slash $1.2 trillion of value from the Barclays US Aggregate Bond Index, with further losses once junk bonds, fixed-rate mortgages, and derivatives are included.

Margin debt on Wall Street has risen to an all-time high, as has the share of risky bonds with minimal protection.

William White is the Swiss-based head of the OECD’s review board and ex-chief economist for the Bank for International Settlements.

Bill White world’s central banks were making a mistake with their single-minded focus on monetary policy, Mauldin

Starting in 2003, officials at the Basel-based institution, started to warn that the world economy was plagued by excessive levels of debt.

This made the system dangerously distorted; so went the off-the-record murmurs from men such as William White (a genial Canadian, BIS chief economist) and Claudio Borio (an Italian, who was White’s deputy).

Gillian Tett

Derivatives contracts indicate that investors believe the 10-year Treasury yield

will be below the 3 per cent mark in two, five and even 10 years’ time.

Robin Wigglesworth, FT 12 January 2018

Equivalent German and Japanese bond futures show that investors think their benchmark bond yields will stay below 2 per cent and 1 per cent respectively over the same timeframes.

The global bond rout has begun, leaving equities on borrowed time

Ambrose Evans-Pritchard, 10 JANUARY 2018

Nobody knows where the pain threshold lies for a global financial system with a record debt ratio of 332pc of GDP – up 56 percentage points even since the Lehman bubble – and with an unprecedented sensitivity to US monetary policy through offshore dollar funding markets.

Nor does anybody know what the breaking point is for a world that has been lured into an "intertemporal" trap by a quarter century of central bank ideology, reducing the Wicksellian natural rate of interest to levels never seen before in the history of modern markets.

We are flying blind.

The Moment of Truth for the Secular Bond Bull Market Has Arrived

John Mauldin 10 January 2018

Anyone who started investing after 1981 has never experienced a bear market in Treasuries.

The vast majority of today’s investors have only ever invested when Treasury yields are falling.

The $50 Trillion Question for Bonds

Bloomberg 10 January 2018

While calling the turn in bonds, especially in Europe, has been a widow-making trade in recent years, recent moves certainly look like the trend is no longer your friend.

Bond guru Bill Gross signals a new era for Treasury markets

The bond bear market is finally upon us after more than 25 years, bond guru Bill Gross said

CNBC 10 January 2018

Stock valuations are high by historical standards, the report noted. The cyclically adjusted price-to-earnings ratio of the S&P 500 is at its 97th percentile relative to the last 130 years.

In the bond market, sensitivity of bond prices to interest rate moves has steadily increased since the crisis, the report said.

In early 2017, the duration of the Barclays U.S. Aggregate Bond Index reached an all-time high of just over six years.

At current levels of duration, a 1 percentage point increase in interest rates would lead to a decline of almost $1.2 trillion in the securities underlying the index.

The risks from a big stock or bond market drop ‘are high and rising,’ government watchdog says

https://www.marketwatch.com/2017-12-05

The Office of Financial Research (OFR)

Republican tax package will definitively put an end to 36-year upswing for Treasuries

With hindsight, we can identify the inflection point as July 5 this year when 10-year Treasuries closed at a rock bottom yield of 1.37 per cent.

John Plender 5 December 2017

While William McChesney Martin had famously remarked that the task of central bankers was to take away the punchbowl just as the party gets going, monetary policy was reactive rather than pre-emptive and conspicuously slow

We’re in bubble territory again, but this time might be different

Martin Wolf, FT 10 November 2017

“The real problem is that when the bond-market bubble collapses, long-term interest rates will rise,” Greenspan said.

“We are moving into a different phase of the economy -- to a stagflation not seen since the 1970s.

That is not good for asset prices.”

Bloomberg 1 August 2017

“By any measure, real long-term interest rates are much too low and therefore unsustainable,” the former Federal Reserve chairman, 91, said in an interview.

Hedge funds that built up bullish long-end Treasury wagers to the highest outright level since 2008 are

rushing for the exit as a government bond rout that started in Europe following a weak French debt auction

is spreading to the U.S. market.

Bloomberg 6 July 2017

This may be just the beginning according to DoubleLine Capital’s Chief Executive Officer Jeffrey Gundlach

Keep Eye on Sovereign Debt for Next Minsky Moment

The recent turmoil in bonds offers a good example of what's to come as the global economy recovers

and central bankers curb stimulus.

Alberto Gallo, Bloomberg 5 juli 2017

This time around the issue isn't only excess debt -- it is also that prolonged loose monetary policy may have left us with at least three collateral effects.

The first is a misallocation of economic resources.

The second is a rise in wealth inequality, where the wealth effect from rising asset prices benefited asset owners and the old more than the young and the poor.

The third is a suppression of risk premia and volatility across financial markets.

But the biggest worry for investors is that the calm environment established by QE may conceal a storm, and that such extraordinary measures may have encouraged the formation of asset bubbles ready to pop when loose monetary policy ends.

Unlike in 2008, the culprit isn't low-quality subprime mortgage debt, but sovereign bond markets.

Bob Michele, head of fixed income for JPMorgan Asset Management, “What they were trying to communicate, is that the 30-year bull market is over and things should go back to normal”.

In this case normal means higher interest rates, which are bad for bond prices, and leads to the second conclusion:

after three decades of mostly falling bond yields, changing course is extremely difficult when prices for trillions of dollars worth of assets hang on every word.

FT 30 June 2017

George Saravelos at Deutsche Bank, who says that out of Sintra emerged “a co-ordinated shift by developed world central banks in a more hawkish direction”. He dubs it “the Sintra pact”.

For investors scrambling to keep pace with a hawkish shift in the world’s biggest central banks,

the second half of 2017 just got a lot more interesting.

Bloomberg 29 June 2017

wikipedia.org/wiki/May_you_live_in_interesting_times

The Federal Reserve might be doing the right thing for the U.S. economy by moving to bring interest rates back up to normal.

But for foreign companies and governments that have borrowed trillions of U.S. dollars, the adjustment could be painful.

Mark Whitehouse, Bloomberg 19 March 2017

Economists may warn that the combination of Trump’s protectionism, big tax cuts, and uncontrolled government borrowing,

coming at a time when the US economy is already near full employment, will ultimately fuel inflationary pressure.

But financial markets simply do not believe this message.

Anatole Kaletskys Project Syndicate 27 March 2018

Both economic analysis and decades of past experience suggest that long-term interest rates tend to fluctuate around the rate of nominal GDP growth.

This rule of thumb implies 30-year rates in the 4-5% range.

Trump’s election has almost certainly ended the 35-year trend of disinflation and declining rates that began in 1981,

and that has been the dominant influence on economic conditions and asset prices worldwide.

But investors and policymakers don’t believe it yet.

Anatole Kaletsky, Project Syndicate 30 January 2017

The Daily Prophet:

Why Is China Dumping Treasuries?

Robert Burgess, Bloomberg 19 January 2017 with nice charts

Foreign investors would hardly want to buy dollar-denominated assets such as Treasuries if they suspected the government actively wanted to depreciate its currency.

In today's auction by the U.S. government of $13 billion in 10-year Treasury

Inflation-Protected Securities demand was so great that primary dealers were left with about 16 percent of the bonds,

the lowest on record in data going back to 2003.

Steering Clear:

How to Avoid a Debt Crisis and Secure Our Economic Future

2015 by Peter G. Peterson

The real number to keep an eye on is 2.6 per cent yield on the 10-year Treasury note, says Bill Gross.

The low-for-long era is over.

This summer, the BoJ and then the ECB both changed their mantra

from whatever it takes to less is more targeting steeper yield curves

and the transmission mechanism of stimulus to the real economy,

moving away from unlimited asset purchases.

Alberto Gallo, FT 27 December 2016

They are right in doing so.

Monetary stimulus without appropriate fiscal action

encouraged misallocation of resources to zombie firms and banks that should otherwise restructure;

created asset bubbles in high dividend equities, property and precious metals, as well as art and collectibles;

and widened the gap in relative wealth between the haves and the have-nots.

- Jag tycker det är skriande uppenbart att räntan världen över är för låg

och att en större del av stimulanserna borde ske via finanspolitiken,

skrev jag i december 2009.

Today’s young Wall Street hotshots have never seen anything like that.

To them the jump from 0.5% to 0.75% must seem like a big deal.

It’s really not.

America’s growing strong dollar conundrum poses a threat to Mr Trump’s vows to slash the trade deficit

FT 13 December 2016

Repeat After me: “Bonds Don’t Necessarily Lose Value When Rates Rise”

Most people don’t apply the right maturity and/or duration to their portfolios

Cullen Roche

What is the Worst Case Scenario for Bonds?

Cullen Roche

November 2018 will mark the tenth anniversary of quantitative easing (QE)

— undoubtedly the boldest policy experiment in the modern history of central banking.

Stephen S. Roach 30 July 2018

The only thing comparable to QE was the US Federal Reserve’s anti-inflation campaign of 1979-1980, orchestrated by the Fed’s then-chair, Paul Volcker.

But that earlier effort entailed a major adjustment in interest rates via conventional monetary policy.

By contrast, the Fed’s QE balance-sheet adjustments were unconventional and, therefore, untested from the start.

Era of quantitative easing is drawing to a close

arguably the greatest monetary policy experiment since John Law began dabbling with fiat paper money in France

Robin Wigglesworth, FT 8 December 2016

Markets have already decided that 2016 is the year when the economic stimulus baton switches hands from central banks to governments.

The Mississippi Bubble of 1720 and the European Debt Crisis

Liberty Street Economics

internetional.se/shares.htm#tulip05

Interest rates follow very long-term cycles.

Now we need real demand and moderate inflation to grow us out of this predicament,

as we can’t rely on corporate investment (other than in stock buybacks, dividends and acquisitions)

or consumer spending (if consumers don’t have the money to spend).

US Treasuries sell-off continues as inflation fears mount

Dollar at 13-year high after economic data bolster case for rate rise

FT 23 November 2016

Reinforced the view that the multi-decade bond bull market has reached a turning point.

Global Bonds Suffer Biggest Crash In Over 25 Years

zerohedge 18 November 2016

Bond-market losses will be huge, and retirees are most vulnerable

"Investors unprepared for rising interest rates"

So says Ric Edelman, executive chairman of Edelman Financial Services a financial planning firm that manages $17 billion

MarketWatch 17 november 2016

Barron’s named the firm the nation’s No. 1 independent financial advisor in 2009, 2010, and 2012.

He is also author of the recently updated bestseller “Rescue Your Money.”

He is also author of the recently updated bestseller “Rescue Your Money.”

Investors unprepared for rising interest rates, top financial adviser Ric Edelman tells Howard GoldWhile people think they’re being prudent by avoiding stocks, they are actually taking on more risk piling into bonds.

Bond valuations are the Achilles heel of markets

Investors seem to have concluded that this is the beginning of the end of unconventional central bank monetary policy.

Investors can, of course, change their minds.

John Plender, 1 November 2016

The equity market is less obviously in bubble territory, though it remains remarkably buoyant on the back of poor corporate earnings. On a cyclically adjusted basis price earnings ratios look very expensive.

Yet the market is supported by a large volume of corporate buying through takeovers and buybacks.

Now, some strategists and investors think that the linkers

— inflation-linked government bonds — trade is back on

FT 20 October 2016

But

Excellent article by John Authers about Why bond yields are so low

FT 20 October 2016

How can anyone make sense of today’s markets?

Gillian Tett, FT 14 October 2016

By reducing the incomes of retirees and terrifying near-retirees,

the Fed successfully reduced economic activity.

John Mauldin 9 October 2016

Ray Dalio Warns A 1% Rise In Yields Would Lead To Trillions In Losses

zerohedge 8 October 2016

Dalio pointed out that thoughts which dared to question the economic orthodoxy, and which were once relegated to the fringe blogs,

have become the norm, pointing out that it is no longer controversial to say that:

…this isn’t a normal business cycle and we are likely in an environment of abnormally slow growth

…the current tools of monetary policy will be a lot less effective going forward

…the risks are asymmetric to the downside

…investment returns will be very low going forward, and

…the impatience with economic stagnation, especially among middle and lower income earners, is leading to dangerous populism and nationalism.

Globally, the stock market is about $69 trillion in size,

trading about $191 billion in shares per day.

The bond markets are well north of $140 trillion,

and trade about $700 billion in volume per day

zerohedge 4 October 2016

What should you do if Trump is right about a bond bubble?

Nigam Arora, MarketWatch Sept 29, 2016

In the first presidential debate, Donald Trump said,

"Now, look, we have the worst revival of an economy since the Great Depression.

And believe me: We're in a bubble right now. And the only thing that looks good is the stock market,

but if you raise interest rates even a little bit, that's going to come crashing down.

“We are in a big, fat, ugly bubble. And we better be awfully careful. And we have a Fed that's doing political things.

This Janet Yellen of the Fed. The Fed is doing political — by keeping the interest rates at this level.

And believe me: The day Obama goes off, and he leaves, and goes out to the golf course for the rest of his life to play golf,

when they raise interest rates, you're going to see some very bad things happen, because the Fed is not doing their job.

The Fed is being more political than Secretary Clinton."

Old Mutual Global Investors Ltd., which oversees the equivalent of about $436 billion,

says a policy change aimed at steepening the yield curve wouldn’t be surprising, even though it would come at the expense of bondholders.

“It would definitely see some pain,” said Mark Nash, head of global bonds at the London-based fund manager.

“Money flows across borders. It’s all linked.”

The claim that you can capitalize the stock market at an unusually high PE multiple owing to ultra-low interest rates,

therefore, implies that deep negative real rates are a permanent condition, and that governments will be able to destroy savers until the end of time.

The truth of the matter is that interest rates have nowhere to go in the longer-run except up

In his latest just released monthly letter, Bill Gross lays out the global economy as an analogy to Monopoly

where the narrative only works if everyone gets $200 in cash on every rotation around the board.

It’s the $200 of cash (which in the economic scheme of things represents new “credit”) that is responsible for the ongoing health of our finance-based economy.

Without new credit, economic growth moves in reverse and individual player “bankruptcies” become more probable.

And without banks creating new loans and injecting money into the broader economy, economic activity grinds to a halt.

Bill Gross $10tn negative-yield bonds a ‘supernova that will explode one day’

FT 10 June 2016

Trump, Englund och sedelpressarna

- People say I want to default on debt, You never have to default because you print the money

"If interest rates go up, we can buyback debt at a discount if we are liquid enough as a country.

Om man har en sedelpress går man inte i konkurs

Englund blog 10 May 2016

$17 Trillion Of Governments Yield Less Than 1%, Duration Risk Soaring

Investors face damaging losses if yields rise even a little

A half-percentage point increase would wipe out $1.6 trillion

Bloomberg Business 26 April 2016

Investors continuing to buy bonds even when they pay next to nothing suggests deep concern over the state of the global economy.

This month, the International Monetary Fund warned the threat of worldwide stagnation was rising because economic expansion has been so tepid for so long.

BlackRock chief Larry Fink

negative and low interest rates around the world are crushing savers, and

those policies are "going to become the biggest crisis globally."

Fink called on political leaders to step in and provide fiscal reform to complement monetary policy.

"We have become too dependent on central bankers" to boost the global economies, he said, stressing easy money policies were supposed to be a temporary healing.

"I don't call seven, eight years temporary. ... I don't see how that [still] has a positive impact."

Vi kan mycket väl bevittna världshistoriens största och kanske farligaste bubbla.

Räntorna är de lägsta på åtminstone 5 000 år.

Detta betyder att priset på obligationer är de högsta på 5 000 år.

Andreas Cervenka, SVD 27 januari 2016

Statspapper är själva fundamentet i det globala finansbygget.

Det totala värdet av alla världens statsobligationer uppgår till närmare 60 000 miljarder dollar enligt siffror från McKinsey.

Lägg till andra obligationer, där räntan direkt och indirekt påverkas av statslåneräntorna,

och siffran är runt 150 000 miljarder dollar.

I slutet av 2014 var värdet på alla världens aktiemarknader cirka 70 000 miljarder dollar.

Increasingly hysterical calls for negative interest rates, helicopter money and the like look premature

The era of zero interest rates has a lot longer to run yet.

Real rates of return, traditionally in the 2.5pc to 3pc range, are virtually impossible to come by

Jeremy Warner, 6 Feb 2016

Last month, the Fed lifted interest rates for the first time in nine years, and short-term bond yields have duly climbed higher.

But longer-term Treasury bonds have shrugged, with yields actually falling since the US central bank tightened monetary policy.

Robin Wigglesworth, Financial Times 7 January 2016

In all, the massive speculation unleashed in the equity markets since the March 2009 bottom

has caused more than $5 trillion of current cash flow and new debt to be allocated to corporate stock buybacks, M&A deals and LBOs.

The stock market is thus a creature of financial engineering, not a mechanism for efficiently allocating capital and accurately pricing prospective risk and return.

David Stockman, October 20, 2015

What I wish George Will, Bill Gross, and other free market advocates would consider is

the possibility that the Fed itself is not the source of the low rates, but simply is a follower of where market forces have pushed interest rates.

That is, the Great Recession and the prolonged slump that followed caused interest rates to be depressed and the Fed did its best to keep short-term interest rate near this low market-clearing level.

Economists view 20 October 2015

"We are at a sharp inflexion point," says Charles Goodhart, a professor at the London School of Economics and a former top official at the Bank of England.

As cheap labour dries up and savings fall, real interest rates will climb from sub-zero levels back to their historic norm of 2.75pc to 3pc, or even higher.

The implications are ominous for long-term US Treasuries, Gilts or Bunds. The whole structure of the global bond market is a based on false anthropology.

Ambrose Evans-Pritchard, 23 September 2015

The working age cohort was 685m in the developed world in 1990. China and eastern Europe added a further 820m, more than doubling the work pool of the globalised market in the blink of an eye.

"It was the biggest 'positive labour shock' the world has ever seen. It is what led to 25 years of wage stagnation," said Prof Goodhart, speaking at a forum held by Lombard Street Research.

The handling of the current financial crisis has reinforced too big to fail doctrine.

So how can one reduce moral hazard and reduce expectations of future bail-outs?

Living wills to curtail too-big-to-fail, perhaps even thereby allowing systemically important banks, such as Citigroup, Goldman Sachs or Barclays, to fail or, at least, to be unwound.

Charles Goodhart and Dirk Schoenmaker, FT August 9 2010

Throughout this extraordinary monetary experiment managers of listed companies have been reluctant to invest in fixed assets

despite enjoying the lowest borrowing costs in history.

By contrast financial institutions have been fearless in propelling markets ever higher.

John Plender, FT 6 august 2015

This dichotomy between subdued risk taking in the real economy and aggressive risk taking in financial markets has prompted Angel Gurría, secretary-general of the Organisation for Economic Cooperation and Dev-elopment, to remark that one or other of these views will be proved wrong.

The folk in Basel believe that low interest rates beget yet lower rates because they cause bubbles, followed by central bank bailouts.

Their worry is that we risk trapping ourselves in a cycle of financial imbalances and busts. .

Escaping from this once-in-5,000-year aberration may thus require Houdini-like skills.

The U.S. agency that monitors risks in the financial sector in the wake of the Great Recession

doesn’t yet understand why there have been an increasing number of sharp selloffs in U.S. and European bond markets,

the head of the organization said Monday.

MarketWatch 8 June 2015

The recent selloff wiped out about $1.2 trillion in value from the global bond market

And holders of debt globally are more exposed to the potential for big losses than at any time in history,

based on a metric known as duration.

Bloomberg 8 June 2015

After all, the potential for losses is now greater than at any time on record, based on duration levels for $50 trillion of debt tracked by Barclays Plc.

If yields on 10-year Treasuries rose to 3 percent by year-end, investors today would face losses of 3.6 percent.

Output is financially sustainable when spending patterns and the distribution of income are such that the fruit of economic activity can be absorbed without creating dangerous imbalances in the financial system.

It is unsustainable if generating enough demand to absorb the output of the economy requires too much borrowing, real rates of interest rates that are far below zero, or both.

Martin Wolf, FT 14 April 2015

Bonds beware as money catches fire in the US and Europe

The broad M3 money

"Forecasters ignore broad money at their peril," says Gabriel Stein, at Oxford Economics.

A dynamic measure of eurozone M3 known as Divisia - tracked by the Bruegel Institute in Brussels - is back to growth levels last seen in 2007.

Ambrose Evans-Pritchard, 15 Apr 2015

The developed world seems to be moving toward a long-term zero-interest-rate environment.

Though the United States, the United Kingdom, Japan, and the eurozone have kept central-bank policy rates at zero for several years already,

the perception that this was a temporary aberration meant that medium- to long-term rates remained substantial.

If debt can be rolled over forever at zero rates, it does not really matter – and nobody can be considered insolvent.

Daniel Gros, Project Syndicate 10 April 2015

In an environment of zero or near-zero interest rates, creditors have an incentive to “extend and pretend” – that is, roll over their maturing debt, so that they can keep their problems hidden for longer. Because the debt can be refinanced at such low rates, rollover risk is very low, allowing debtors who would be considered insolvent under normal circumstances to carry on much longer than they otherwise could.

After all, if debt can be rolled over forever at zero rates, it does not really matter – and nobody can be considered insolvent. The debt becomes de facto perpetual.

Governments do know how to stop a slide into another Great Depression. But, governments are haunted by fears of large fiscal deficits.

They have relied on monetary expansion, which is politically more acceptable, but also much weaker in its effect

Robert Skidelsky:, Project Syndicate 22 January 2015

Claudio Borio

Low inflation, bond yields and interest rates around the world will push the boundaries of economic and political stability to breaking point

if they continue on their downward trajectory, the Bank for International Settlements has warned.

Szu Ping Chan, Telegraph 18 Mar 2015

The Swiss-based "bank of central banks" said the "sinking trend" of global rates would push countries further into uncharted territory.

It highlighted that $2.4 trillion (£1.6 trillion) of long-term global sovereign debt was now trading at negative yields,

with an increasing number of investors willing to pay governments for the privilege of lending to them.

"As bond markets show us day after day, the boundaries of the unthinkable are exceptionally elastic," said Claudio Borio, head of the Monetary and Economic department at the BIS.

Why are interest rates so low? The best answer is that the advanced countries are still in a “managed depression”. This malady is deep. It will not end soon.

The fact that vigorous programmes of monetary stimulus have produced such meagre increases in output and inflation indicates just how weak economies now are.

The explosions in private credit seen before the crisis were how central banks sustained demand in a demand-deficient world. Without them, we would have seen something similar to today’s malaise sooner.

Martin Wolf, FT March 17, 2015

The Fed put

Federal Reserve uttered the single word “patience” and everything changed.

On Wednesday the stock market rose 2 per cent and on Thursday the Dow Jones Industrial index had its best day in three years.

The market dependence on Fed policy has never seemed greater

Financial Times December 19, 2014

Despite the fact that the Fed message also noted that rate increases could come as early next spring.

The game of chicken between the Fed and the markets is on once more.

Every time it seems that we are finally drawing to an end of easy money, something (or things) in the world go wrong and only Fed forbearance and patience can soothe the markets.

The flow of Opec petrodollars into global financial markets is set to dry up

as the collapse in the oil price delivers a $316bn hit to the cartel’s revenues.

The $316bn figure would be much higher if other big oil exporters including Russia,

Norway, Mexico, Kazakhstan and Oman are taken into account.

Financial Times, 3 December 2014

Gavyn Davies, The very long run equity bull market and

Lawrence Summers and Paul Krugman on secular stagnation

Gavyn Davies, FT blog, Nov 09 2014

Greenspan said that the Fed’s quantitative easing has failed in one of its goals, to spur demand.

Inflation is “dead in the water” because effective demand is “dead in the water,”

But quantitative easing has been a “terrific success” in getting the real rate of return on long-term assets down,

boosting all income-earning assets.

MarketWatch 29 October 2014

“It hasn’t been a success in the demand side,” he said, because banks are simply parking the reserves at the central bank.

“They just let it sit. Unless or until that happens, you don’t galvanize economic activity,” he said.

“When that starts, all things can happen - and not all of them are good,”

Strategin synes vara att det gäller att stabilisera, helst höja, villapriserna

så att konsumenterna främst i USA skall återgå till att konsumera med lånta pengar, dvs just det som ledde fram till katastrofen.

Detta kan inte vara klokt.

Det skrev jag på min blogg första gången den 5 december 2009.

Nu skriver jag det igen.

Rolf Englund blog 28 October 2014

Systems flooded with cash can sometimes freeze.

Having lots of money in the system does not guarantee that funding will flow freely

Gillian Tett, FT October 16, 2014

Since the 2008 crisis, western central banks have flooded the system with cash and expanded their balance sheets by – depending on how you calculate it – an eye-popping $7tn-$10tn.

But the problem with “liquidity” is that the word can mean several things; having lots of money in the system does not guarantee that funding will flow freely, or that traders can cut deals.

Forward-looking credit swaps already suggest that

Fed will not be able to raise interest rates next year, or the year after, or ever, one might say.

Put another way, it is possible that the world economy is so damaged that it needs permanent QE just to keep the show on the road.

Ambrose Evans-Pritchard, 15 October 2014

A rocky exit from low interest rates by the Federal Reserve risks

$3.8 trillion of losses to global bond portfolios,

IMF warned in its latest global financial stability report.

MarketWatch 8 October 2014

GLOBAL FINANCIAL STABILITY REPORT (GFSR)

Risk Taking, Liquidity, and Shadow Banking: Curbing Excess While Promoting Growth

October 2014

There is no bond market bubble

Using the Mankiw rule to predict US monetary policy 10-years ahead

The Market Monetarist/Krugman, 20 September 2014

I find it very hard to see why US bond yields should suddenly spike 200 or 300bp as some of doomsayers are claiming.

And finally I should stress that this is not investment advice and I am not making any recommendations to sell or buy US Treasury bonds and the market might go in whatever direction.

Don’t confuse brilliance with a bull market

I’ve noticed that many long-time bears are capitulating. If you look at market history, when bulls feel invincible and beaten-down bears give up, you have the makings of a market top.

When the Fed attempts to extricate itself from the market one day, that’s when the music stops, and the blame game begins.

MarketWatch, Michael Sincere 23 September 2014

Hindsight is a wonderful thing, especially when it comes to explaining market crashes.

The glaringly obvious guide to the next crash

James Mackintosh, FT September 21, 2014

International bond issuance, fuelled by ultra-low western interest rates, continues to swell:

Exotic issuers such as Pakistan, Zambia, Mongolia and Ecuador have successfully issued debt

Governments and companies in emerging markets have issued $796bn in debt this year,

compared with $734bn in 2013, according to Dealogic data.

FT 6 August 2014

Good recap of Argentina Passi Passu

Greenspan, 88:

How to unwind the huge increase in the size of Feds balance sheet with minimal impact.

It is not going to be easy, and it is not obvious exactly how to do it.

Interview with Alan Greenspan, MarketWatch 24 July 2014

Without asset-market surveillance, you do not have an integrated view of how the economy works.

How to respond to asset-price change is a legitimate issue. But not to monitor it, I think, is clearly a mistake.

Greenspan: I happen to agree that bubbles are primarily an issue to be addressed by regulation.

Low interest rates ‘ruining’ insurers

FT June 24, 2014

For decades, economic growth in America was driven by a powerful and sustainable force: increased consumption paid for by the rising incomes for middle-class and working-class Americans. But somewhere around 1980, that model broke down.

And now, with the economy only partially healed, it seems we’re going back to the lend-and-spend economy that failed us before.

Rex Nutting, MarketWatch 27 juni 2014

But somewhere around 1980, that model broke down. Wages flattened out, but consumption didn’t. Americans cut back on their savings, and took on more debt — mostly mortgage debt — to satisfy their needs and desires.

It’s not a sustainable model, but it did persist for nearly 30 years until the credit bubble burst in 2007. Millions of Americans lost their jobs, and millions lost their homes when the credit spigot was shut off, forcing average families to cut back on their consumption and live within their means once again.

And now, with the economy only partially healed, it seems we’re going back to the lend-and-spend economy that failed us before.

Full text"Battle raging between the world’s leading macroeconomists"

The European Central Bank has found itself caught in the crossfire

The Bank for International Settlements’ call last month has reignited the debate over how to explain – and tackle –

the financial and economic turmoil that has persisted over the past six years.

The debate is so fierce, the viewpoints so distinct, that two of the world’s leading multilateral organisations,

the BIS and the International Monetary Fund, have completely different ideas on what the ECB’s next step should be

FT Money Supply blog 14 July 2014

Ekonomerna mer oense än någonsin

Rolf Englund blog 2014-07-15

Infrastrukturinvesteringar har blivit det fikonlöv bakom vilket åtstramningens kolportörer

gömmer det faktum att nu även de vill stimulera ekonomin genom ökad efterfrågan.

Rolf Englund blog 15 juli 2014

På Gripenstedts tid var Sverige ett av Europas fattigaste länder, med hungersnöd år 1868.

Utan de stora statsfinansiella underskotten hade konungariket varit mindre skuldsatt, men utan järnvägar.

Carl-Johan Westholm, Liberal Debatt nr 3, publicerad på nätet den 19 maj 2014

For Prof Krugman, the BIS is another example of those who have been wrong about the crisis,

but refuse to acknowledge it and have to keep on inventing new bogey men to justify their point of view.

Except that as far as I can see it's precisely the reverse.

The BIS was one of the few international bodies to come anywhere close to predicting the crisis.

Jeremy Warner, 14 July 2014

If it sees the same mistakes being repeated again, then perhaps we should all sit up and take a bit of notice.

BIS's main point – that you cannot for ever rely on ever rising levels of debt as the main engine of growth – is surely correct.

Besides, any organisation that constantly attacks the policies of its owners, the world's major central banks, strikes me as entirely healthy in its own right, whether mistaken or not.

Liquidationism in the 21st Century

Paul Krugman JULY 12, 2014

BIS chief fears fresh Lehman from worldwide debt surge

Jaime Caruana says investors are ignoring prospect of higher interest rates in the hunt for returns

Ambrose Evans-Pritchard 13 July 2014

The world economy is just as vulnerable to a financial crisis as it was in 2007, with the added danger that debt ratios are now far higher and emerging markets have been drawn into the fire as well, the Bank for International Settlements has warned.

Jaime Caruana, head of the Swiss-based financial watchdog, said investors were ignoring the risk of monetary tightening in their voracious hunt for yield.

“Markets seem to be considering only a very narrow spectrum of potential outcomes. They have become convinced that monetary conditions will remain easy for a very long time, and may be taking more assurance than central banks wish to give,” he told The Telegraph.

The analytical underpinnings of the current phase of risk taking in financial markets are far from robust.

Less pleasant scenario – that of stagflation and greater financial instability.

Mohamed El-Erian, FT 14 July 2014

BIS Slams the Fed

"A Controlled Collapse?"

I propose Yellen is clueless. If she had any sense, she would have acted in advance to prevent an asset bubble

or at least stall the one Bernanke had started.

The Fed is not going to attempt a controlled collapse.

Yet, a collapse is coming. It will be anything but controlled.

Mike "Mish" Shedlock, 11 July 2014

An article on ZeroHedge entitled "Is The Fed Going To Attempt A Controlled Collapse?"

The question stems from lengthy (256 page PDF) from the BIS Annual Report

I will address the absurdity of that notion momentary, but first please consider some snips from the BIS report that caught my attention.

BIS

Investment by businesses is the key ingredient to cut our reliance on debt-fuelled current expenditure by consumers or the state

But there is a deeper issue to be tackled:

why does the economy have to be stimulated in artificial ways through the boosting of lending

Roger Bootle, Telegraph 6 July 2014

BIS warned that ultra-loose monetary policy risked causing another financial crisis.

It argued that interest rates should be raised, and indeed returned to normal, sooner rather than later.

BIS was one of the few institutions to warn of the coming financial crisis that shook the world in 2008.

Believe it or not, central banks, markets and the academic community had all lost sight of the fragility of the financial system and the importance of financial stability.

The BIS case was that ultra-loose monetary policy had engineered a false boost to demand by strengthening spending based on debt,

and by encouraging a regime in which credit risk was not properly assessed.

As a result, when a large shock arrived the system would shudder, if not collapse.

That is exactly what happened.

But there is a deeper issue to be tackled: why does the economy have to be stimulated in artificial ways through the boosting of lending to dodgy borrowers?

The main culprit is Germany. It is running a current account surplus of 7½pc of GDP.

Over the last 18 years, German consumer spending has grown by only 18pc, compared with a 53pc increase by UK consumers.

The second source of the world’s deflationary tendency is continued under-spending by two main groups of surplus countries: oil producers and the Asian emerging markets

There is now a gaping cavern between the interest rates available to retail savers and the rates of return sought by industrial and commercial companies when considering their investments.

As a retail saver you might be lucky to get 1pc or 2pc a year. Yet companies turn their noses up at projects which do not yield more than 10pc, sometimes 15 or even 20pc.

If spare capacity in the west were taken up by investment in productive plant, machinery and infrastructure, then demand would not need to be boosted by unsustainable mountains of debt.

Roger Bootle's latest book, “The Trouble with Europe”, has just been published.

Kommentar av Rolf Englund:

Javisst, men varför skulle företagen investera om de vet att konsumenterna skall dra ner på sina utgifter?

Grundbultsfrågan: Hur blir S = I ???

Savings and investment, being different activities carried on by different people

Man återkommer ständigt till Keynes och Hayek. Har den ekonomiska "vetenskapen" inte kommit längre?

Rolf Englund blog 8 juli 2014

Leonid Bershinksy weeps over the cruel world that for some reason isn’t listening to Jaime Caruana of the BIS,

who warns that we must raise interest rates now now now.

Why is this prophet so lonely? And where are the bond vigilantes?

Paul Krugman, JULY 5, 2014

Well, it might have something to do with the fact that three years ago Caruana and the BIS warned that

interest rates must rise to avert a surge of inflation.

I missed my chance to mark the anniversary, but it’s now five years plus since the WSJ warned that wildly inflationary monetary and fiscal policies were bringing on the bond vigilantes.

I admire the Bank for International Settlements.

It takes courage to accuse its owners – the world’s main central banks – of incompetence.

Yet this is what it has done, most recently in its latest annual report.

Martin Wolf, Financial Times 1 July 2014

It would be easy to dismiss this as the rantings of a prophet of doom. That would be a mistake.

Whether or not one agrees with its pre-1930s view of macroeconomic policy, the BIS raises big questions.

Contrariness adds value.

One can divide the BIS analysis into three parts:

what caused the crisis;

where we are now on the way out of it;

and what we should do.

On the first, the perspective is that of the “financial cycle”.

This analysis goes back to the work of the great Swedish economist Knut Wicksell

"All in all, the report is not good news"

BIS annual report suggests that “monetary policy is testing its outer limits,” and

that advanced economies, including the U.S., need “balance sheet repair and structural reform.”

Investors should take note, as the run-up in U.S. stocks has been driven by central bank accommodation using low interest rates.

MarketWatch 1 July 2014

Although near-zero rates are no longer effective in rallying the economy, they have sent investors into equities.

“Obviously,” the report concludes, “market participants are pricing in hardly any risks … a powerful and pervasive search for yield has gathered, and credit spreads have narrowed.”

All in all, the report is not good news

We must end this addiction to debt as the engine of growth

There has been no serious attempt to get to grips with the financial cycle,

which requires moving away from debt as the engine of growth

Jeremy Warner Telegraph 30 June 2014

In its annual report, Bank for International Settlements (BIS) spelled out

the risks of relying too heavily on monetary policy to stimulate the economy.

BIS warned that central banks including the Bank of England and US Federal Reserve could keep monetary policy loose for too long,

with potentially damaging consequences.

Szu Ping Chan, Telegraph 29 June 2014

BIS Annual Report, 2013/2014

29 June 2014

Jag tycker det är skriande uppenbart att räntan världen över är för låg och att

en större del av stimulanserna borde ske via finanspolitiken.

Rolf Englund, 5 december 2009

Conventional wisdom has it natural interest rates have fallen

With debt in the developed world standing at higher levels than before the financial crisis,

one of the more disturbing threats to financial stability is an unexpectedly sharp rise in global interest rates.

John Plender, Financial Times June 24, 2014

Policy rates. Over centuries these have been remarkably stable.The bank rate in the UK, for example, has averaged around five per cent since the Bank of England came into being in 1694.

The nearest I can find to a plausible case for a near-permanent downward bias to rates is a nightmarish one that comes from the economists at the Bank for International Settlements.

They have long argued that monetary policy making both in the US and elsewhere has been dangerously asymmetric.

Central bankers have failed to lean against booms, while easing aggressively during busts.

This has led to a downward bias in interest rates and an upward debt accumulation habit. Vicious circles result, because it becomes difficult to raise rates without damaging economic growth. At the same time the distortions in production and investment behaviour induced by persistently low rates prevent a return to more normal interest rate levels.

As Stephen Roach, former chairman of Morgan Stanley Asia, has pointed out, The US, is going back to the low saving, excess consumption growth model that prevailed before 2008.

Asset price bubbles and Central Bank Policy, Alan Greenspan

Bank for International Settlements

Fed’s easy money has disconnected markets from the real economy

Junk bond spreads near all-time lows and stocks at record highs

Is it time to sound the alarm over levels in the credit or equity markets?

Henny Sender, Financial Times 6 June 2014

Asset price bubbles and Central Bank Policy

Nils-Eric Sandberg, Stefan Ingves och mysteriet med den försvunna inflationen

Rolf Englund blog 23 mars 2014

but says it could begin scaling back later this year and ending it completely in 2014. BBC, June 20, 2013

In recent years an astonishing amount of money has quietly flooded into fixed income funds,

which buy corporate bonds, emerging markets bonds and mortgage debt.

And as the US looks more likely to raise interest rates, creating potential losses for bondholders,

the flows could reverse – creating destabilising shocks for regulators and investors alike.

Gillian Tett, 13 March 2014

A new paper from the Chicago Booth business school estimates that inflows to global fixed income funds have been almost $2tn since 2008, four times that of equity funds.

Seth Klarman, the publicity shy head of the $27bn Baupost Group

whose investment opinions have attracted a near cult-like following, said that investors were underplaying risk and were

not prepared for an end to central banks reversing a five-year experiment in ultra-loose money.

Financial Times, 10 march 2014

While noting that he could not predict exactly when a significant market correction would occur, Mr Klarman wrote in a private letter to clients:

“When the markets reverse, everything investors thought they knew will be turned upside down and inside out. ‘Buy the dips’ will be replaced with ‘what was I thinking?’?.?.?.?

Anyone who is poorly positioned and ill-prepared will find there’s a long way to fall. Few, if any, will escape unscathed.

Since central banks slashed interest rates to record lows and began a policy of buying up government bonds after the 2008 market crash, the S&P 500 has rallied by more than 150 per cent to new all-time highs.

While the mainstream media is loaded with flattering articles of the Fed’s brilliance in quantitative easing and its stimulus program,

the real beneficiaries of such a policy are the largest banks.

Here Seth Klarman notes they have placed the economy at great risk without achieving much reward.

Mark Melin, March 04, 2014, via John Mauldin

Bonds have been in a major bull market for nearly 33 years

— ever since the 30-year Treasury yield hit its all-time a high of 15.20% on Sept. 29, 1981.

MarketWatch, 25 February 2014

The 10-year’s yield record high came the next day, at 15.84%.

Today, in contrast, the 30-year yield is 3.7% and the 10-year’s is 2.74%.

Anyone whose investment careers began after 1981 has therefore never experienced a bond bear market. Assuming the typical investor doesn’t seriously start thinking about investing until he is 25 or 30 years old, especially about investing in bonds, that means that anyone today not in, or very close to, retirement has only known a bond bull market.

That’s an amazing historical and psychological fact, the significance of which cannot be overstated. It means that very few investors today have the long-term perspective with which to properly assess whether bonds are likely to suffer major declines in coming years.

The U.S. Treasury yield curve has lost its forecasting power

An ideal leading indicator would exclude components such as the yield curve that behave perversely during times of financial stress, said Morgan Stanley economist Ellen Zentner.

She suggested investors look at the Duncan Leading Indicator,

devised in 1977 by Wallace Duncan, then of the Federal Reserve Bank of Dallas.

Bloomberg, Simon Kennedy, Nov 27, 2013

Treasuries have turned anything but risk-free

The global financial system is hostage to a big rise in borrowing costs

when the retreat from QE puts an end to the current era of extraordinarily low interest rates.

John Plender, FT 22 October 2013

If any issue is going to cause surprises in the system in the coming years,

it is not necessarily going to be a credit risk at all;

interest rate risk could be more dangerous.

Gillian Tett, FT October 3, 2013

For the past few years, interest rates have been at rock bottom levels, and it is widely assumed this will continue.

But at some point the cycle will change, either because the central banks eventually tighten policy (in a good scenario), or markets panic (say, after a “technical” default).

And yet – oddly – the issue of interest rate risk gets far less focus in the new regulatory architecture than credit risk.

As Jens Weidmann, Bundesbank president, pointed out in a Financial Times editorial this week, this poses all manner of long-ignored dangers.

Worse still, there has been surprisingly little effort by the official sector to conduct public analysis of what surging interest rates might do to banks or asset managers

At a central bankers’ summit in Jackson Hole, Wyoming, a paper presented by Hélène Rey, economics professor at London Business School, identified a common global financial cycle

driven in part by Fed actions, with asset prices following investors’ risk appetites as measured by “fear gauges” such as Wall Street’s Vix index of expected stock market volatility.

If she is right, the recent turmoil in emerging markets could spread.

Financial Times, August 30, 2013

“If the reversing of easy monetary conditions is serious then, yes, I believe it will go across asset classes,” Ms Rey told the Financial Times. “But if the Fed acts slowly, it will be much easier for portfolios to adjust without major losses – it does depend on the speed.”

Some strategists are more cataclysmic. Not invited to Jackson Hole was Albert Edwards, Société Générale’s famously bearish global strategist,

who warned this week the crisis would not be confined to emerging market economies with yawning current account deficits.

“I see this as the beginning of a process where the most wobbly domino falls

and topples the whole, precarious, rotten, risk-loving edifice that our policy makers have built,” he wrote in a note.

Financial Times, August 30, 2013

Could it really have arrived? Are global stocks about to tank in an all consuming way?

Indeed, is this the moment Albert Edwards has been waiting for since 1996?

Of course, Edwards is perhaps London’s best-known doom-monger when it comes to stocks.

FT Alphaville Monday, March 5th, 2007

Holdings of Treasuries in China, the largest foreign lender to the U.S., fell in June

amid discussion by Federal Reserve officials about slowing the pace their bond purchases.

China’s stake dropped by $21.5 billion in June, to $1.276 trillion,

Bloomberg, August 15, 2013

Why Obama should not pick Summers for the Fed

Even worse, he has warned that policies such as quantitative easing and low interest rates

threaten to create malinvestment and new asset bubbles.

Scott Sumner, Financial Times, August 7, 2013

Professor Summers has argued that the Fed may not be able to control aggregate demand once interest rates hit zero, and therefore that we need to rely on fiscal stimulus.

Even worse, he has warned that policies such as quantitative easing and low interest rates threaten to create malinvestment and new asset bubbles.

Prof Summers is a brilliant economist and would probably display outstanding leadership skills in a banking crisis. But that is not what we need in a 21st century central banker.

The most important monetary trend of the past 30 years is the relentless decline in real yields on Treasury bonds, from 7 per cent to roughly zero. We can debate the causes of the decline, but there is no evidence that it will turn around soon. That means the US economy is likely to hit the zero bound in future recessions, again and again.

Some people seem to believe that large-scale asset purchases by central banks have created bubbles in many markets

and that stopping such purchases (let alone reversing them) must cause big falls in prices.

Others take the view that these central bank purchases are ineffective in stimulating demand in the wider economy.

I think the evidence for either of these positions is weak.

But some people believe both things – a position that I think is also contradictory as well as being profoundly pessimistic.

David Miles, external member of the Bank of England’s Monetary Policy Committee, FT 27 juni 2013

Three more years of zero interest rates

Whether it's in the long term interests of the economy is another matter.

Savers are again punished, and the profligate rewarded.

Jeremy Warner, August 7th, 2013

We know that the longer negative real interest rates persist, the more unbalanced and unsustainable the sort of growth they give rise to becomes.

BIS, which counts the world’s leading monetary authorities as members,

said cheap and plentiful central bank money had merely bought time,

warning that more bond buying would retard the global economy’s return to health.

Financial Times, June 23, 2013

It used its influential annual report to call on members to re-emphasise their focus on inflation and press governments to do more to spearhead a return to growth.

The BIS report comes on the back of last week’s markets turmoil, fuelled by Fed chairman Ben Bernanke’s comments that the central bank could slow its $85bn monthly bond-buying programme this year and end it by mid-2014.Unwinding the world’s biggest economic experiment

Gavyn Davies, FT June 21, 2013

The long retreat from easy monetary policy in the US has begun.

It is close to impossible to doubt that the three-decade bull market in bonds is over.

John Authers, Financial Times, June 21, 2013

The Federal Reserve, it is true, is still buying bonds at a rate of $85bn per month, and has not committed to a timetable for ending those purchases. But we now know that the Fed wants bond yields to rise. And indeed 10-year Treasury yields have risen more than a full percentage point since last July’s low, to 2.5 per cent. That is a tightening.

It is unclear whether the Fed really believes the US economy is strong, or fears that asset prices could be close to a bubble, but of its change in direction there can be no doubt.

Second, we can have faith in the immense latent power of central banks. The Fed has engineered this tightening, and removed air from asset markets throughout the world, just by jawboning. Indeed it continues to buy bonds at a fast rate.

Meanwhile, the ECB has created a persistent lull in the eurozone crisis by promising to do “whatever it takes” – and without, as yet, doing anything.

Third, and related to these, it is close to impossible to doubt that the three-decade bull market in bonds is over.

Opinions vary widely on what happened in Washington last night.

My take is that Fed has just tightened monetary policy.

Bernanke shifted the unemployment target from 6.5pc to 7pc, bringing the end of stimulus much closer.

Ambrose Evans-Pritchard, Telegraph, June 20th, 2013

The US Federal Reserve has refused to blink. The Chinese central bank has refused to blink.

The authorities in the world's two biggest economies appear determined to strike a blow against moral hazard and clear the froth in asset markets, at least until this exhibition of virtue blows up in their faces.

The term "Perfect Storm" is banned by the Telegraph as a lamentable cliché,

so let us just say that this is the moment we long been fearing or waiting for – depending on taste – when markets are no longer given what they want.

The Bernanke Put has become the Bernanke Call.

The Politburo Put has become the Politburo Call.

Rather than putting a floor under asset markets whenever there is trouble, they are instead putting a roof on asset price rises.

It’s hard to write a happy ending to ‘QE’ story

Have we finally witnessed the end of the great 32-year bull market in bonds?

John Plender, Financial Times, June 18, 2013

Yields on 10-year and 30-year US Treasuries up by half a percentage point since the start of May and emerging markets in a funk.

The eurozone still hangs like a dark cloud over the global economy, in recession with no comprehensive solution in sight to the problem of imbalances and a banking system that is undercapitalised and overloaded with sovereign debt.

As Stephen Lewis of Monument Securities remarks, the fear that the Fed will not taper, or indeed dare not taper, may be as significant a factor in the current malaise as anxiety that it will.

The market, he adds, has realised it is difficult to write a happy ending to this story.

UK and much of the eurozone appear determined to repeat the mistakes that inflicted stagnation on Japan

Basel III’s backstop leverage figure is just 3 per cent by 2019.

For a banking system to operate on the basis that a fall of a mere 3 per cent in the value of bank assets

will wipe out the banks is simply absurd

John Plender, Financial Times, June 21, 2013

Higher rates may trigger increases in bad loans, which would also create problems for banks, creating a financial crisis.

Financial markets are focusing on the potential exit from the expansionary fiscal and monetary measures,

low or zero interest rates and quantitative easing that policy makers have relied on to engineer a recovery.

Satyajit Das, Financial Times 17 June 2013

Central banks believe they will be able to exit when appropriate,

reminiscent of Ashly Lorenzana’s definition of addiction in her journal Sex, Drugs & Being an Escort:

“When you can give up something any time, as long as it’s next Tuesday.”

In reality, these policies may be hard, if not impossible, to reverse.

In the US, it now requires a government budget deficit of about $600bn,

augmented by injection of about $1tn in liquidity from the Federal Reserve,

to create about $300bn of growth.

Since 2008, the balance sheets of big central banks have expanded from about $5tn-$6tn to more than $18tn.

Zero interest rate and QE policies have increased financial risk.

Low rates allow overextended companies and nations to maintain or increase borrowings rather than reducing debt levels.

It becomes difficult for central banks to increase interest rates.

Levels of debt encouraged by low rates rapidly become unsustainable at higher rates.

Higher rates may trigger increases in bad loans, which would also create problems for banks, creating a financial crisis.

Satyajit Das is a former banker and author of

Traders, Guns and Money: Knowns and Unknowns in the Dazzling World of Derivatives, and

Extreme Money: The Masters of the Universe and the Cult of Risk

Amazon

– Om vi ser att de ekonomiska förbättringarna håller i sig kan centralbanken vara redo

att trappa ner på sina stimulansköp under de nästa mötena.

Ungefär så lät det från centralbankschefen Ben Bernanke den 22 maj

Enligt uppgifter från Bank of America Merrill Lynch har de globala börserna

förlorat 3000 miljarder dollar, cirka 20 000 miljarder kronor, i värde sedan den 22 maj.

Daniel Kedersted, SvD Wall Street blog 14 juni 2013

I dagsläget pumpar centralbanken in 85 miljarder dollar i det finansiella systemet varje månad.

Hittills har man satsat över 2000 miljarder dollar i konstgjord andning

Satsningarna är så pass tunga att marknaden i mannaminne aldrig varit så beroende av finanspolitiska stimulanser som idag.

Jag tycker det är skriande uppenbart att räntan världen över är för låg och att en större del av stimulanserna borde ske via finanspolitiken. Rolf Englund, 5 december 2009

This isn’t a /Bond market/ bubble in the classic sense of markets holding unrealistic expectations

It arises as a result of the correct perception of official policy.

But the extent of the distortion this has caused in the bond markets is quite remarkable.

Roger Bootle, Telegraph 9 June 2013

Index-linked bonds currently present the most remarkable features.

For most of their history, such “linkers” have yielded between 2pc and 4pc after inflation, that is, in real terms.

Recently, however, real yields have been negative.

That’s right, investors have willingly held them at yields which are bound to lose money in real terms.

And investors even have to pay tax on the interest.

Roger Bootle, Telegraph 9 June 2013

So what is going to happen?

What the appropriate level of interest rates and bond yields should be when things have returned to normal will depend crucially upon inflation.

If inflation is expected to run at something like 2pc, then we can expect conventional long bonds to yield between 4pc and 6pc.

Realräntor - Real Interest Rates

Authorities would surely need to maintain very low short rates while simultaneously putting pressure on the banks, pension funds and insurance companies to maintain high ratios of bonds in their portfolios “for safety reasons”. This is exactly what happened in the UK and the US in the years immediately after the Second World War and it is already happening again now.

In other words, such a regime would involve sharply negative real interest rates and real yields.

That is a substantial underpinning for the value of all sorts of assets, including residential and commercial property and equities.

But, of course, the foundations for such resilience are distinctly dodgy, because eventually the bond bubble will have to burst.

Yes, yields on US conventional 10-year bonds are up about 40 basis points over the past month.

But they are still just over 2 per cent. This is hardly a bond market Armageddon.

If recovery takes hold, as we hope, yields will rise further.

Nobody can have supposed that nominal and real long-term interest rates would remain at basement levels forever.

Martin Wolf, 4 June 2013

Comment by Rolf Englund:

Martin Wolf is right, of course, when he writes that "nobody can have supposed that nominal and real long-term interest rates would remain at basement levels forever."

Just as nobody before the start of the financial crisis can have supposed that houseprices would rise for ever.

Comment at FT

Many analysts believe that QE has caused a major bubble to appear in asset prices,

the full extent of which will be unveiled only when the central banks start to shrink their balance sheets.

Others reply that the rise in both bond and equity prices has been justified by economic fundamentals.

This is probably the most important debate in the financial markets today,

with enormous ramifications for both policy makers and investors.

Gavyn Davies, FT blog 26 May 2013

Is this the “big one” for global bonds?

The month just ended was the fourth worst month for government bond returns in the past two decades.

Gavyn Davies, FT blog June 2, 2013

Abrupt response to Ben Bernanke’s warning that the Fed might think about tapering QE

Fears that the great bull market in fixed income, which started in 1982, might now be threatened by a sharp reversal.

Can you hear the bears growling?

When bonds and equities were rallying globally until recently,

the bear argument was that central banks and regulators had created such worrying vulnerabilities

in the financial system that a plunge back to earth was only a matter of time.

That tipping point looks closer than we thought a month ago.

Financial Times 4 June 2013

In a topsy-turvy world in which good economic news is bad news – because it brings forward the day when QE stops – strong non-farm US payroll data on Friday could see further disruptive bond selling.

Bernanke is determined not to have a repeat of 1994 bond market sell-off

Investors Should Remember 1994

blogs.wsj.com/source/2010/12/29/

Last night's panic in Tokyo, where the Nikkei dropped a stomach churning 7 per cent, demonstrates just how difficult it's going to be for the world's central banks to exit their loose money policies.

You can do what Britain, and now Japan, are attempting, and inflate your way out of it.

Central bankers dream of getting back to "normal" – normal interest rates, a normal balance sheet, and so on.

But that point isn't going to come any time soon.

Jeremy Warner, Telegraph 23 May 2013

Why all the talk of a bond bubble?

What is a bubble, anyway? Surprisingly, there’s no standard definition.

But I’d define it as a situation in which asset prices appear to be based on implausible or inconsistent views about the future.

Dot-com prices in 1999 ... housing prices in 2006

Is there anything comparable going on in today’s bond market?

Paul Krugman, New York Times 9 May 2013

Dot-com prices in 1999 made sense only if you believed that many companies would all turn out to be a Microsoft;

housing prices in 2006 only made sense if you believed that home prices could keep rising much faster than buyers’ incomes for years to come.

You don’t want to buy a 10-year bond at less than 2 percent, the current going rate, if you believe that the Fed will be raising short-term rates to 4 percent or 5 percent in the not-too-distant future.

But why, exactly, should you believe any such thing?

The Fed normally cuts rates when unemployment is high and inflation is low — which is the situation today.

True, it can’t cut rates any further because they’re already near zero and can’t go lower. (Otherwise investors would just sit on cash.)

But it’s hard to see why the Fed should raise rates until unemployment falls a lot and/or inflation surges,

and there’s no hint in the data that anything like that is going to happen for years to come.

There isn’t any case for believing that we face any broad bubble problem,

let alone that worrying about hypothetical bubbles should take precedence over the task of getting Americans back to work.

Asset price bubbles and Central Bank Policy

Are the markets going mad?